Forum Replies Created

-

AuthorReplies

-

I believe the critic in question is Jamie Merchant, who is a sort of dogmatic follower of Moishe Postone, the arch idealist of 20th century marxism

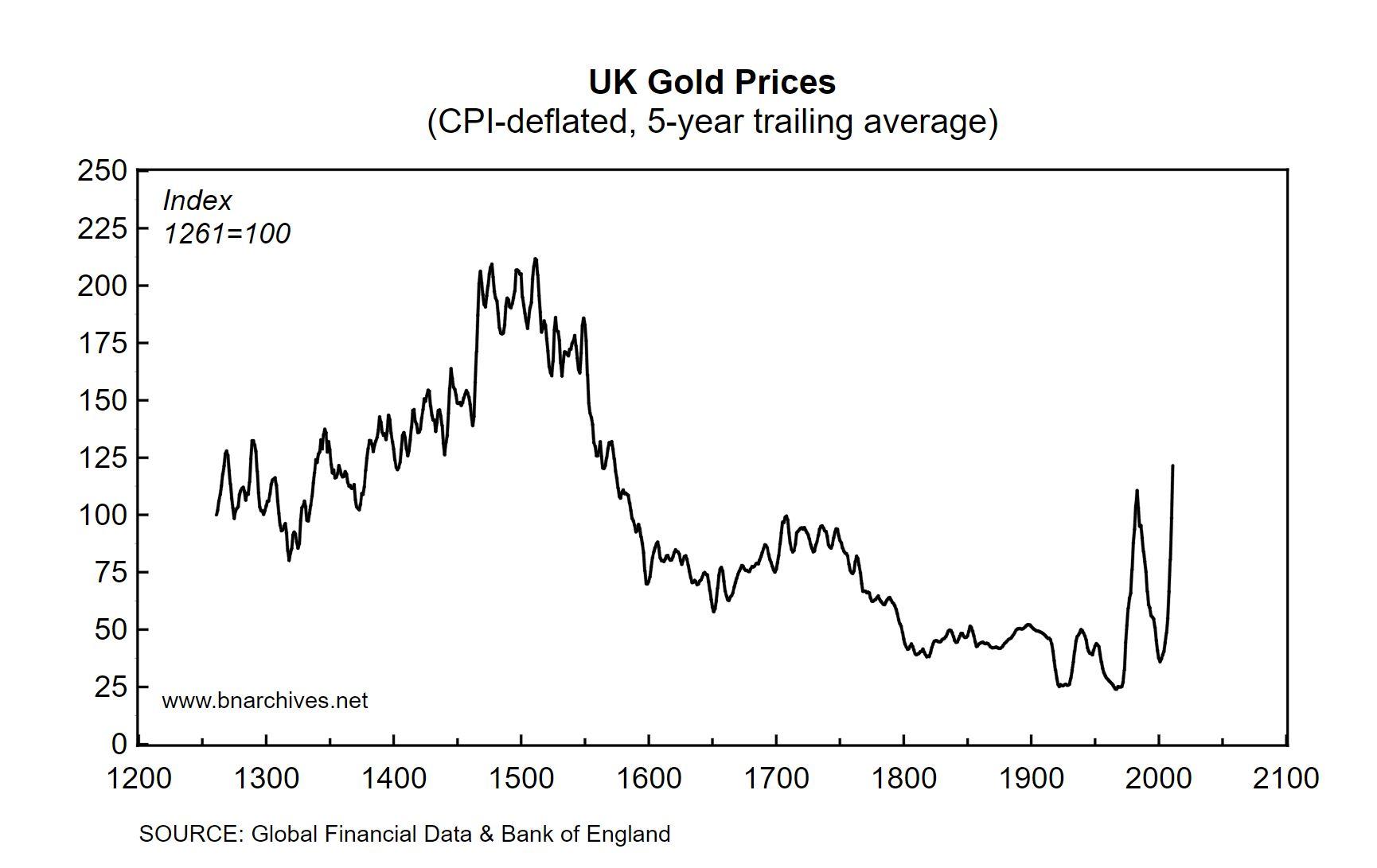

March 26, 2022 at 5:08 pm in reply to: Did Capitalism Change the Nature of Power, or Just Its Expression? #247883need to keep in mind that for most of the time period covered by this chart, the unit of account is in silver and the gold coin would be sometimes cried up or down in terms of the value of silver. so the main thing this chart is going to be tracking is the bimetallic ratio. Also, which price is being tracked here, — the mint price, or some market price? those are not necessarily the same. This matters precisely because the English monetary system for much of this period is characterized by an *undervalued* silver coin that defines the unit of account and an *overvalued* gold coin that made up the vast majority of the total nominal money supply.

There are a LOT of reasons for this changing price, which involve the entire world system: the black plague and the collapse of the yuan-ming fiduciary money in the 14th century, or the american treasure, etc. At the end of the 16th century the price of gold relative to silver is being suppressed in northern europe by the effects of the Habsburg-Genoese financing of the occupation of the Netherlands… and so on.

It’s not easy to disarticulate the changing value of money “as such” from the changing value of one money *against another*…

Issues with the CPI deflator aside…

Here is the pound price of gold relative to other UK prices. Is this price the same as gold’s value? If yes, why is this value changing? If no, what is this value?

- This reply was modified 4 years ago by Colin Drumm.

- This reply was modified 4 years ago by Colin Drumm.

- This reply was modified 4 years ago by Colin Drumm.

March 26, 2022 at 5:01 pm in reply to: Did Capitalism Change the Nature of Power, or Just Its Expression? #247882A monometallic mint standard does contain the same “option” since there is a legally defined premium on the domestic coin. a legal silver coin is worth more under domestic law than the silver in it, but also contains the option to melt or export the coin.

The monometallic mint cannot be arbitraged in quite the same was as a bimetallic mint. But there is a potential for arbitrage in the case that the price of a coin on a foreign exchange rises higher than the price of a bill exchange. In other words, if I can sell 240 pence for X foreign money and purchase a bill for a pound sterling drawn on london for X-Y foreign money, that would also constitute an arbitrage point.

There’s nothing mysterious about “intrinsic value.” But it has units denominated in metal, not in terms of nominal unit of account. In order to know the relationship between these two things, we need to know the policy stance of the mint (the level of seignorage + brassage and the mint price). That will give us the legal overvaluation of the coin. But whether this overvaluation is correct or not (too high or too low) is something that can only be determined by comparison to a foreign market.

“Colin will insist that it was Lydian kings who introduced money, but, like most ancient historians, he is far too credulous of ancient historians, who are famous liars”

i would say nothing of the sort. the earliest *coins* are indeed from Lydia, but not all money is coins. coinage is an intervention into a monetary system that already existed for a long time before the development of coinage during the breakup of the neo assyrian empire.

March 9, 2022 at 11:12 pm in reply to: Did Capitalism Change the Nature of Power, or Just Its Expression? #247864“There is nothing in gold that makes it valuable.”

Blair, this is just not true. Gold is valuable because it is a material that can be used to make very impressive status objects out of. In order to say that there is nothing valuable about gold, you would have to also say that there is nothing valuable about the vast majority of things that are produced by modern economies. You might think this, but it’s a normative judgment, not a description of how things work.

Gold is valuable because it can be used to make objects that impress people, and impressing people is a very important kind of power. A view that is centered around **power** would do well not to abstract from this. It is important for understanding the phenomenon of money at an anthropological level.

You are voicing a version of the “abstraction thesis” about money that forms part of the received common sense, but it doesn’t really do a good job of accounting for the phenomena. On this point, “Private Money and Public Currency: The Sixteenth Century Challenge” by Boyer-Xambeau et al is especially important.

Credit is only a substitute for coin to the extent that the payments graph is symmetrical. the difference between money and credit is an index of the asymmetry in the graph of the monetary economy. the insufficiency of money in the medieval economy is not relative to “exchange” simply put, but relative to the need to finance clearinghouse drains

” my understanding has always been that business between parties with a long-term relationship (neighbors, relatives, friends, trading partners) was largely conducted with credit (credit preceded coinage by millennia). Coin, when available, would be used for periodic settling of accounts.”

so now you can see why a debasement is a unit of account devaluation for legally enforceable debts. the unit of account refers to a coin, and if the legal definition of that coin changes, so does the meaning of the unit of account.

Drumm writes: “monetary interventions such as debasements are intended to draw hoarded coins out of hoards and to the mint.”

This doesn’t make sense. Why on Earth would debasement of the circulating coin encourage one to exchange good coin for bad? During medieval times point with bulk silver could have to minted into coins for a fee. But if you already have coin there is no need to remint it.

I am no expert…”

The last bit is definitely correct 😛 This is a fundamentally basic point to understand about the history of debasement.

Debasements are enticements to dishoard coins for a very simple reason: by selling old, good coins to the mint for new, bad coins, the seller will receive a profit in domestic unit of account. Thus, if I owe a debt for a pound sterling, and I have 240 good old pennies, and the mint is offering to purchase those old pennies for 250 pence in new bad pennies, I may want to hit the window even though the 250 pence in new bad pennies have less silver than the 240 good old pence. That is because I can now pay my debt for a pound and have 10 pence left over. If I had paid the debt with the good pennies, I would have nothing. Now, it is possible that my counterparty may wish to accept my good old pennies at a premium, rather than be forced to accept the new bad pennies instead. But if he wishes to enforce payment against me in a court, I always have the option to pay the 240 bad pence instead of the good ones.

I hope you can now see why a debasement is an anti-hoarding monetary policy intervention. For more details, you can consult the dissertation.

I am skeptical about the construction of price level indices for these periods so i would want to get very into the weeds about how exactly the index has been constructed. what is the basket of goods and what is the source material?

In general, deep price history seems to have a two-phase attractor — there are periods of relative stability, and there are periods of “price revolution.” One tricky thing about studying price revolutions is whether we ought to measure prices in relation to silver or in relation to the unit of account — so in the sixteenth century, nominal prices are rising, but the silver content of the unit of account is also falling, and to fully understand what is going on we would need to disaggregate those things.

Price level history is really not my expertise although I do have some thoughts about it. The historical debate is between those who see price level changes as always driven by “real” variables such as demography, and those who see the effects as monetary. I suspect that both things probably happen. But things get complicated as in the case, for example, of the sixteenth century and the American treasure, where it probably the *bimetallic ratio* that matters more than simply the *quantity* of money, which is what moderns are accustomed to think about.

I’d be very interested in working with more data-oriented CasP researchers on this topic going forward. But we have to begin by having a materialist/institutional picture of the relevant monetary systems, which is what my work is about. My research presents a theory of the relationship between the mints and the exchanges that has not been previously fully understood.

So the question about the price level or Mehrling’s “fourth price of money” is somewhat unresolved in what I write in the dissertation…

“If pre-modern money was a store of (precious metal) value”

here I can tell you something more for certain, which is that the biggest issue was generally the hoarding of money. monetary interventions such as debasements are intended to draw hoarded coins out of hoards and to the mint. I write about this in the dissertation. modern money is fundamentally different from coinage in that coins are not fungible — if i have a good coin in my floorboards, there is nothing the king can do to remove silver from it other than tempting me to dig it up and bring it to the mint. not the case with modern reserve notes, which lack an “outside option” to melt and thus derive their value purely from the “inside option” of their legal tender status.

Hi Scot!

really delighted that you are reading my work and picking up on what matters about it.

i just want to point out one small correction: as I show in chapter 3, the negative economic effects of a scarcity of money is not just borne by the “commoners” as in proletariat, but also by the “commons” as in the non-landed mercantile interests in the city of london. perhaps in the revised version i should telegraph this more explicitly in chapter 2.

cheers!

C

-

AuthorReplies