Home › Forum › Political Economy › The distintegration of neoliberalism

- This topic has 10 replies, 4 voices, and was last updated January 28, 2022 at 5:28 pm by Michael Alexander.

-

CreatorTopic

-

January 25, 2022 at 2:59 pm #247623

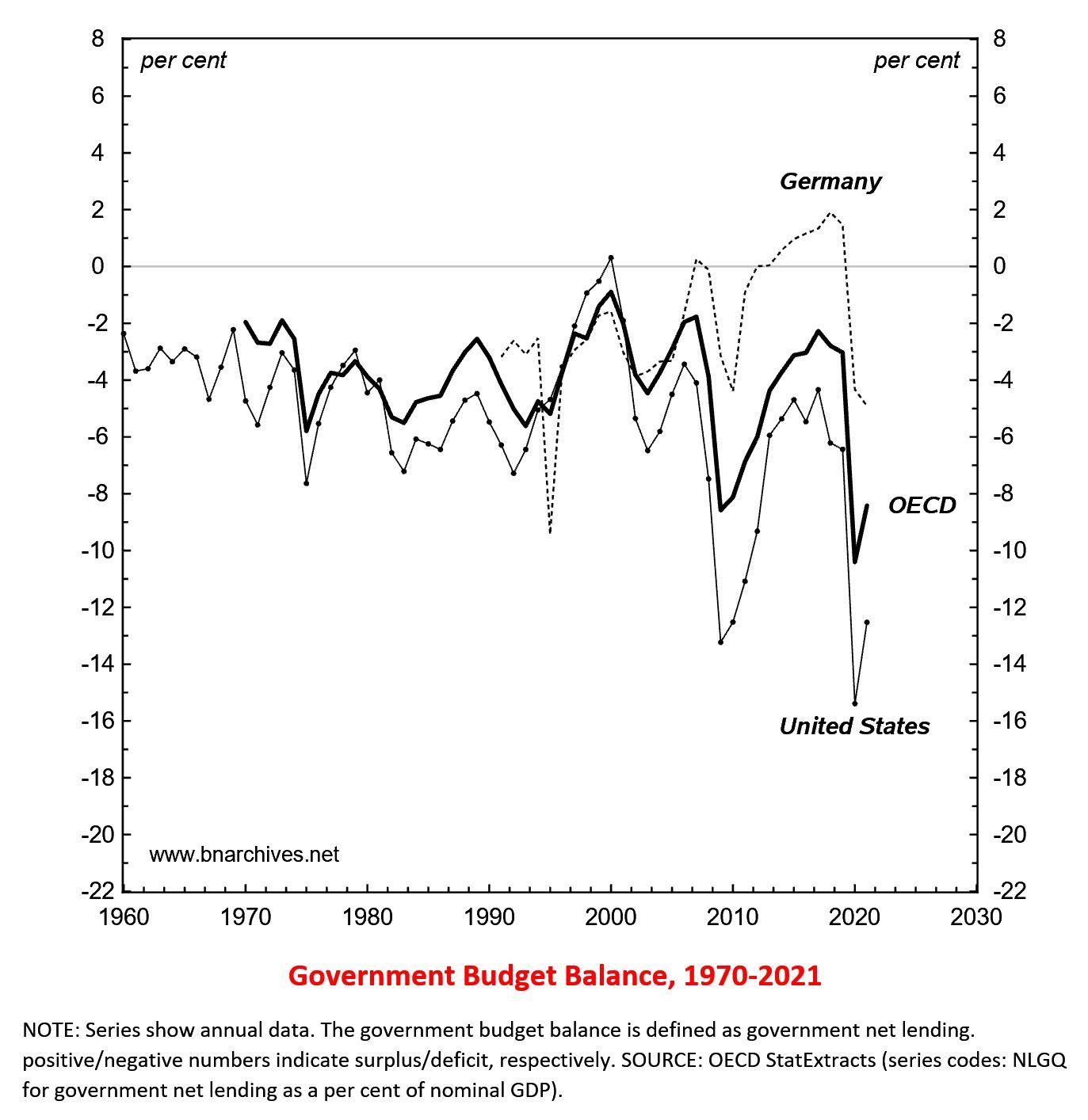

Look at the growth of those OECD government deficits, particularly in the United States, the bastion of the ‘free market’.

-

CreatorTopic

-

AuthorReplies

-

-

January 25, 2022 at 4:05 pm #247624

That’s neoliberalism working as planned. One truth for the masses, another truth for the elites.

-

January 25, 2022 at 4:08 pm #247625

Wow, what an eloquent graph.

Is the small “dead cat bounce” of 2021 (if I’m not mistaken) due to the general Covid-related recovery plans issued in OECD countries?

-

January 25, 2022 at 5:45 pm #247630

Is the small “dead cat bounce” of 2021 (if I’m not mistaken) due to the general Covid-related recovery plans issued in OECD countries?

Could be.

-

-

January 25, 2022 at 5:37 pm #247626

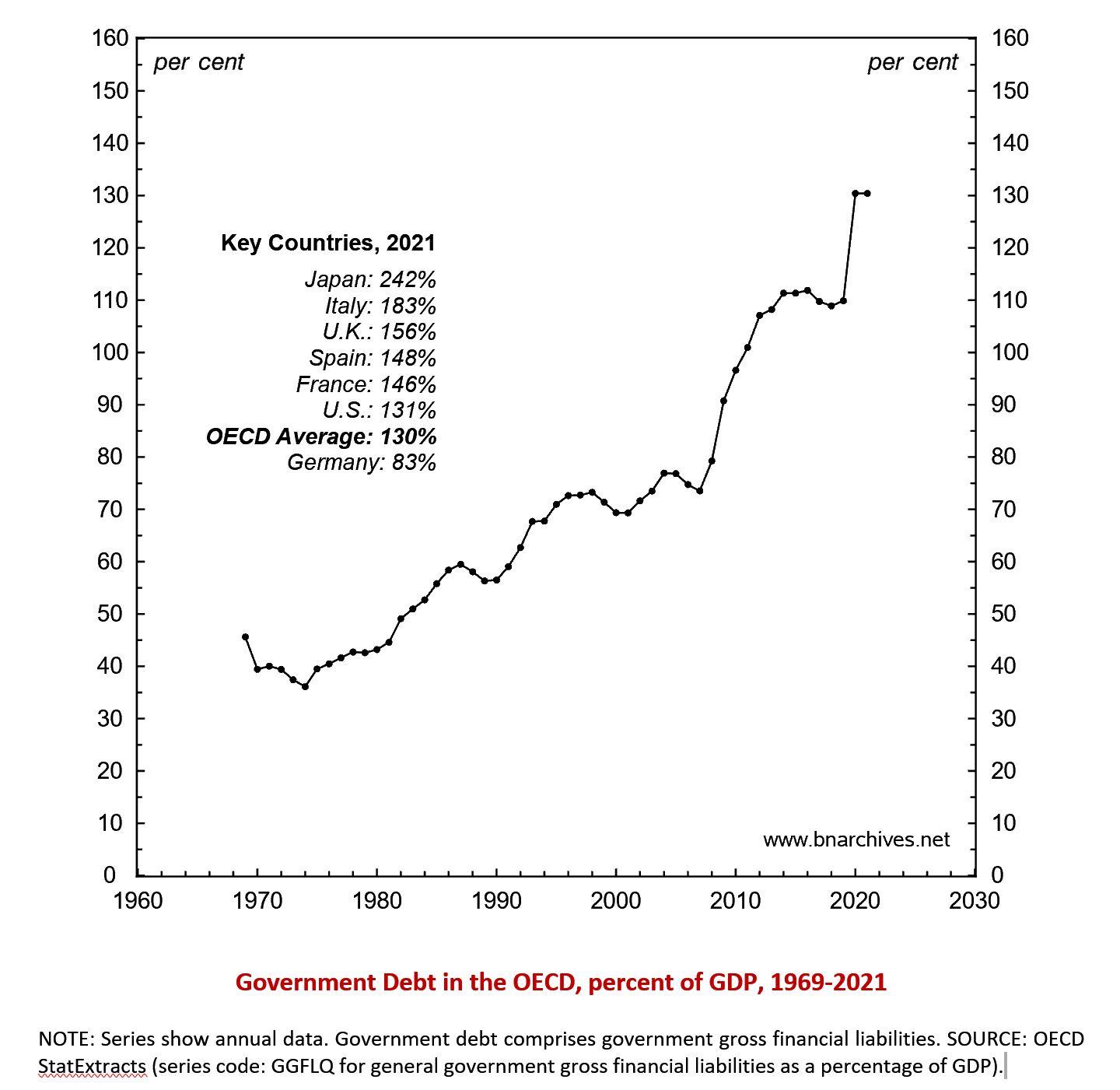

The neoliberal debt balloon: since 1980, the economy grew freer and freer while the OECD government debt/GDP ratio inflated. By 2021, this ratio was three times larger than it was in 1980.

- This reply was modified 4 years, 2 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 2 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 2 months ago by Jonathan Nitzan.

-

January 25, 2022 at 7:32 pm #247631

Well, second place for my country! So proud!

Jokes aside, is there a specific event that we should consider as the key trigger? Doesn’t this all coincide with the end of Bretton Woods?

-

January 25, 2022 at 8:14 pm #247632

… is there a specific event that we should consider as the key trigger? Doesn’t this all coincide with the end of Bretton Woods?

I don’t know about triggers, events and Bretton Woods.

From a CasP viewpoint, the reason seems straightforward.

Neoliberalism is the rule of dominant capital; this rule is based on the hierarchical growth of dominant capital; this hierarchical growth amplifies the extent and intensity of strategic sabotage; and in order to avoid systemic implosion, this sabotage must be offset to some extent. That is why neoliberal governments become bigger, the deficits get amplified and their debts soar.

For a recent account of this process, see Dominant Capital and the Government.

-

January 28, 2022 at 5:28 pm #247662

It is instructive to extend this type of relation further back. The figure below is US government debt as a percent of GDP over time. The dashed line is when the Bretton Woods system collapsed. What we see are periods when debt/GDP is falling and periods when it is rising. Prior to the 1979 “October Revolution” in Fed policy, fiscal policy affected inflationary dynamics. For example, Table 4.1 in my book shows how fiscal balance during periods of war vs. peace in Anglo-American wars from the war of the League of Augsburg to WW I is correlated with inflation. https://mikebert.neocities.org/America-in-crisis.pdf

Periods after wars, when debt was being paid down, shown in the figure below as declining ratio of debt/GDP were exerted a deflationary effect, while periods of rising ratio had an inflationary effect. Accommodative Fed policy (low real interest rates intended to spur economic growth) is inflationary since it leads to creation of more private debt. During the postwar boom, Fed policy was accommodative resulting in strong growth. The inflationary effects of this were countered by the deflationary effects of declining debt/GDP. This downwards trend ended shortly after the end of the Bretton Woods system, which allowed the inflationary effects of Fed low interest policy to manifest as 1970’s inflation. This inflation led to the October Revolution that end the relation between fiscal balance and inflation. For the next two decades inflationary fiscal policy shown by the rising ratio in the figure was countered by tight Fed policy which controls inflation by preventing wage increases (if wages don’t rise, consumers will be more price conscious producing the desired deflationary effect). After giving China MFN status in 1999 it was not possible to exert a deflationary effect by exporting dollars overseas in return for goods (trade deficit). This affects the ratio of dollars circulating in the US relative to goods available for purchase, which should have a deflationary effect.

The figure ends in 2019 and so doesn’t show the big increase as a result of Covid. Recent experience with inflation suggests that the inflationary impact of rising debt/GDP is finally overwhelming the deflationary effect of trade imbalance and with interest rates near zero there is nothing to stop inflation. Time will tell is this is so.

- This reply was modified 4 years, 2 months ago by Michael Alexander.

-

-

-

January 26, 2022 at 5:48 pm #247636

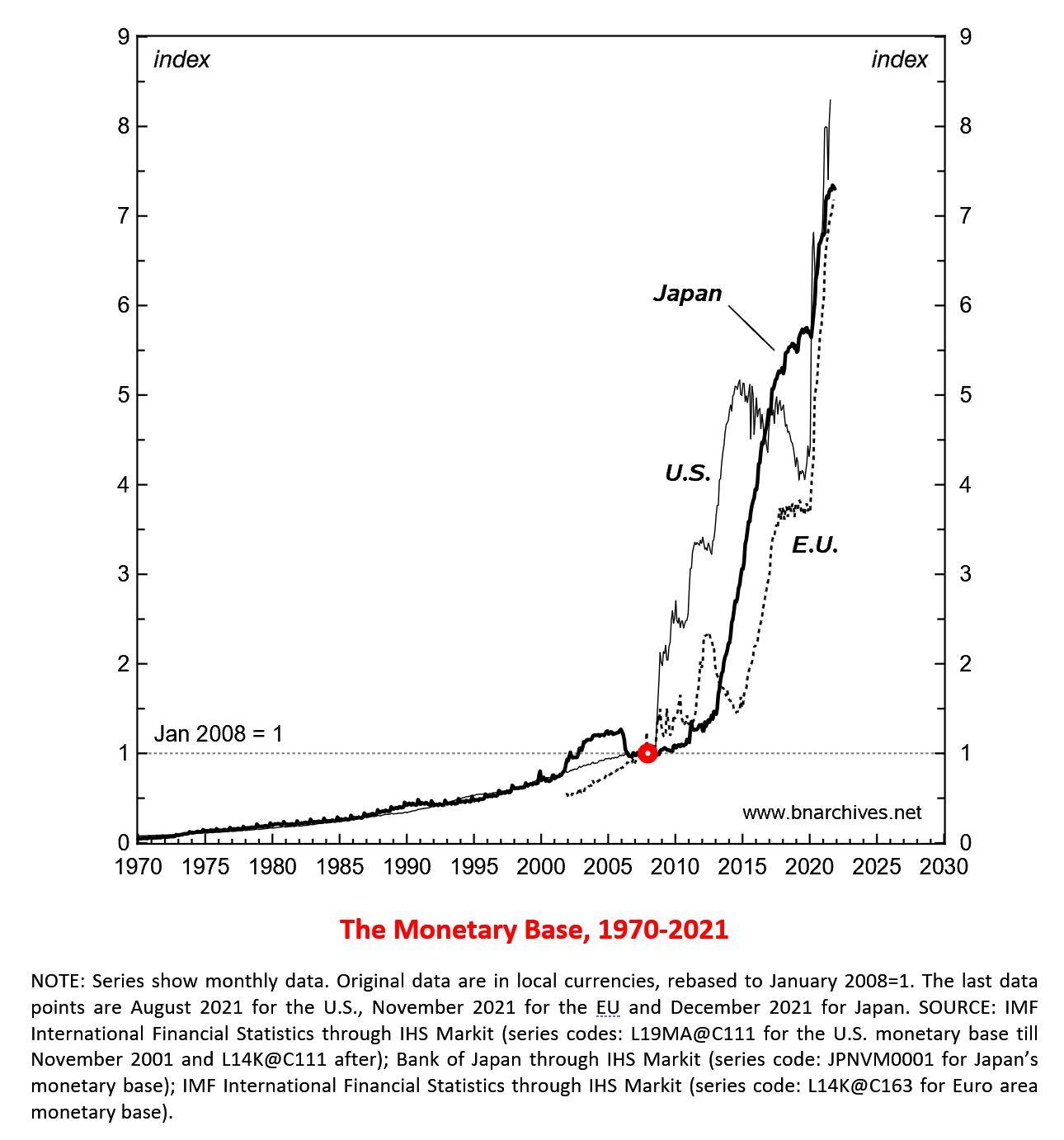

The end of monetarism

A note by Shimshon Bichler & Jonathan Nitzan

According to Milton Friedman, inflation is always and everywhere a monetary phenomenon of too much money chasing too few commodities. Following this logic, the Holy Grail of neoliberal policy is to have the so-called money supply expand just a bit faster than the long-term growth trend of the ‘real economy’. This way, the economy is given some flexibility — but not enough to stoke the monetarist fire of inflation.

And sure enough, as our chart shows, central bankers in the advanced capitalist economies — the U.S., Europe and Japan — adhered to the spirit of this policy up until the early 2000.

The chart plots the size of the ‘monetary base’ — namely, the overall value of notes and coins circulating in each country/area. This value is expressed in local currency and is rebased with January 2008 = 1 to enable temporal comparisons between the different series.

Until the beginning of the new millennium, the monetary base grew gradually and predictably, just as monetarism demanded. But in the early 2000s, the orthodoxy started to rattle. The first deviant was the Bank of Japan, whose ‘quantitative easing’ aimed — or so we were told — to fight the country’s persistent deflation. And then came the 2008 global financial crisis and all hell broke loose.

Having panicked, ‘policymakers’ started issuing high-power money as if there was no tomorrow. Initially, they justified their heresy by end-of-the-world scenarios of financial collapse. But while the danger came and went, their quantitative easing stayed. Since 2008, the monetary base of the EU rose 7.2 times, Japan’s 7.3 times, and the U.S.’s 8.3 times.

Adding insult to injury, this historically unprecedented breakdown of monetarist policy was accompanied by an equally radical refutation of monetarist theory. Recall that monetarism claims that money growth fuels inflation — yet despite the monetary explosion, inflation refused to cooperate. From 2008 to 2020, consumer prices rose by only 29% in the U.S, 17% in the EU and a mere 3% in Japan.

For more: see ‘Can Capitalists Afford Recovery? Three Views on Economic Policy in Times of Crisis’.

-

January 26, 2022 at 7:23 pm #247638

First, I had always understood that the Fed’s love affair with monetarism died with Volcker’s failed monetarist experiment in the 1980s, that the Fed thereafter returned to targeting the Fed Funds Rate instead of trying to actively manage debt and monetary aggregates.

Second, what the Fed publishes (and the IMF appears to use) as the US monetary base (the series BOGMBASE) is not “the overall value of notes and coins circulating in each country/area” but rather the “currency in circulation” plus “reserve balances,” which by definition do not circulate. See the H.6 Release of Monetary Stock Measures. Since Sep 2008, most of the increase in BOGMBASE has been driven by increasing reserve balances, and reserves currently equal roughly double the currency in circulation. Compare reserve balances (TOTRESNS) to currency in circulation (CURRSL).

My working theory is the Fed in 2008 increased reserve requirements such that reserve balances were roughly equal to M1 (which then only include demand deposits, i.e., checking accounts, and not savings accounts) to prevent further bank failures. In 2020, the Fed redefined M1 to include most of M2, and last year the Fed reduced reserve requirements to 0%, which makes the increase in reserves last year hard to explain (unless the Fed also upped the interest paid on reserves).

-

-

January 27, 2022 at 9:01 am #247640

Thank you Scot.

First, I had always understood that the Fed’s love affair with monetarism died with Volcker’s failed monetarist experiment in the 1980s, that the Fed thereafter returned to targeting the Fed Funds Rate instead of trying to actively manage debt and monetary aggregates.

I think it is useful to distinguish monetarism from its policy instruments. Interest rates and the so-called money supply (an umbrella term that can mean many different things) are often used as policy instruments. They are also related, insofar as changing one alters the other, and vice versa. Central bankers and economists bicker constantly on the proper way to calibrate these slippery variables.

That being said, theoretically, most central bankers and mainstream economists agree that inflation is a monetary phenomenon in the sense that P = M * V / Q, and then argue endlessly on the meaning of each variable and how they lag each other in time. (When I came to work at the Bank Credit Analyst Research Group in the 1990s, I presented some of my PhD work on ‘Inflation as Restructuring’. One of the lead editors told me that although he found my argument fascinating, in the final analysis in didn’t matter: when all was said and done, inflation was all about the growth of money.)

what the Fed publishes (and the IMF appears to use) as the US monetary base (the series BOGMBASE) is not “the overall value of notes and coins circulating in each country/area” but rather the “currency in circulation” plus “reserve balances,” which by definition do not circulate.

Yes, you are correct; my definition was inaccurate. But the distinction between currency in circulation and reserve balances is mostly a technical feature that facilitates settlements among private banks and between private banks and the central bank. The key thing is that the monetary base is the only money aggregate that central banks control directly. The other aggregates (M1, M2, etc.) are determined jointly with the private sector.

-

-

AuthorReplies

- You must be logged in to reply to this topic.