Forum Replies Created

-

AuthorReplies

-

I just cannot agree that your narrative offers a complete explanation of the interaction between the movie industry (the creators) and the movie business (those who sabotage the creators in search of profits).

I would not claim that Hollywood Business doesn’t Strategically Sabotage Hollywood Industry. It definitely does, My contention here is that the depiction by Jacobin isn’t accurate. What is being sabotaged is not the creativity. I come from an Arts background, with several years in theatre and film. I was on stage, and in front of the camera, and behind the curtain and the camera.

It’s difficult to argue that creativity isn’t stifled by budget constraints, but having worked with both big budgets and highly restricted budgets, I can confidently say that in situations where budgets were limited, we got more creative with the story-telling, and the technical techniques, in order to make the money we did have available, work better for us. There is also a measure of push-back that emerges when you constrain budgets, and the creatives then tend to encode anti-power subtext throughout their works.

The homogenization of media content of all types is undeniable and has been noted by many people over the last decade or two.

This is where I disagree, and to be honest, the only thing that will change my mind is a detailed analysis of content, which none of the opinion pieces over the last 2 decades have provided. Instead, what they provide, are very cherry picked instances of Executive interference in the creative process, and subjective critiques of the movies that just happen to confirm their “movies are becoming the same” line.

Close to 12 thousand movies released in the last 14 years, means we cannot use a sample size of 20 movies, and use that to extrapolate any kind of meaningful conclusion.

Homogenous does not have to mean “bad,” but it always means “the same or similar.”

Debate exists within the arts community about the variety of stories it is possible to tell. Meta-narrative pundits have been saying since the time of the ancient greeks that there are only 3, or 6, or 7, or 12, or 36 stories that can be told. Regardless of the number there is indeed a very low upper limit to the variety that can be used in basic plot lines. Creativity is not in the basic plot, but in how we tell the stories. So homogenous plots are definitely an observable phenomena, but the creativity with which they are told, is a very different concept. It is this creativity that I highly doubt is being sabotaged, or indeed can be sabotaged. The Audience simply would not tolerate it.

Whether these five companies refuse to fund ground-breaking movies with unfamiliar or unproven themes, or just crowd such movies out by buying up all the theater space, creativity is being hindered.

Crowding Indy Studios out of theatres was certainly the case from the 80’s to the early 2000’s,

but since Netflix’s rise to prominence there has been a massive shift in the power dynamics of the industry, and every VOD and SVOD service is clamoring for content, which provides a fair bit of leverage for independent studios in negotiations. But again, this doesn’t affect the creative process, it merely affects the budgets that the studios have available.If capitalism ultimately succeeds, there truly will be nothing new under the sun because capitalists seek pareto efficiency, which requires sticking with what reliably works, i.e., the familiar.

In this context, Pareto Efficiency would mean that a major studio would gain differentially over its competitors by providing more creative control to creators, since this would reduce the benefit the other studio is getting from witholding creative control. Or maybe i’m misunderstanding your usage of Pareto Efficiency here

Hi Scot,

I’m going to try to make my case, using limited data, and a relatively simplistic argument.

The argument being made in general in the Jacobin article might make use of the term “risk” appropriately, but the underlying suggestion is that creative control is the risk factor that is hedged against.

I wont argue that Hollywood finance isn’t risk averse. That would be silly. Instead I would say that a plethora of research on the subject has indicated that in order to minimize risk, the predominant factor in the finance equation is a very simple “low budget – high projected return” production. Risk is not in the creativity, or the controversial nature of the projects. And so homogeneity of content has very little to do with the decision being made by executives.

Jacobin does make a good point in that part of the risk aversion exhibited by Hollywood studios, is the tendency to put out larger volumes of movies with lower returns, than to bet everything on very few blockbusters with the potential for high returns.

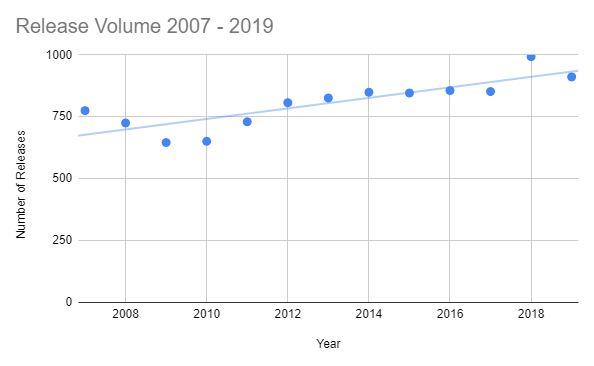

Here we can see an overall increase in total volume of theatrical releases from 2007 – 2019

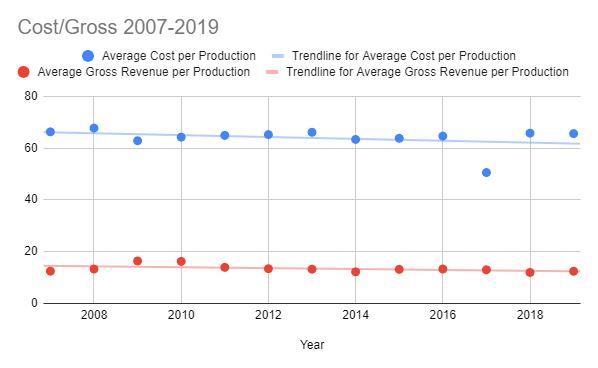

Then if we look at the same period and start inspecting the finances, the average cost per production far outweighs the average revenue per production.

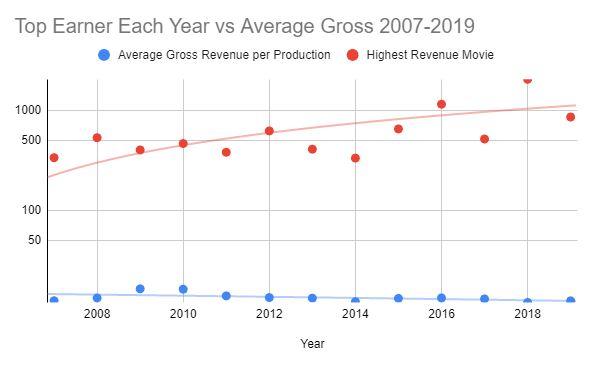

Finally if we compare each year’s top earner to the baseline average gross per movie, we can see that the vast majority of the movies being produced are not big revenue earners at all

This seems to suggest that the vast majority of the 700-800 movies released annually, are not being produced with any thought to limiting creative control to conform with homogenized audience demands, but purely to minimizing budgets. With the odd Big Earner to make up any potential shortfall.

And on the streamer side of content, it is all about churn. They don’t care if a movie or series is creative or not. What they care about is having a broad base of diverse IP that appeals to every niche they can find through their algorithms.

Is Hollywood risk-averse? Yes

Does Hollywood’s risk aversion result in bad movies? I would answer by saying tastes vary, even within targeted demographics, but for the most part, no.- This reply was modified 4 years, 7 months ago by Pieter de Beer.

I only briefly perused the article, and right off the bat, their understanding of entertainment risk seems to be inconsistent with corporate and financial risk.

They seem to be conflating the notion of stories that might not viewed, with the risk that CasP explicitly describes as the risk of not beating the average.

While there is probably some slight overlap, the 2 are not the same.

They also, in a single article, state that movie content is becoming universalized, and that streaming content is becoming ever more niche and diversified in order to appeal to specific demographics.

So both strategies, according to Jacobin, are risk averse, suggesting that no matter what trend would be taken by content creators, it would be considered the result of risk aversion.

This indicates that their understanding of Risk needs a lot more clarification

Hi Rowan.

I read your walls of text. Which is how I am able to formulate my questions. There’s a lot to unpack in this one, but before I do, I just wanted to say that I do think outrage has it’s place. Anger, releases cortisol in the brain, which cements memories. It’s a signal to the brain that this moment, is something to pay attention to. It is something that should be remembered and learned from. But then we have to move on. Long term cortisol levels in the brain have detrimental effects, like emotional dysfunction, and reduced ability to reason clearly. So while Anger and outrage have their uses, we should stay angry, lest we become outrageous.

“We cannot have a meaningful revolution without humor.”

—Bell HooksBeing cool and analytic gives the opposition (Authoritarians and Capitalists, and the stooges of bureaucratic middle-management, and Neoclassical economists) less ammunition with which to assail you when you make your points.

It is possible to be impassioned without forsaking logic and reason, and empirical analysis. Just like it is possible to remain cool and calm and still make intuitive leaps of abductive logic.

Hi Rowan,

First I want to confirm that you did see my full response to your post, and then I was hoping if you could clarify something. Are you suggesting that Dominant Pharmaceuticals, or any other powerful entities deliberately planned the Covid-19 Pandemic?

Don’t get me wrong, I have deep-seated dislike and enmity for those at the top of the power structures, but I think that planning of the Pandemic goes against the rituals of Dominant Capital. It is one thing to opportunistically prey upon crisis. It is an entirely different matter to create a crisis that can easily spiral out of control and result in the total destruction of power bases. I don’t think the Powerful, who are demonstrably risk-averse, would hazard such a risk, even for massive short term gains in wealth or social control.

Ok, So, Attempt number 2, should go better this time as I am saving as I go

1. The Science

The Vaccine

So while it is important to try and separate the science of Covid-19 Vaccines from the business of Covid-19 Vaccines, this is no simple task, since the science is bought and paid for by both Public and Private Sector money. mRNA vaccines spent about 5 decades in development hell. I mean this quite literally, since there were lots of fights over patenting issues, companies set up to try and profit from research, companies failing, companies being bought, a kind of musical chairs of company founders/scientists/researchers jumping ship to larger firms. Accusations of misconduct, both scientifically and socially… It’s an entire story all of it’s own.But around the turn of the decade (2010), 2 important things happened

1) UPenn sold exclusive patent rights for an mRNA process that resulted in Pseudodrine (which prevented the host body from seeing the foreign mRNA as an antagonist), for $300,000 to a small Lab-Reagent company now called CellScript, who have since made millions in sublicensing this patent to companies like Moderna, and

2) from the early 1980’s until 2012 Canadian Pieter Cullis and his team of researchers at University of British Colombia, developed Lipid Nano Particle tech, which forms the basis of the delivery platform for mRNA vaccines. By 2012, they had managed to develop the technology enough that mass production was possible. And this is when big money investors became interested. Cullis has started several small companies, and one of these is now privately valued at around $13mil, thanks to investment rounds based on ongoing research into his LNP tech.All of this meant that the day after the SARS-COV-2 Virus Genome was made publicly available, companies like Moderna and BionTech were immediately ready with their vaccines to begin testing. They did not want to waste any time in profiting from the global pandemic, and whoever made it to market first with a proven Vaccine, was going to rake in Billions in international purchasing contracts.

Preparation and forewarning

Virtually every science writer and journalist, at some point, had written a piece like “It’s not if, but when” with regards to a pandemic being an existential threat to humanity. I had read so many of these by 2018, that I included it in a podcast episode I did with a friend about existential risks. And yet, studies have found that not a single country, rich or poor, was prepared when the pandemic hit.Areas of research that were identified at the start of the pandemic as vital were impacts of quarantine, case and contact isolation, hand hygiene, face masks, public education about personal protection, therapeutics (antivirals and antibodies), and future vaccines. And these studies were rapidly conducted, and the findings were rapidly processed and collated and disseminated.

The first 6 months of the pandemic saw 100,000 research papers published in relation to Covid-19. (although estimates of the first 10,000 showed that only about 40% were original research, and the other 60% were mostly opinion pieces) It was seriously an unprecedented achievement for science.

But the result was a policy rollout of mismatched and counterproductive government and business policies that got so bad, that eventually, the only solution was lockdowns. This is the surface reading of lockdowns, but a long-view of the lockdowns shows that lockdowns led to stimulus spending, which predominantly benefitted a very small portion of the private sector, very disproportionately (1% of businesses reaped 25% of the $700bn reward) and the stimulus spending that went to households, triggered a spending frenzy that massively boosted the Consumer Discretionary sector, and the IT and Communications Sectors. So while it would unwise to attribute the lockdowns to a deliberate decision to assist Dominant Capital, it is not far fetched to say that poor governance, poor planning, and poor readiness, allowed for the optimal conditions for Capitalists to pounce on a crisis, as the have often done in the past.

2. Dominant Pharmaceutical Capital and their differential accumulation throughout the pandemic

Looking at the Pharmaceutical Industry through the CasP framework, we can see a number of very telling indicators showing how its Dominant players Accumulated Differentially.

1st, Mergers and Acquisitions increased 17% in the first half of 2020, which is a massive increase in breadth given the downturn taken by much of the rest of the economy.

2nd, Strategic Sabotage in the form of Patenting saw a 6.3% rise in BioTech and a 10.2% rise in Pharmaceuticals. So not only were they consolidating like crazy, they were also enclosing the access rights to a life-saving technology.

3rd, Depth of Capital Accumulation was also increased during this time, as Market Dominance and desperation by those with less power allowed the Pharma giants to vary their prices by region, and gouge the international market to extract as much profit from the situation as they could get away with

4th, The Direction and Pace of Industry was decidedly skewed toward broadening and deepening power. Vaccine Production facilities were largely outside of the regions where they were most needed, and this did not change, and has not changed, because to do so would reduce the power now held by the producer to get away with the 3rd point made above. From 2022, plans are being made to begin production in India and South Africa of mRNA vaccines, but this process has taken 2 years to come to fruition, and developing the production facilities up to par is going to take an additional several months. These delays, again served to strengthen the power-base of Dominant Capital.

5th, Weeding out Competition was very subversive throughout the pandemic, very specifically in the form of Media bias being propagated toward the Chinese Sinopharm vaccine. By painting China as the cause of the pandemic, and the source of the virus, western media was able to influence the majority of nations into rejecting the Sinopharm Vaccine in favour of Western Vaccines. With the result being that of all the big vaccine producers, Sinopharm was the only one that failed to accumulate capital at a net positive rate throughout the pandemic.

3. The Rest of the Dominant Capital Market and their differential accumulation throughout the pandemic

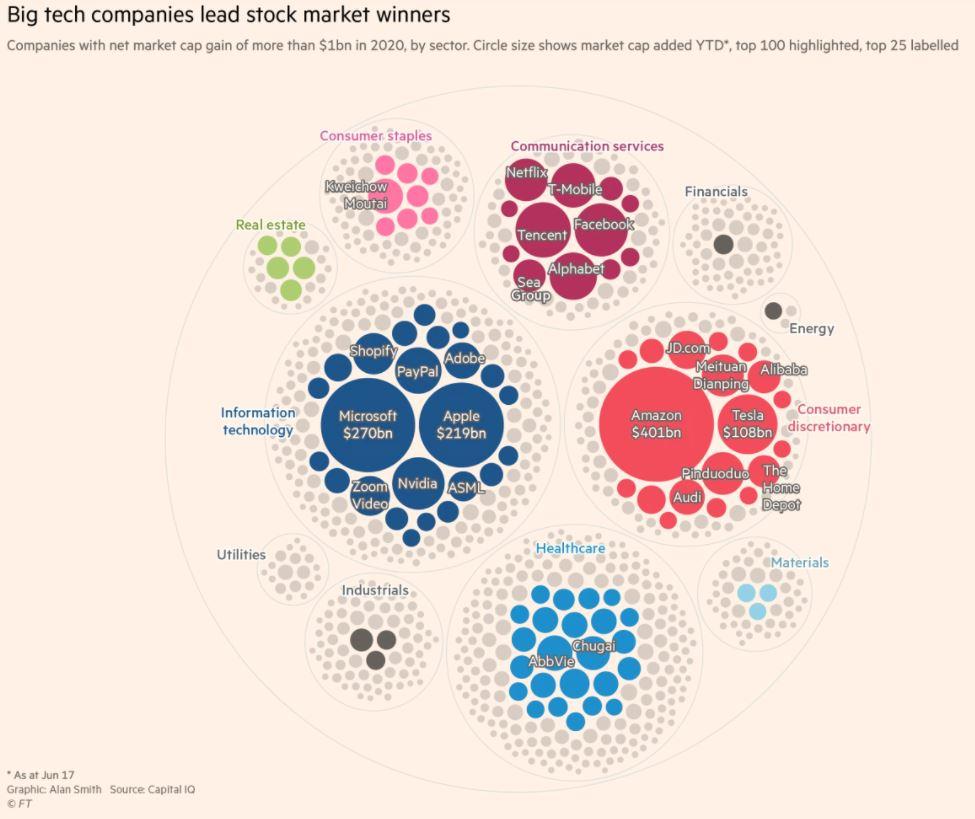

2020 was a banger year for Dominant Capital. the Financial Times did a breakdown list of “the top 100 winners of the pandemic“, and USA Today did a roundup showing that Billionaires added almost a trillion dollars to their combined income in 2020. Below, you can see the infographic of the big winners, dominated by Big Tech, Communications, Healthcare, and Consumer Discretionary.

It is important to note here that the same tactics employed by Pharma’s Dominant Capital, was also employed by the rest of the Dominant Capital playing field.

Mergers and acquisitions were down globally, but kicked back up in North America in the 3rd and 4th quarters of 2020, and as lockdowns were ended and economies reopened, a global supply chain crisis gave dominant capital all the excuse they needed to begin inflating their prices as the swung into a depth phase.

To what extent their actions can be attributed to an aversion to lockdowns, I feel is probably up for debate, given that there were a great many that benefitted from the lockdowns then, and will likely benefit again. The Industry that is most deeply hit by lockdowns, is Oil and Gas. 2020 was a terrible year for them, while 2021 was a fantastic year. So they will likely be the ones least eager to see and kind of lockdown be re-enacted. I don’t know how to check for lobbying activity in this regard, but it would be invaluable to know where the oil industry is spending their lobbying dollars.4. The State of Capital and its Support Structures for a) Accumulation of Capital and b) creating a Global Inequitable Vaccine Divide

As illustrated above, the state’s lockdown procedures were not running counter to Dominant Capital in all cases, and in many cases acted as a support structure for Dominant Capital’s accumulation practices. In addition to acting as a support structure via stimulus spending, eliminating competition that was not “too big to fail”, the state also enabled Dominant Capital accumulation by means of trade influence to ensure wealthy countries benefited more from changes in trade flows than did poorer countries.

In addition to support for differential accumulation, Wealthy nations created, in conjunction with Dominant Capital, a despicably large gap in vaccine equity. While rich and middle income nations are now at an average of 70% vaccinated, poor nations are still struggling at around 7%. and it is not just internationally that this wealth/vaccine inequity was perpetuated. Poor and marginalized communities in wealthy nations have also been disproportionately undervaccinated. The vast response to much of the criticism surrounding this point has been that poor and marginalized communities have shown a large Hesitancy to take the vaccines. But putting aside the fact that many of these communities have ample reason to distrust Pharmaceutical companies and Governments that have a long history of using and abusing them by dumping faulty or expired medications on them and using them as involuntary experiments, there is the question of the deliberate spread of counterfactual information that has resulted in the majority of the hesitancy. Which brings us to point number 5.

5. The Role of Misinformation and Disinformation in Expanding the Pandemic Problem

Many believe that the anti-vaccine community is a decentralized community largely spearheaded by concerned soccer moms that are terrified their children will develop Autism from the harmful chemical cocktails the state wants to force onto them. To some extent, there is some truth to this belief, because a large and vocal portion of the the anti-vaccine community is exactly this type of demographic.

But what is largely ignored is that these entities tend to act as boosters for the disinformation rather than the original source. Research done by the Center for Countering Digital Hate has found that the vast majority (over 70%) of all Vaccine Disinformation and Covid-19 Disinformation, originates from just 12 influential social media accounts. Now dubbed the Disinformation Dozen, and that within this group, the most prevalent voice is that of Joseph Mercola, an osteopath with an “alternative health” Empire he runs jointly with his wife, to the value of over $100million.

*************************************************************

So what we see is almost a perfect storm of conditions for the Power of Capital. Science enclosed by property rights, generating Differential Accumulation in the health industry, and sustaining the condition for the State of Capital to ensure further differential Accumulation by sectors outside of health, while simultaneous reinforcing global divides, deepening and broadening power bases, while the little emperors of pseudoscience re-enforce foundations for the global divides.

- This reply was modified 4 years, 7 months ago by Pieter de Beer.

It happens, and has happened to me before on other forums.

I should have saved the work in a word processor before posting, as I should have learned this lesson a long time ago.

C’est La Vie

I spent all day today typing up a response to this post, gathering information from various sources, and fleshing out my ideas… and when I went to submit… everything just disappeared.

Will try again I suppose

Basically my comment came down to this though.

The Covid Crisis analysis should be broken up into 5 Facets (while keeping in mind that all the facets have strong interlinks and overlaps)

- The Science

- Dominant Pharmaceutical Capital and their differential accumulation throughout the pandemic

- The Rest of the Dominant Capital Market and their differential accumulation throughout the pandemic

- The State of Capital and its Support Structures for the a) Accumulation of Capital and b) creating a Global Inequitable Vaccine Divide

- The Role of Misinformation and Disinformation in Expanding the Pandemic Problem

December 9, 2021 at 3:16 am in reply to: Is “Hype” Really an Elementary Particle of Capitalization? #247316Ok… so this seems to have gone down a strange turn. Scot, you seem to be suggesting (and please correct me if I am wrong) that Hype is a Power tactic that is nebulous and largely unmeasurable? if so, I would say that almost everything can be measured, unless we specifically define them in such a way as to make them unmeasurable.

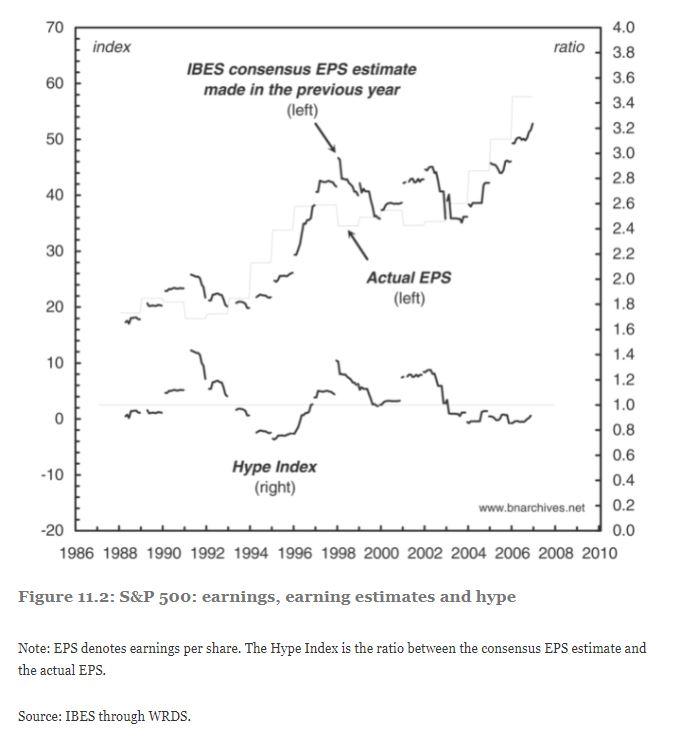

Hype, as defined by CasP, is a ratio that measures the difference between expected earnings, and realized earnings. EE/E

Long term observation of this ratio is the mechanism by which we are able to tell to what degree Analysts are being positive or negative about a valuation.

The Analysts are not the ones with the motives that need inspecting though… Analysts build their valuations and forecasts on various ratios and metrics, but there is always a level of hype that falls outside of the standard equations. If this were not the case, what we would see is an almost perfect match up of analyst predictions for expected earnings and the hindsight of realized future earnings.

This error-gap has only 2 possible explanations. Either the Efficient Market Hypothesis is correct, and information is embedded in the price, which was only known to inside traders who acted on that information, thus distorting price expectations (a position that is fundamentally unfalsifiable), or there is Market Hype at play. And given that we can actively see Market Hype occurring all the time (Elon Musk is a prime example with his tweets regularly affecting share price), my guess is that the Efficient Market Hypothesis is a bunch of hooey, and Hype needs further investigation.

in 2006, Alan Turk from Illinois Wesleyan University, produced a paper in which he formulated some of the most commonly used ratios, introduced industry controls, and then added in a model he developed for Hype.

Unfortunately, his was a once-off study, that looked at a very short-term time-span, during a very specific economic period. As a result, his Hype model did not have the expected outcomes, and only really worked for the Financial and Communication sectors, while showing little to no effect in other sectors. Had there been follow up studies done on all studied sectors, with repeated analysis at every quarter over a number of years, and with a related study of media content verbiage as a Time-series Analysis of all the Market Hype surrounding specific stocks, the data may have revealed the kind of granular Hype I was referring to earlier.

Nonetheless, I still think that given the large discrepancy between forecasts and actual returns, Hype needs further investigation.

December 7, 2021 at 5:03 am in reply to: Is “Hype” Really an Elementary Particle of Capitalization? #247297Hi Scot,

Your post really made me think, because I have very little experience in this arena. So I had to do a little digging to refamiliarize myself with the concepts being addressed.

My larger concern is that “hype,” like utils, snalts and “capital stock” cannot be definitively measured.

I think that part of the point made in CasP, is that none of it is really measurable in the absolute sense. That’s half the point. By hyping future earnings prior to earnings calls, the investors are then steered toward a desired share price.

Personally, I’ve never seen any Wall Street analyst include a “hype” factor in their discounted cash flow analyses of future earnings.

The way I understood it, Hype wasn’t something that could be seen in individual company data in the short term, and could only be identified in the long view because of the dramatic over/under estimation of value reflected in the Hype Index vs Expected Earnings Share data presented in the book. And it isn’t visible at the individual analyst level, because the analysts are all following each other’s lead, so to speak.

Perhaps one could argue that “hype” determines earnings growth projections, but those are typically explicitly stated or shown, usually are based on recent earnings growth, and typically taper down to some lower, terminal growth value that is used to calculate a terminal value of the earnings. I have seen stocks (e.g., Tesla and, previously, Amazon) that seem wildly over-valued compared to fundamentals, and that phenomenon is of interest, but over time an overvalued stock can to an undervalued stock, and vice versa.

This sounds like a decent enough summation of what is described in the book. It is not that Hype sets the price, but that it influences investors/shareholders in order to guide them toward a desired price.

Regardless, the concept of “hype” does not seem to add any value to CasP in a broad sense

I have to disagree, based on my admittedly limited understanding. If the herd mentality of Analysts is demonstrable (as seen in the above chart), then this provides a frame of reference with which to approach investigation of hype at a more granular level

although it might when focused on specific stocks that seem particularly inflated or deflated from a nominal expected value. In that kind of case, “hype” may really be a conscious manifestation of power, i.e., dominant capital is rewarding (or discouraging) a particular company to encourage (or discourage) greenfield investment in competitors.

So if we can (hesitantly) classify Hype into 2 categories, Generalized, and Granular. Then we can focus down to see the agency behind Granular Hype. Generalized Hype becomes a Particle of Capitalization as viewed at the overall market level, while granular hype can be described more closely as a concept of power (COP). A mechanism for the pulling of strings.

This is where it becomes important to know the actual power players in the game, and once identified, we can then apply the CasP framework to the Power Players overall strategies and tactics for a clearer understanding of individual motivations. But I don’t think that the CasP framework is that clearly refined as yet, before the framework can be applied at such a level, we would need a comprehensive understanding of most, if not all, of the Concepts of Power being deployed throughout the Capital Power regime. And so far, I don’t think we have even gotten a comprehensive list of COPs, let alone a detailed analysis of their individual or collective effects.

Loving this list.

Some Comedy entries I think could be added

Clueless (1995): because it is a story about how a ruling class girl constantly interferes with the lives of others, especially those that are ‘beneath’ her station. A good allegory for how absentee owners creorder society today. (it is technically a modern retelling of Jane Austin’s Emma, which explains the very pertinent Power Dynamics)

Office Space (1999): because it very viscerally looks at the hierarchical inequalities of power, and the constant resistance to power. How small acts can cause serious damage to power structures. But ultimately, without constant pressure, the system rebounds, and is ultimately reinforced by systems co-opting resistance

American Psycho (2000): because it satirically represents the capitalist need for enacting violence on others in order to externalize the pain of constantly having to internalize the unempathic interactions of capitalism, and the superficial expression of intellectualist musical artistic critique.

December 1, 2021 at 1:43 am in reply to: Inflation is always and everywhere a redistributional phenomenon #247263I’m not a data scientist, so have little to contribute to this thread. But i do find it fascinating. So i went looking to see who else has looked at similar lines of thought.

Honestly the closest I could find is what I think might be a White Paper by Brian Lowell of McKinsey insights

and as White Papers go, it is very sparse on Sources, but here’s the related McKinsey article

Not sure if this is of any help to anyone

November 30, 2021 at 12:10 am in reply to: Regulation as support structure for the Power of Capital #247249If I were to start in on this kind of project, I would focus on the Sherman Antitrust Act of 1890 and follow the thread of federal antitrust law and enforcement through to the present day. We know many of the consequences, e.g., the rise of the modern corporation to avoid antitrust laws, breaking up AT&T, curtailing Xerox’s IP rights, etc., and we can find others through applying CasP logic. Moreover, the Sherman Antitrust Act began as a standalone, bright line law whose enforcement was gradually pushed to administrative agencies, many of which have become captured by the industries they are supposed to monitor.

Sherman Antitrust and a ton of associated literature is already on my reading list.

I was going to mention this, as well. For example, much of the “regulation” we see in the U.S. today is actually being performed by courts (not legislative or administrative bodies), particularly by judges influenced by the Law and Economics movement, which I’d argue is the dominant legal philosophy today.

Regulation being done by courts, rather than agencies, seems like a counterintuitive idea. To my understanding, legislators and agencies are tasked with codifying the rules. The agencies are expected to enforce the rules. Courts are meant to adjudicate transgression of the rules. Obviously the judicial interpretation of rules holds massive sway on how the rules are applied in reality, but that would only be one piece of the puzzle right?

Theoretically, the full regulatory capture would encompass Legislators, Agencies and the ideological influence of political economy theorizing that affects judicial interpretation.

For Dominant Capital to effectively use Regulation as a support structure for the Power of Capital, they would need to ensure that the 3-pronged approach be as robust as possible.

Other potential areas/topics would be environmental protection laws

Environmental protection regulation and the associated Tort Law will definitely be a fascinating aspect of this entire journey.

and copyright laws (there is a massive schism in patent law that has shaped an oddly schizophrenic regime of patent enforcement, but that’s interesting, too;

IP laws are equally fascinating, but I’m hesitant to go there, because it feels more like the domain of Strategic Sabotage

how does dominant capital deal with civil wars among capitalists?), the histories of which are pretty well-established and are likely to yield new insights if subjected to CasP analysis..

The Civil War in Dominant Capital is actually something I enjoy thinking about. Given the imperative for Differential Accumulation, it makes sense that Dominant Capital would wage war on Dominant Capital. But this, also, would be a topic for another day. The regulation and capitalization stuff will have me busy for months yet.

November 29, 2021 at 11:46 pm in reply to: Regulation as support structure for the Power of Capital #247248Thanks for the feedback Jonothan,

I added the caveat about the categories not being exhaustive or necessarily accurate, mainly because I have not yet read the necessary literature, but also because the eventual categories would need to be mappable and testable. I had not even considered the multiple consequences yet, but it makes perfect sense. All actions have multiple intended consequences, and multiple unintended consequences. Mapping the unintended consequences would be supremely difficult, if not outright impossible, but I intend to give it a go nonetheless.

It is encouraging to know that you think this might be worth pursuing. My thinking is simply that regulation as it currently exists must be a COP (Concept of Power) under the current Capitalist Mode of Power, and that its evolution should be observably (as illustrated by early studies of it’s effect on railroad stock prices)

November 29, 2021 at 11:32 pm in reply to: Regulation as support structure for the Power of Capital #247247Thanks Scot,

I might limit the scope of the article I end up writing, but I want to first collect and read all the literature I can on the subject.

Your resources are a great start.

-

AuthorReplies