- This topic has 10 replies, 5 voices, and was last updated January 10, 2023 at 2:51 pm by .

-

Topic

-

Firstly, as far as I can see, this hasn’t been covered in the forum yet but apologies if this has been addressed elsewhere.

My question is about how broadly and loosely can we use the terms (differential) breadth and depth before we’ve completely strayed from CasP theory? These terms seem to have a lot of potential for understanding power more generally so I’d like to clarify their strictly CasP usage.

Back in October 2021, Cory Doctorow posted a thread on Twitter discussing Chris Mouré’s terrific “Soft Wars” research. In the thread Cory provides a perhaps less than pure CasP definition of breadth and depth:

There are two strategies for accumulating power: one is “breadth”: to grow the market as much as possible, thus accumulating profits faster than the average competitor, eventually taking a commanding lead over the rest of the field.

The other strategy is “depth,” dominating your sector by capping its growth and then taking as much business away from your rivals as possible – if the industry is crucial (like, say, software), then dominating it gives you a LOT of power, even if you’re strangling it.

The Bichler and Nitzan twitter account replied clarifying the terms as per their proper use in CasP:

‘Breadth’ — raising employment faster than the average

‘Depth — raising profit or capitalization per employee faster than the average.

Multiplying breadth x depth tells you whether total profit or capitalization beat the average.

Breadth measures the *relative size* of the capitalized organization.

Depth measures the *relative power per unit of organization*.

Breadth x depth measures the *overall power* of the capitalized organization.

Differential breadth and depth can be increased through green-field growth, mergers & acquisitions, stagflation and cost cutting.

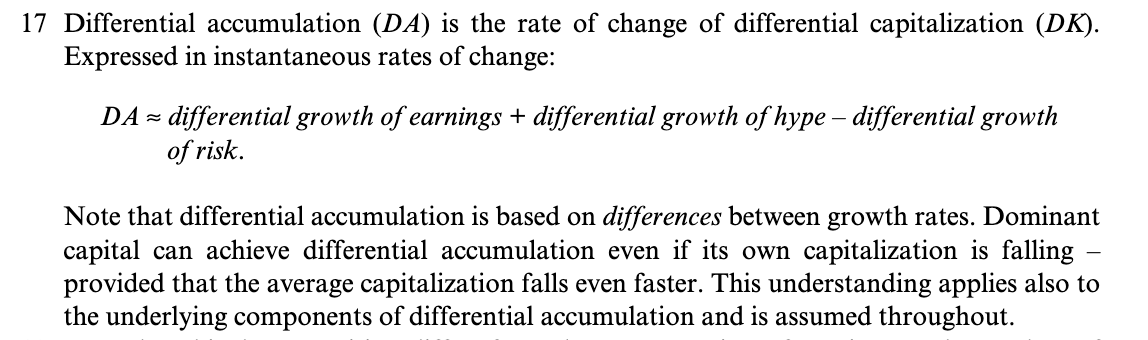

Economists glorify growth and cost-cutting, but differential accumulation is driven mostly by M&A and stagflation.

Why only count employees?

Why is it breadth and depth only measured in terms of employees and earnings per employee? Is this simply because it is easiest to measure?

Both external and internal breadth result in the control (employ/ownership) of both more employees and capital, and potentially other factors like land or market share more generally. Similarly with external and internal depth, both increase profits or capitalisation relative to employees, capital, land, etc, at least as far as I can tell.

The measurability has clearly been fruitful in empirically revealing the internal breadth to external depth cycle, so I’m certainly not questioning the validity of the strict definitions as they currently stand. But is there scope for insight on including more factors or focusing on different factors?

I am also a tad confused about this definition offered in the Bichler and Nitzan tweet as I had it in my mind breadth/depth mainly focused on capital accumulation rather than employees. A quick skim of those sections in the book hasn’t clarified this but more than likely I’m missing something.

Cogs in the Megamachine?

I remember CasP builds on Lewis Mumford’s idea of the “megamachine”, the social technology of large hierarchies. In this framework it would make sense to consider people employed in a firm to be “units of organisation” within the “capitalised organisation” – but is that the thinking behind the approach? That only people count in the equation of social power because they’re the only “factors” of production to which social power applies? I guess machines, IP and land don’t think or act, and their ownership is a wholly social matter in that it only exists with thinking, acting people.

Hard CasP vs Soft CasP?

I wonder if there’s a more “Soft Casp” way of seeing power accumulation that, while certainly less empirically inclined, might offer ways of understanding or at least speaking of power more generally.

For example, we could speak of a tyrant pursuing zero-sum growth of the (internal) breadth of their power over [insert object of domination here]. Similarly, we could speak of a tyrant who, feeling threatened in their power, decides to go for broke, stretching and pushing everyone around them to maximise the (external) depth of their power.

This would clearly be the least formal use of the terms, but if thats the limit, how much more specific do we need to be to get back in CasP territory?

Are there other factors besides employees worth considering as part of their own differential breadth and depth regimes in capitalism?

Lastly, how useful might the internal/external, breadth/depth matrix be to understanding other modes of power I wonder?

- You must be logged in to reply to this topic.