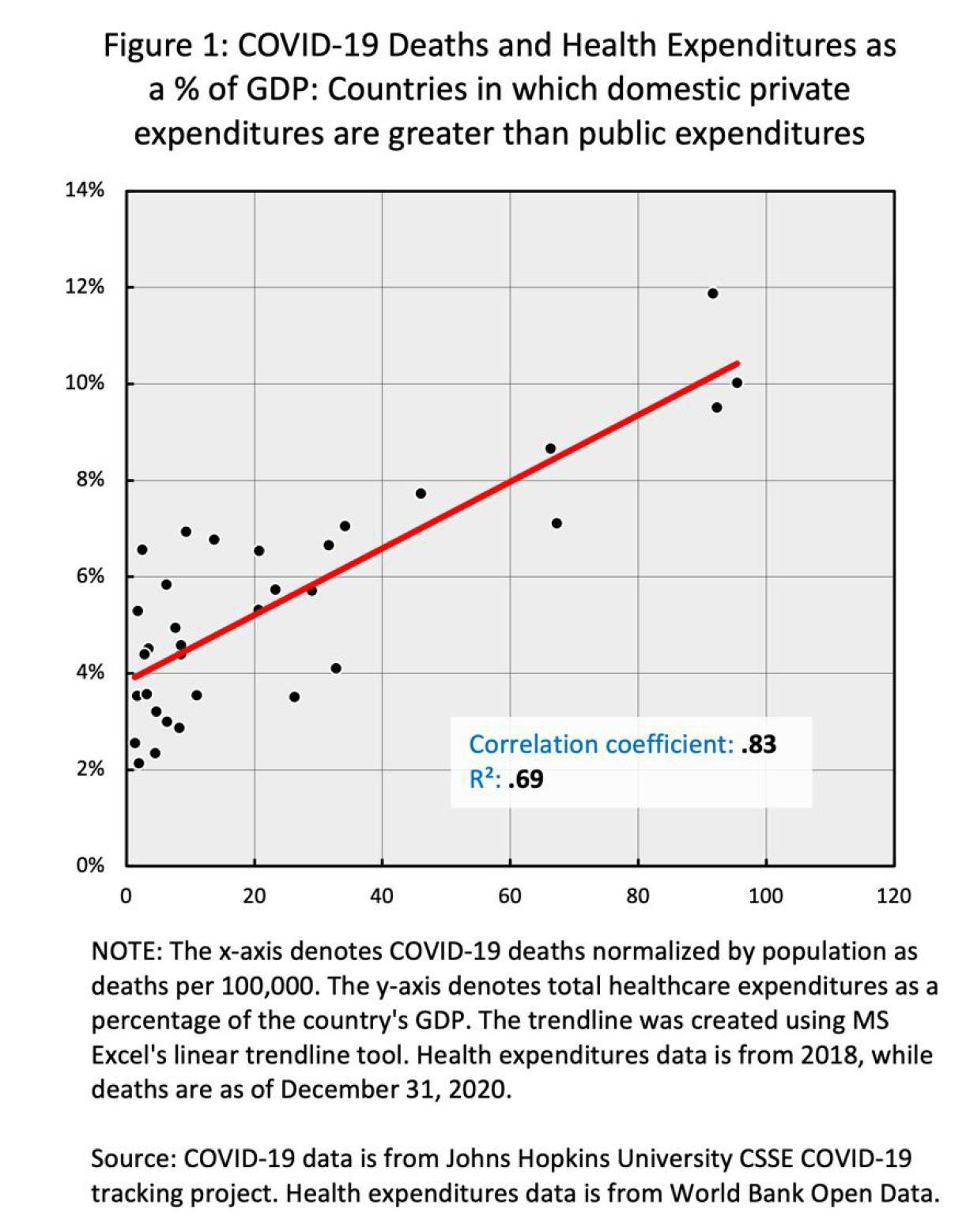

I was hoping to get some feedback broadly in terms of these questions: 1. Do you think the approximation of health financing ratios to ratios of public/private control of health care systems is warranted? What additional information or questions answered do you think might strengthen or weaken this assumption? 2. Is the explanation and treatment of the quantitative analysis comprehensive enough/too comprehensive (and how)? What further information/calculation/chart illustrations would you like to see (e.g. other variables, larger sample size, etc.). Is there anything that is unnecessary or superfluous? 3. Any other notes on the empirical evidence, including ideas of how to expand the study? Many thanks in advance!

For the duration of 2020, COVID-19 was an untreatable disease and largely remains so now. You can get vaccinated, but if you contract COVID-19, the only question is whether you survive it. By the end of 2020, the US had approved remdesivir and monoclonal antibodies as treatments, but I don’t believe they are broadly deployed even today. Given this inability to treat the disease, how do we measure quality of care or efficiency? Alternatively, if neither the quality of care nor the efficiency of its delivery affects the outcome, why do they matter?

Responding to your questions:

1. Does the mix of non-profit v. for-profit private providers affect your approximation of health financing ratios? I know that you chose to leave the US out of most of your analysis, but the American health care system is the only one I have studied. According to the Kaiser Family Foundation, in 2019, only 24% of American hospitals were for-profit entities, 57.3% were non-profit entities, and the remainder were government entities (state or federal). Nominally, then, 76% of American hospitals are not driven by the demand for differential accumulation. To be clear, I believe that it can be shown that an increasing number of non-profit hospitals are managed exactly like for-profit hospitals, but the profits are distributed as salaries and bonuses to management, not as dividends to the owners.

2. The explanation and treatment of the quantitative analysis seem comprehensive enough based on your assumptions and the limits you placed on your study. If you had included the US healthcare system in the meat of your results, I probably would have had something to say because I don’t think differential accumulation in US healthcare manifests itself purely as a strategic scarcity (i.e., the most common form of sabotage). In fact, the real scam in US healthcare is price fixing, or more precisely “annual price increase fixing,” between insurers and providers. The whole point of the US healthcare system appears to be transfer what little wealth elderly Americans have to dominant capital (over 60% of all healthcare costs are incurred by people 50 and over).

3. I have some ideas, but they’re probably more relevant to a different study than the current one. That said, to the extent you do discuss U.S. healthcare costs and COVID-19 outcomes, you may consider consider comparing outcomes among the states themselves, as the per capita data for both healthcare costs and COVID-19 deaths are available. Unfortunately, the CMS’s per capita healthcare costs data seems to end in 2014, but newer data seems to be available elsewhere.