Forum Replies Created

-

AuthorReplies

-

October 7, 2022 at 7:38 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #248399

If capitalization is the only pricing mechanism in capitalism, this would imply that what Marx calls exchange value is, in fact, just discounted use value, i.e., exchange value is capitalized use value.

Why do you say that discounting capitalizes use value (rather than power)?

Capitalization is the discounting to present value of risk-adjusted expected future income. Here, by “use value” I mean an employer’s expected future income arising from the work contributed by an employee, and by “exchange value” I mean the wages paid by the employer to the employee for that expected future income. If that is a reasonable way to look at things, any difference between the employer’s future income and the employee’s wages arises from the act of discounting the employer’s expected future income to present value; i.e., wages can be considered the capitalization of the employee’s contribution to the employer’s expected future income.

Is that reasonable, or am I missing something?

Of course, wages and wage labor predate the emergence of capitalism by thousands of years, which implies that capitalization predates capitalism by thousands of years.

Capitalization was first used, embryonically, sometimes in the 14th century; was first formalized, if only tentatively, in the middle of the 19th century; and came into common use and full dominance in the second half of the 20th century. You can argue that capitalists were always forward-looking, and that the prices of their assets represented, or at least reflected, however unknowingly, future expectations. But I find it hard to think of the daily wage in Sumer as capitalizing something.

If an employee’s wages can properly be viewed as expressing the discounted present value of an employer’s risk-adjusted future income arising from the employee’s contribution, then the daily wage in Sumer can be said to have capitalized the employer’s expected future income.

Arguably, Marx’s surplus does not exist, if employees’ wages represent the employers’ discounted future income arising from the employee’s contribution. This is because wages, at least theoretically, represent the fair value of that contribution according to the logic of capitalization.

This does not mean that capital does not symbolize power (energy, actually, as capital and energy are stocks, while power is a flow), nor does it mean that workers are not exploited, but I think it does imply there is a source of social power anterior to capital, i.e., something caused non-capitalists to accept the logic of capitalism and its pricing mechanism of capitalization.

- This reply was modified 3 years, 9 months ago by Scot Griffin. Reason: Added final two paragraphs

In capitalism, power is priced in and traded for $, and since in principle prices are the same for everyone, Musk and you will buy the same power for the same price. But this universality does not imply that Musk and you have the same power. If Musk owns $232 billion and you own $232 million, he is 1,000 times more powerful than you — even though both of you face the same prices. In general, capitalists grow more powerful not because they buy for less than others, but because they change the world in such a way that makes the price of what they own rise faster than other prices.

No, the principle prices are not the same for everyone, and you have proved it yourself through CasP.

Pricing in what economists (and political economists) call “the market” is based on cost plus mark-up.

Pricing in financial markets (what you call the State of Capital and I call “the Market”) is based on discounted future earnings.

All of this is right there in your theory, CasP theory. The market prices the past while the Market prices the future as “the state” (however constituted throughout history) monetizes and arbitrages the value of labor over time.

Yes, to the extent that capitalists avail themselves of the market, they are subject to its pricing methodology, but the whole point of having “fuck you money” (aka capital) is to not be subject to the market in the same way as the masses, i.e., the point of being a capitalist is to be free from the market; to be autonomous and a citizen of the Market, not a subject of the market. Both economies/nomoi/poleis are real, but they are not the same, just as capital and money are not the same, even though each can be transformed into the other through the membrane/machine of Finance, which resides in the Market (and stands above the market like a lord; it is the Market that rules, not the capitalists).

Within the nomos of the Market, it does not matter to a capitalist that Musk is more powerful than he/she because the capitalist owes Musk nothing. Within the nomos of the market under the modern money regime, everything is debt , which means the debtor is “less than” his creditor and owes him a portion of his labor, just as the laborer is “less than” and owes the capitalist a portion of his labor for having a job. Debt within the market is a self-replicating construct that creates hierarchies within the market, hierarchies that capital ultimately controls through the Market and capital (the One Ring of debt). Within the nomos of the Market, debt is just a way to share power, not to cede it. It just isn’t the same thing as debt in the market, which is why we have Sanders and Warren pushing for a wealth tax in view of the fact that billionaires and hundred millionaires can collateralize their capital in the Market to live their lavish lifestyles free of taxation and real cost.

I do agree with you that capitalists writ large control the market in a way that ensures the Market grows faster than the market (aka Piketty’s r>g), but the basic mechanism of power for millennia (and to this day) has been debt within the market, which ensures the masses are subjugated. Capital is what has allowed both the Market and the market to grow without conquest (although it is no impediment to conquest) by allowing wealth to be hoarded as capital without affecting the money in circulation (unless and until there is a financial crisis, whereupon austerity is imposed to beggar the masses and make the capitalists “whole”).

The dichotomy of politics (the market) and economics (the Market) is true for capitalists and false for the masses, and that is one of the many “double truths” (double lies) of neoclassical economics. In this case, you correctly reject the dichotomy as false for the masses, but you miss that it is true for capitalists. For more on double truths, see Philip Mirowski’s work regarding neoliberalism.

To be clear, I would have not seen the double truth of the dichotomy but for you and the many theorists who have advanced CasP to where it is today. I think CasP is the most viable theory of social power we have, it just needs to wrench itself completely free of the framing of classical political economists, including Marx himself (not just from the neoclassicals). When Thatcher told us “there is no society,” she was speaking a truth that had been suppressed for thousands of years, one that you agreed with on Twitter today by arguing that capitalists stand outside of society. I would put a finer point on it and argue that capitalists are to society what the shepherd is to his sheep. I say this as an observation, not an endorsement.

- This reply was modified 3 years, 9 months ago by Scot Griffin.

- This reply was modified 3 years, 9 months ago by Scot Griffin.

If we can ignore the exploited/subjected classes, is capitalism a democratic or horizontal creorder (at least among capitalists)?

The Capitalist Class is, itself hierarchical. Its internal power structures are inherently differential, and as such it has it’s own levels of status. All capitalists do not have equal power within their class, even if the capitalists may seem to the average worker to be on par with other capitalists, from the vantage point of the lower strata.

I agree that capitalist firms that sell goods and services at a mark-up align into hierarchies, but I don’t believe that is the case for the human beings who make up the Capitalist Class.

The fact that we can use CasP to rate and rank individual capitalists of the Capitalist Class by their relative power does not mean they apply the power between and amongst themselves to create or perpetuate hierarchies. The fact that a football team is ranked first in its table does not mean football teams ranked behind it owe (or show) the team who is in first place any fealty or favor.

Consider that in the stock market, where capitalists interact directly to exchange and transform their power, for every attempt to sell shares of stock there is a bid (from the buyer) and an ask (from the seller), and the difference between the bid and ask is the spread. No stock sale will occur unless one or both of the buyer and the seller crosses the spread and they both to agree on a sale price. A seller who is a billionaire cannot use his differential power to require a buyer who is a millionaire to cross the spread, i.e., the seller does not have the ability to add mark-up to the market price and expect a sale anyway. Any exchange that occurs is fully horizontal.

September 27, 2022 at 8:15 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248357I think that theorizing a “State of Capital” does not go far enough, that it would be better simply to focus on understanding and studying the Market as sovereign and relegate the modern state to the Market’s subject, as we all are (including capitalists).

The study of the “state of capital” is in its infancy, and I doubt you can predict its potential reach and likely insights. Having said that, you are more than welcome to make the “Market” the supreme subject and see if it offers different/better insights.

And I’d prefer to jettison words like “ruler,” “ruled,” “citizen,” and “class” to focus entirely developing a new taxonomy based on differential power, which I think is more likely to lead to insights that eliminate such power altogether.

We scarcely refer to “citizens” and “classes”. I’m not sure, though, how one can speak of differential power without differentiating rulers from ruled.

Thank you, Jonathan. Between your responses here and your recent comments on Twitter, you’ve convinced me that capitalist power is not confidence in liquidity. You have also given me a deeper appreciation of the power-fear dialectic and its purpose. That said, I think developing a market-centric version of the power-fear dialectic could provide additional utility, and I will post a proposed market-centric power-fear dialectic as a new topic on the forum once I think I have something worthy of everyone’s time. Thanks again. –Scot

- This reply was modified 3 years, 10 months ago by Scot Griffin. Reason: corrected spelling error

Your point about capitalists aiming to preserve their wealth by ensuring their return on capital exceeds inflation makes sense. Although would this not generally require them to also beat the average?

I think we need to distinguish between individuals and firms. They’re entirely different, and CasP focuses on firms (“dominant capital”), not individuals. As among individuals, some people just want to preserve capital and play it safe, some want to “beat the average,” and others try to balance between the two. The Capital Asset Pricing Model (“CAPM”), which is the basis of CasP’s insight regarding beating the average, was developed to provide a way for individual investors with different goals to understand which investment opportunities best suit their investment goals, which is often called a “risk profile.”

If Jonathan Nitzan, Shimshon Bichler, and Blair Fix (e.g. https://economicsfromthetopdown.com/2021/11/24/the-truth-about-inflation/) are correct that inflation is driven by power struggles within dominant capital to raise prices faster than their peers, then doesn’t it follow that those whose accumulation exceeds this (average) rate of inflation will also beat the average in terms of differential earnings and capitalization? Cheers, Adam

I think the assessment that inflation is driven by the desire to raise prices faster than peers is overly simplistic and incorrect. We need to think in terms of things like supply chains (or value chains) instead of just the prices end consumers see. Vendors, especially vendors to dominant capital, are generally loathe to raise their prices for fear of getting locked out of the next opportunity. That’s why prices are “sticky” or “inelastic.” To me, inflation like we are seeing today is combination of supply chain problems and the confidence of entire supply chains that their customers will have no issue absorbing the increased costs and passing them on (with additional markup) to the end customer.

An important lesson I learned at Intel was everybody in the supply chain for consumer product, e.g., a personal computer, is competing for its share of the total profit margin, and their relative power determines their share. Consumer products get priced based on what the marketing folks determine consumers will pay. One of the projects I worked on as an IP attorney for Intel was the Intel Web Pad, which was basically the iPad a decade before Apple launched it (but nowhere as cool or full featured). Intel scrapped the Web Pad because LCDs were too expensive at the time for any Web Pad maker from getting the profit margin needed to justify making the product. To be clear, Intel did not want to make and sell Web Pads itself; it wanted other companies to use its reference design and buy Intel chips to stuff them with. As a sophisticated end customer in its own right (Intel plays rough with its vendors), Intel realized it could not get the margins it wanted and leave enough for the maker of the Web Pad, and so the Web Pad was never commercialized.

September 24, 2022 at 10:12 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248348I think “confidence in obedience” collapses too many disparate issues into a singularity, obliterating any opportunity to distinguish between those issues and understand their differences.

Yes, “confidence in obedience” is a way of describing the totalizing meaning of capitalized power (see Questions 15-16 in ‘The Capitalist as Power Approach’).

Do you believe your Power Index directly measures confidence in obedience, or do you view it as merely indicative of it? I’ve gone back to the paper in which you first introduce the Power Index, but your assertions and reasoning are more logical than empirical.

I’m not sure, though, how the existence of this abstract notion is “obliterating any opportunity to distinguish between those issues and understand their differences.”

Abstraction destroys the ability to study details that are ignored or eliminated for the sake of simplification. You can’t look at what you aren’t allowed to see.

This where I think CASP’s outright rejection of the politics v. economics duality is problematic. I have always agreed with you that this dichotomy is a false one, that politics and economics are inseparable, but I also think we have to accept that this dichotomy, as false as it is, is a normative myth that has real power over people’s thinking and drives the formation of capitalist institutions. Whether we treat the state and Finance as separate entities or lump them together as “the state of capital,” the two operate in concert towards the same ends, but they operate differently and independently according to the normative myth and false dichotomy of politics v. economics.

I realize that we don’t share the same views on this matter, but I don’t think that we reject the politics-economics duality outright. Here is what we write on pp. 29-30 of Capital as Power:

To sum up, then, both neoclassicists and Marxists separate politics from economics, although for different reasons. The neoclassicists see the separation as desirable and, if handled properly, potentially beneficial. By contrast, Marxists view the distinction as contradictory and, in the final analysis, destructive for capitalism. Yet, both conclusions, although very different, are deeply problematic — and for much the same reason. The difficulty lies less in the explanation of the duality and more in the widespread assumption that such a duality exists in the first place. Even E. P. Thompson, a brilliant historian who was otherwise critical of Marxist theoretical abstractions, seems unable to escape it. Writing on the development of British capitalism from the viewpoint of industrial workers, he describes the class socialization of workers as ‘subjected to an intensification of two intolerable forms of relationship: those of economic exploitation and of political oppression’ (1964: 198–99). In this dual world, the industrial labourer works for and is exploited by the factory owner — and when he organizes in opposition, in comes the policeman who breaks his bones, the sheriff who evicts him and the judge who jails him. Now, this bifurcation is certainly relevant and meaningful — but only up to a point. From the everyday perspective of a worker, an unemployed person, a professional, even a small capitalist, economics and politics indeed seem distinct. As noted, most people tend to think of entities such as ‘factory’, ‘head office’, ‘pay cheque’ and ‘shopping’ differently from the way they think of ‘political party’, ‘taxation’, ‘police’, ‘military spending’ and ‘foreign policy’. Seen from below, the former belong to economics, the latter to politics. But that is not at all what capitalism looks like from above. It is not how the capitalist ruling class views capitalism, and it is not the most revealing way to understand the basic concepts and broader processes of capitalism. When we consider capitalist society as a whole, the separation of politics and economics becomes a pseudofact. Contrary to both neoclassicists and Marxists who see this duality as inherent in capitalism, in our view it is a theoretical impossibility, one that is precluded by the very nature of capitalism. To paraphrase David Bohm (1980), from this broader perspective, the politics–economics duality is not a useful division, but a misleading fragmentation. It cannot be shown to exist — and if it did exist, profit and accumulation would cease and capitalism would disappear. The consequences of this entanglement for capital theory are dramatic. As we shall demonstrate, without an ‘economy’ clearly demarcated from ‘politics’ we can no longer speak of quantifiable utility and objective labour value; and with these measures gone, neoclassical and Marxian capital theories lose their basic building blocks. They can observe that Microsoft is worth $300 billion and that Toyota pays $2 billion for a new factory, but they cannot explain why.

Any disagreement about this dichotomy is more a matter of degree than substance (we both agree it is false, but I think it remains useful to consider). Thanks for reminding me of the above language from your book. I was thinking of some of your more recent polemics against neoclassical and Marxist economics.

You write that:

Next to the capitalists themselves, it is the states whose potential “disobedience” is most concerning to dominant capital.

Yes. Conflicts within dominant capital, which we think of as a complex network of big capitalists, large corporations, government organs and so-called policymakers, are crucial. But in our view, these inner-class conflicts are tied to and delineated by the conflict between the rulers and the ruled. If this latter conflict did not exist or was insignificant, the share of profit in national income would have been far higher, the laws would have been very different and potentially far harsher for the underlying population, violence would have been more extreme, etc.

When I first read CasP (the book), it seemed to me that you and Bichler had established a new paradigm, a true break from how we understand political economy. I still believe that, and I realize now that the elements of current CasP theory that I find chafing are those that borrow too heavily from the old paradigm and seem, at least to me, to hold CasP back from achieving many of the goals you state in your 2015 paper “The CasP Project: Past, Present, Future.”

For example, I think that theorizing a “State of Capital” does not go far enough, that it would be better simply to focus on understanding and studying the Market as sovereign and relegate the modern state to the Market’s subject, as we all are (including capitalists). The ruler is the Market, not the capitalists, but the capitalists have rights and privileges within the Market (are “citizens” of the Market), while the vast majority of people do not even have access to the Market because they must spend everything they have in the market for commodities to survive and so cannot afford to accumulate the capital necessary to enter the Market, i.e., to become a citizen of the State of Capital instead of a mere subject. The difference between capitalists and everyone else is the power they derive from having enough freedom from the market to be members of the Market, which is why they fear the Market disappearing if liquidity disappears.

In this sense, I believe that capitalist power does not derive from confidence in the obedience of the ruled but from confidence in the continued rule of the Market. And I’d prefer to jettison words like “ruler,” “ruled,” “citizen,” and “class” to focus entirely developing a new taxonomy based on differential power, which I think is more likely to lead to insights that eliminate such power altogether.

As an aside, I feel MMT, which is an entirely different thing than CasP theory, suffers from similar problems arising from the use of language and concepts of the former paradigm, but MMT’s wounds are self-inflicted because it insists on interpreting the history of classical money to pretend it was just like modern money, which Colin Drumm has disproven. CasP’s reliance on the old paradigm seems to be a mix of habit and a sincere desire to explain the new paradigm in a way that your peers could understand (even if they ultimately refuse to do so).

September 13, 2022 at 9:08 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248332And this is where CasP’s claims about power and confidence in obedience come in. To earn a profit, corporate owners must exert their power over society. And to provide the liquidity needed to price this power, they must be confident that society will continue to obey them – because if it doesn’t, future profits will falter along with prices. I can go on to talk how risk and the normal rate of return are also anchored in power, but I think my point is clear.

“Society” is another traditional term that we need to revisit. Do we even have a society, in the traditional sense, within the capitalist mode of power? Or are we just using the term to refer to a set of people commonly living within the geographical boundaries of a state?

One could argue, and in some ways you do, that confidence in liquidity and confidence in obedience are effectively the same thing because the former implies the latter, but I think “confidence in obedience” collapses too many disparate issues into a singularity, obliterating any opportunity to distinguish between those issues and understand their differences.

At least with “confidence in obedience,” you begin with the domain over which dominant capital has direct and complete control: Finance and the Market (which we can also think of as Business). The ruled don’t occupy this domain because they don’t have the money or capital needed for meaningful access. Instead, the ruled occupy the domain directly controlled by states and the laws they enact to create Industry and the market for services and commodities. Yes, Finance does exert influence over these states, but influence and control are two different things. At the end of the day, it is the states who must act to ensure the ruled obey their laws.

This where I think CASP’s outright rejection of the politics v. economics duality is problematic. I have always agreed with you that this dichotomy is a false one, that politics and economics are inseparable, but I also think we have to accept that this dichotomy, as false as it is, is a normative myth that has real power over people’s thinking and drives the formation of capitalist institutions. Whether we treat the state and Finance as separate entities or lump them together as “the state of capital,” the two operate in concert towards the same ends, but they operate differently and independently according to the normative myth and false dichotomy of politics v. economics.

My preferred approach is to think of the state as an instrument of dominant capital, a tool for creating the institutional violence of the market and punishing those who disobey or seek to escape it. But states do maintain some level of independence, as they must to maintain the illusion created by the normative myth of politics/economics. Next to the capitalists themselves, it is the states whose potential “disobedience” is most concerning to dominant capital. As long as a state ensures that its ruled are reduced to a commodity that can be exploited by capital, dominant capital does not particularly care what the state does to its ruled. Commodities are incapable of obeying or disobeying dominant capital; they exist to be exploited and nothing else.

While the ruled are citizens of their respective states, they are not citizens of the state of capital, where they are at best metics, at worst slaves.

In any event, if power is confidence in the obedience of the ruled, and the Power Index reflects and measures that confidence, it should be easy to use historical events to explain what caused observed changes in confidence as reflected by the Index. For example, what were the ruled up to that shook dominant capital so much it resulted in the Panic of 1907? What about the Great Recession and the austerity that followed? One would think austerity would just enrage the ruled even more, but it seems to be a go-to strategy for dealing with financial crises.

September 11, 2022 at 10:19 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248329“Capitalists are not “rulers” in the traditional sense. They do not issue or enforce laws, they set prices and rely on the Market to intermediate everything, including their own power. ” – Scott Griffin. This statement is qualified by the term “traditional” which isn’t defined but I assume it means state power (by monarch or parliament for example), though it could also mean outright violence which has been rather traditional too, for all of chieftains, monarchs and states. Modern dominant capitalists fund candidates, “capture” laws and regulations (regulatory capture) and lobby, all in manners not open to those who do not possess very large amounts of capital. Then when the laws are written as they require, they employ cadres of lawyers to fight their cases in courts where the judges are schmoozed, if not bought, and where the law they payed to game is brought to bear. They also have a great deal of confidence that the laws used against poor and marginalised people will not be used against them, the rich people, and if by some extraordinary clumsiness on their own part, they do end up in court, they can lawyer-up and escape a negative judgement or pay their way out of trouble (most usually) whilst still retaining large parts of their fortunes. “Confidence in Obedience”, “Confidence in Liquidity”, “Confidence in Impunity”? These are all the inscriptions of the faces of the many-sided die which they cast and which are numbered or labelled on almost all faces with good outcomes for them. One can play confidently with ostensibly unloaded die if the rules of the game grant you wins or at least impunity and significant residual wealth with every throw.

The word “traditional” is actually important. When we consider the key insight of CasP theory, that “in the real world the quantum of capital exists as finance, and only as finance,” does it make sense to refer back to theories of political science designed to describe and understand something entirely different? If we are going to understand capital as power, shouldn’t we consider discarding traditional concepts like “the ruled” and “the state” and build a new lexicon from finance on up? If instead of starting with “the state” of capital, we start with the Market (i.e., the market for capital assets, which like capital exists wholly within Finance), might we see things a bit differently and perhaps more clearly? The ruled are excluded from the Market , i.e., they are not participants of the Market or citizens of the state of capital, they’re just another commodity to be marketed and consumed. From the Market’s point of view, the ruled haven’t been marginalized any more than timber, fish, wheat or cows have been marginalized, and to think otherwise is a category-error.

To the extent the Market controls the market through what we traditionally call the state, we must consider the state’s role relative to the Market, i.e., a state that enforces the market’s rule of the ruled is an appendage of the Market, not vice versa. At the end of the day, capitalism relies primarily on the systemic, institutional violence of the market to render the ruled as helpless as any other commodity. The market requires you to have money to live, so you must work for a wage. Because I gave you a job, you owe me a portion of the value you created, etc. Because the bank “loaned” me money to start my business, I owe it some of the profits I make from my business. It’s this chain of debts that creates and maintains the hierarchies of capitalism, which ensures that Finance is always the senior and secured party.

September 11, 2022 at 9:25 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248328Thank you Scot. Your claim, then, is that if, as a group, capitalists think that asset prices should be lower, they will likely go down — and if they think asset prices should be higher, they will likely rise. I believe we agree on this mechanism. The interesting question is why. Why do capitalists. as a group, think that asset prices should be higher or lower — or, in your language, why should liquidity go up or down?

Unfortunately, that is not my claim. It would be nice if it were so simple, but for me the meaning of “liquidity” depends on the context of its use. Let me fumble around some and try to explain my thinking more clearly.

Liquidity is not the process for setting capital asset prices, it is the predicate for an orderly and functioning Market, by which I mean specifically the market for capital assets. In the absence of liquidity, there are no transactions, and the price of all assets is effectively zero. In this context, liquidity means “potential buyers with money and a desire spend it on capital assets.” If nobody is willing to exchange their money for your capital, how much power do you have? If there are willing buyers but you must sell your capital assets for pennies on the dollar to cover your debts, how much power did you ever have?

In my view, the answer has to do with what capitalists, as a group, think about future earnings, risk and the normal rate of return; and what they think about these three elementary particles hinges on power — that is, on the obedience of the system and people that they collectively rule (including policymakers, mind you). Finally, if we agree that asset prices are set by the capitalists themselves, it follows that their capitalized power gauges their own confidence in this obedience.

The Market is not the same as “the market” (aka the market for goods and services). In the market, capitalists set the prices for goods and services, and consumers pay those prices. In the Market, capital assets are not “priced” in this sense at all. There is a bid, and there is an ask. The difference between the bid and the ask is the spread, and a transaction only occurs if somebody is willing to cross the spread. The “Market price” for a security simply refers to the share price paid in the most recent public sale and is not binding on other buyers and sellers, i.e., prices in the Market are not fixed, they are aspirational. The more confidence capitalists have in liquidity, the more capital asset prices approach the aspirational ideal of discounted future earnings, and vice versa.

Liquidity crises often arise when a capitalist is forced to liquidate its Market holdings to cover debts. If there is not enough liquidity to purchase the holdings at or near current “Market pricing,” this can cause major downward and cascading dislocations in capital asset prices, causing the Market to crash. Such panics arise because capitalists don’t look to the ruled for their cues on when to liquidate their capital assets, they look at each other because threats to their capital (power) almost always come from other capitalists, not from the ruled.

Since its inception, the Market has been beset by fraud and sharp practices designed to give false signals of liquidity and urge prices upwards. We see this every day now with high frequency trading and so-called dark pools, both of which are designed to prevent price-discovery. We also see it with “market making” service providers who, for a fee from a publicly traded company, will buy shares of that company to make sure it does not fall below a certain price. Capitalists have as much concern about the obedience of the ruled as the shepherd has fear of his sheep. To dominant capital, the ruled are sheep, the market pens them in for shearing, and the state rounds up the sheep that try to escape.

This is why I think your Power Index measures confidence in liquidity, not confidence in the obedience of the ruled, and why I believe capital is power only so long as there is sufficient liquidity to ensure a properly functioning Market. Of course, if the Market fails, the state (which the ruled consider separate and distinct from the Market) will step in and impose austerity to ensure the Market’s return to liquidity. Until recently, the sole purpose and role of the Federal Reserve was to ensure Market participants of liquidity, which it is now starting to unwind through quantitative tightening.

September 9, 2022 at 10:40 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248322It seems to me that how capital assets are priced–i.e., looking backward or looking forward– reflects relative confidence in the proper functioning of the Market and, more specifically, the continued existence of liquidity.

Scot, what do you mean by ‘liquidity’, exactly?

That’s a good question. To a great extent, I am trying to use the term as Colin Drumm does in his thesis “The Difference That Money Makes.” Is there a market in money for capital assets, i.e., are there enough potential buyers willing to trade money for capital assets at their current market prices? If not, those prices goes down, generally, and if there is a liquidity crisis (i.e., a broad preference to hold “money” over holding capital assets), the price trends towards zero. If everybody prefers to hold money instead of capital assets, what is the value of those capital assets?

So, I’d guess the best way to define “liquidity” is the availability of a counter-party willing to trade money for a capital asset at or near its current market price. If the spread between bid and ask for a stock becomes too large, the market for that stock fails, and the share price of the stock collapses.

Liquidity requires a sufficient number of buyers willing to support the prices demanded by the sellers (i.e., the market price). I hope that’s not too circular, but hysteresis (positive feedback) is part of market pricing for capital assets.

September 6, 2022 at 7:31 pm in reply to: Jujutsu: can we lever the power of capital against itself? #248315I am waiting for the discussion to develop more before responding substantively (if I ever do). In the meantime, Robert Meister’s recent book Justice Is an Option: A Democratic Theory of Finance for the Twenty-First Century is a very interesting book that explores using finance against itself. The first few chapters are excellent in reframing all financial transactions as options.

From the publisher’s description:

More than ten years after the worst crisis since the Great Depression, the financial sector is thriving. But something is deeply wrong. Taxpayers bore the burden of bailing out “too big to fail” banks, but got nothing in return. Inequality has soared, and a populist backlash against elites has shaken the foundations of our political order. Meanwhile, financial capitalism seems more entrenched than ever. What is the left to do?

Justice Is an Option uses those problems—and the framework of finance that created them—to reimagine historical justice. Robert Meister returns to the spirit of Marx to diagnose our current age of finance. Instead of closing our eyes to the political and economic realities of our era, we need to grapple with them head-on. Meister does just that, asking whether the very tools of finance that have created our vastly unequal world could instead be made to serve justice and equality. Meister here formulates nothing less than a democratic financial theory for the twenty-first century—one that is equally conversant in political philosophy, Marxism, and contemporary politics. Justice Is an Option is a radical, invigorating first page of a new—and sorely needed—leftist playbook.

Here is a link to a YouTube video of a panel discussion from this June where Meister and the panelists discuss Meister’s book and theory.

Andrew,

You may find this forum thread helpful.

The most common use of the term “capitalization” in CasP is shorthand for “market capitalization” and refers to the market cap of a company’s stock, which is the price of a single share of the stock multiplied by the total number of outstanding shares. According to CasP theory, a company’s market cap, i.e., capitalization, is a quantification of its relative power to create or change order within society. Market cap is one of the “key statistics” maintained for every publicly traded company by financial websites like Yahoo Finance.

CasP uses the terms “discounting” and “discount rate” in exactly the same way they are used in finance and accounting. A company’s market capitalization does not represent the present value of its present assets, it represents the present value of its future earnings (profits). To determine the present value of future earnings — which are really only estimates based on certain assumptions– you discount them according to a formula using a discount rate. This basic process is known as “net present valuation” or “NPV,” which is readily available as a function in spreadsheet programs. If you want a deep dive on NPV and how it relates to discounting, see this link. NOTE: the book simplifies the presentation of discounting and discount rate and does not use the NPV formula, but sometimes it is better to sacrifice detail for clarity.

FYI – as much as the book talks about economics, CasP theory is grounded in finance. So, not having an economics background is to your advantage.

So, “biblicalization” of power language correlates not with transitions of the accumulation regime but with the power grip of capital onto society. The greater the power grip the “higher” the justification needs to be, economic justification is no longer enough. Awaiting a proper charting, it seems that at least in the phase after 1980 the change in language trails the rising power grip. If ideology came first it should be the other way round. This would conform Marx’s observation that the “material” process, here rising corporate power, comes first, and only afterwards a “suitable” consciousness develops.

The end of the 19th century in America was known as the “Gilded Age,” which culminated with the passage of antitrust laws in the 1890s. So, one could argue that the peak of biblical jargon circa 1900 resulted in the reduction of the power grip of capital on society; i.e., religion was the basis for combatting the capitalist power, not securing it. Remember, the U.S. was much more religious then than it is today.

It is not clear to me that the current trajectory of biblical jargon will necessarily have the same result as the 1900 peak because the current trajectory coincides with the radicalization of America’s Christian right, whose prosperity gospel is centered on capitalism. They seek to change the capitalist order to make extractive capitalists (e.g., oil, gas, mining and agriculture) ascend above the financial capitalists who currently lead dominant capital. That is, the current trajectory of biblical jargon may indicate a civil war within dominant capital, not society generally seeking to curtail capitalist power.

July 18, 2022 at 9:51 pm in reply to: Comment on “The Aggregate Demand Problem in Capitalism Solved” #248132I’d argue that credit, not wages, is central to all crises.

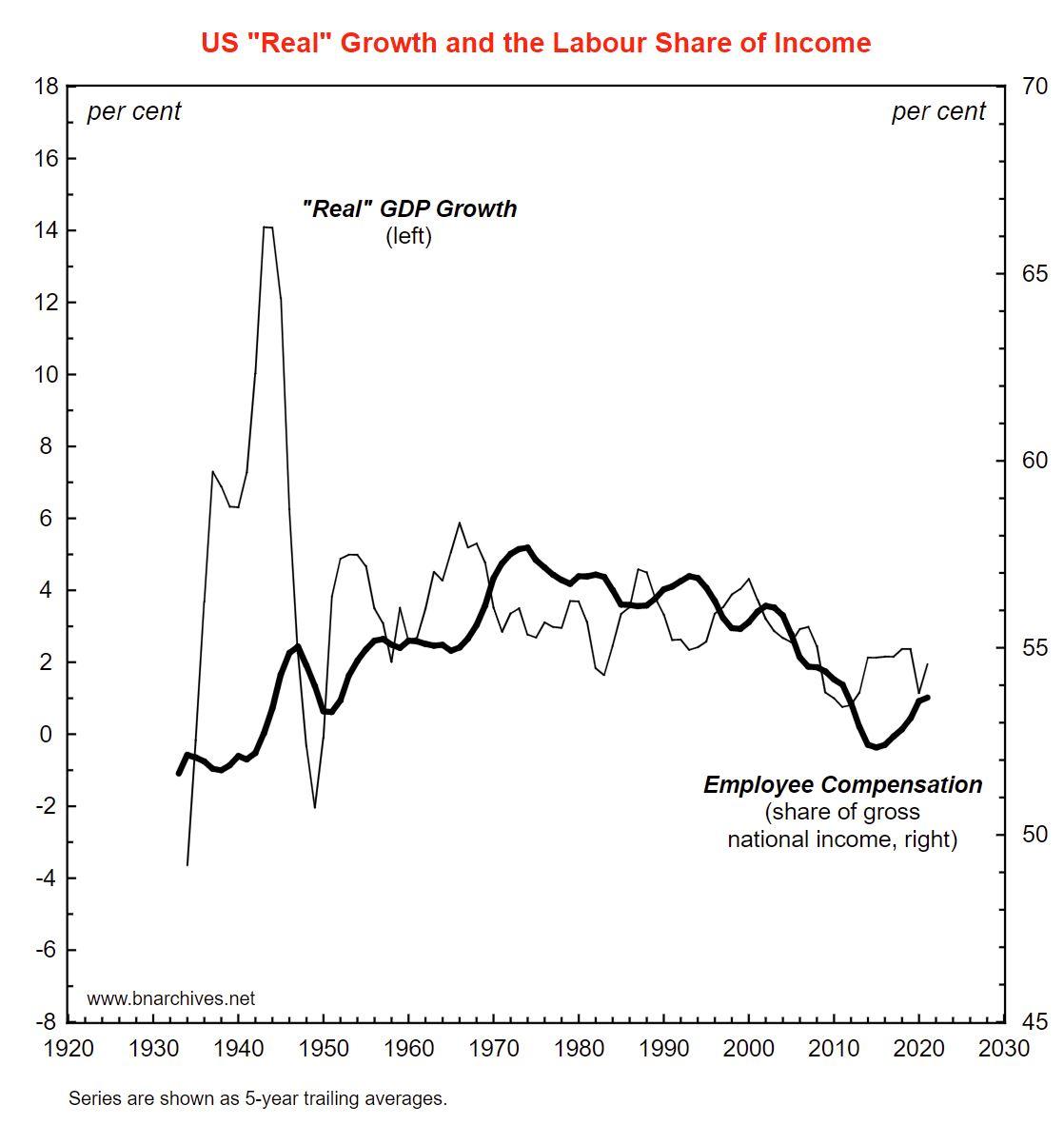

1. Note that my rough-and-ready description rehashes the convention perspective of economics, not my own view. It is meant to explain why Marxists and post-Keynesian see the general movement of wages as central for aggregate demand, even though it is only a segment of that demand. 2. And yes, credit and capitalization more generally are the key organizing principle of capitalism. But the expansion of credit depends on distributional dynamics. If the wage share trends downward, credit expansion can surely fill the gap — but only to a point. The likelihood of banks lending more and more to increasingly wage-strapped workers and firms with bloated excess capacity is fairly small. 3. The figure below shows U.S. ‘real’ GDP growth along with the overall wage share in gross national income. The chart demonstrates that the wage share rose till the early 1970s and fell thereafter, and that ‘real’ growth followed a similar periodicity. The short-term differences between the series may have been affected by credit, but the long-term trends were not.

Thanks, Jonathan. The additional explanation was helpful.

July 18, 2022 at 2:32 pm in reply to: Comment on “The Aggregate Demand Problem in Capitalism Solved” #248129“Aggregate demand comprises more than the consumption of workers alone. It also includes the consumption of capitalists, their investment in new capacity, the spending of government, and the purchases of foreign buyers.”

Credit is another major component of aggregate demand and typically the source of investment (as understood with respect to GDP, which does not consider speculation in equity markets to be investment) and government spending.

“So, in the final analysis, wages, although making only part of aggregate demand, are central to all crises.”

I’d argue that credit, not wages, is central to all crises. For example, according to Steve Keen, if the rate of change of debt contracts, the unemployment rate rises, and aggregate wages go down. Also, the loosening of credit and its extension to workers (e.g., through credit cards) are what allowed the suppression of wage growth reflected in Di Muzio’s graph. Bob Meister has a good discussion of what led to this dynamic in chapter 2 of Justice is an Option at pages 55-58. Finally, in addition to contributing to aggregate demand, credit creation is the source of the liquidity needed to service existing debts, and principal payments are not reflected in the GDP metric (only interest payments are).

Without credit, there is no money. Without money, there are no wages.

-

AuthorReplies