Forum Replies Created

-

AuthorReplies

-

With respect, I feel CasP is failing of its own radical promise and insights if it does not arrive at the full conclusion that the untrue “representations” – they are actually prescriptions not representations – of money, finance, capital with respect to reality and as calculations for the manipulation of reality ought to be wholly and radically abolished […] The complete abolition of capital and capitalism is an existential necessity, [etc.]

1. Yes, I agree. Capitalism should be radically transformed and, if possible, replaced by a different, saner from of social organization. But you don’t need CasP to draw this conclusion. Marxists, anarchists and many social democrats hold similar views.

2. CasP’s main contribution is to show that capital is power, and that capitalism is a mode of power. But I don’t think these claims per se are enough to assess the pros and cons of capitalized power. Such assessment requires that we figure out, both theoretically and empirically, exactly how, to what extent and with what consequences capital is power and capitalism a mode of power. In my view, this research remains very much in its infancy.

3. These uncertainties do not mean we should not try to change or abolish capitalism. The very imposition of capitalized power and its assorted forms of sabotage is good enough reason to jettison it, even if it doesn’t terminate humanity. But I think we should be careful not to deduce our preferences from ‘CasP findings’. Regrettably, these findings, however promising, require more breadth and depth to replace the existing ideologies and critiques of capitalism.

4. I’m voicing these reservations not to diminish CasP, but to defend it. I think CasP is a very effective template for analyzing — and ultimately changing — capitalism. It helps avoid the difficulties and impossibilities of Marxist materialism and neoclassical utilitarianism while offering insights into crucial processes they serve to hide. But these advantages hinge on keeping CasP a vibrant, open science. Once CasP starts accumulating preset ‘positions’, ‘assertions’, ‘leaders’ and ‘followers’, its science and novelty will fizzle out and dogma will take over.

- This reply was modified 2 years, 11 months ago by Jonathan Nitzan.

- This reply was modified 2 years, 11 months ago by Jonathan Nitzan.

- This reply was modified 2 years, 11 months ago by Jonathan Nitzan.

This all asks the question. To survive, must we fully envision the abolition of income-producing private property and of money, markets, capital and finance? If not, what is envisaged and/or advocated from a Capital as Power perspective?

As I see it, the capital as power approach argues that (1) capital is best understood as the quantification of organized power; and (2) this understanding alters the way we theorize, historicize, research and relate to capitalism in practice.

I think that the practical implications of this understanding — namely, whether to defend, reform or abolish capitalism — are open ended. These implications are influenced by the notion that capital is power, but that notion alone does not chart the path forward. For example, CasP anarchists might prefer a system that minimizes organized power; disillusioned neoliberals might argue that the best defense against the quest for power is invigorating capitalist competition; while CasP fascists might go for centralized state and racial power instead.

A side note. The chief capitalist quantities are those used for the creordering of power. But I think that quantities will remain necessary in any complex society, even egalitarian ones. It is difficult if not impossible to juggle the balls of complexity without them.

Thank you Brian. I don’t know if the wranglings you describe represent a new cold war, but I can offer some relevant CasP pointers.

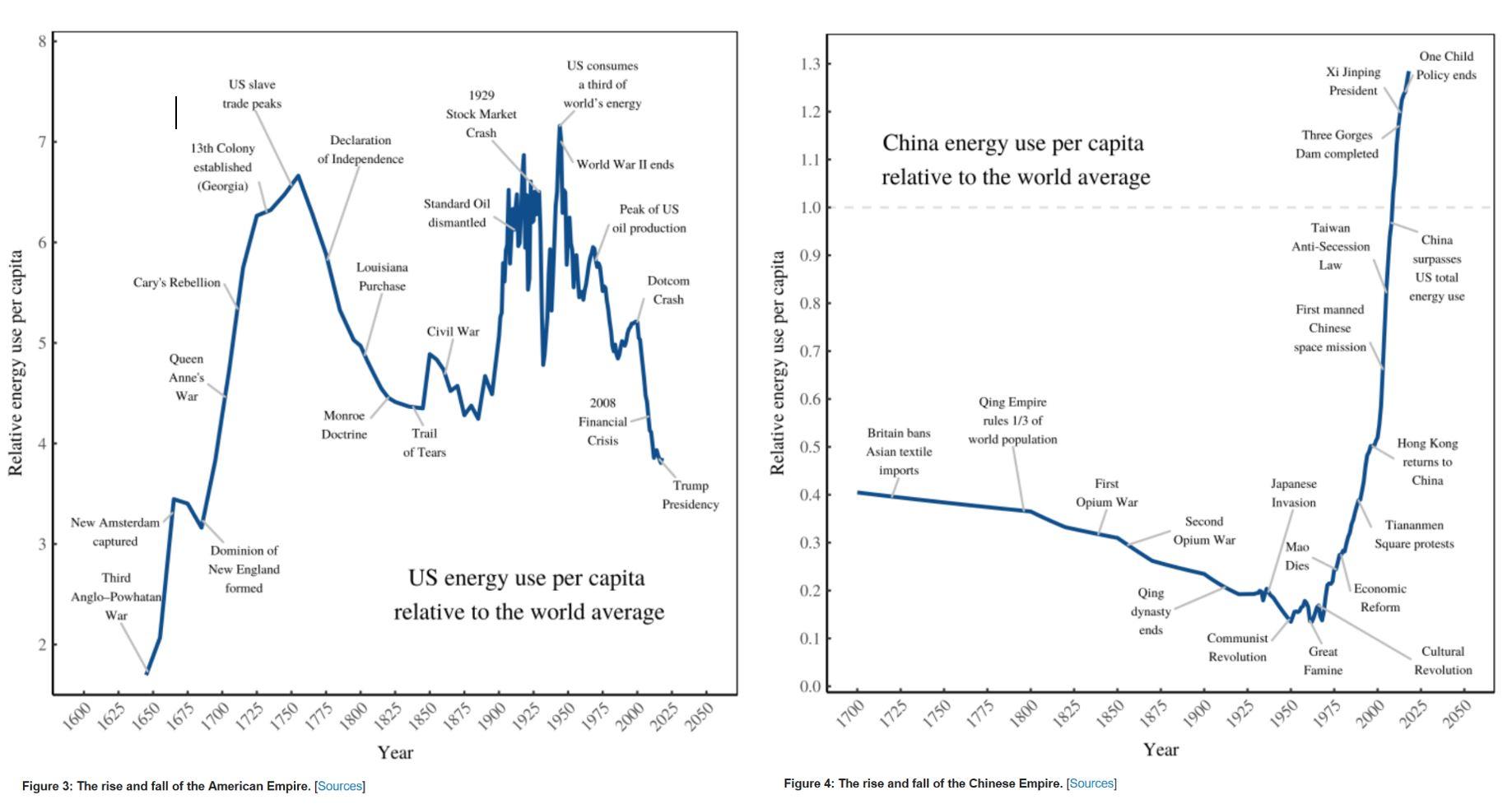

Begin with Blair Fix’s 2020 paper ‘Why America Won’t Be Great Again’, in which he compares the differential energy use per capital of the ‘West’ relative to the ‘East’ and of the U.K., the U.S. and China relative to the world. Here are the U.S. and China charts from his paper.

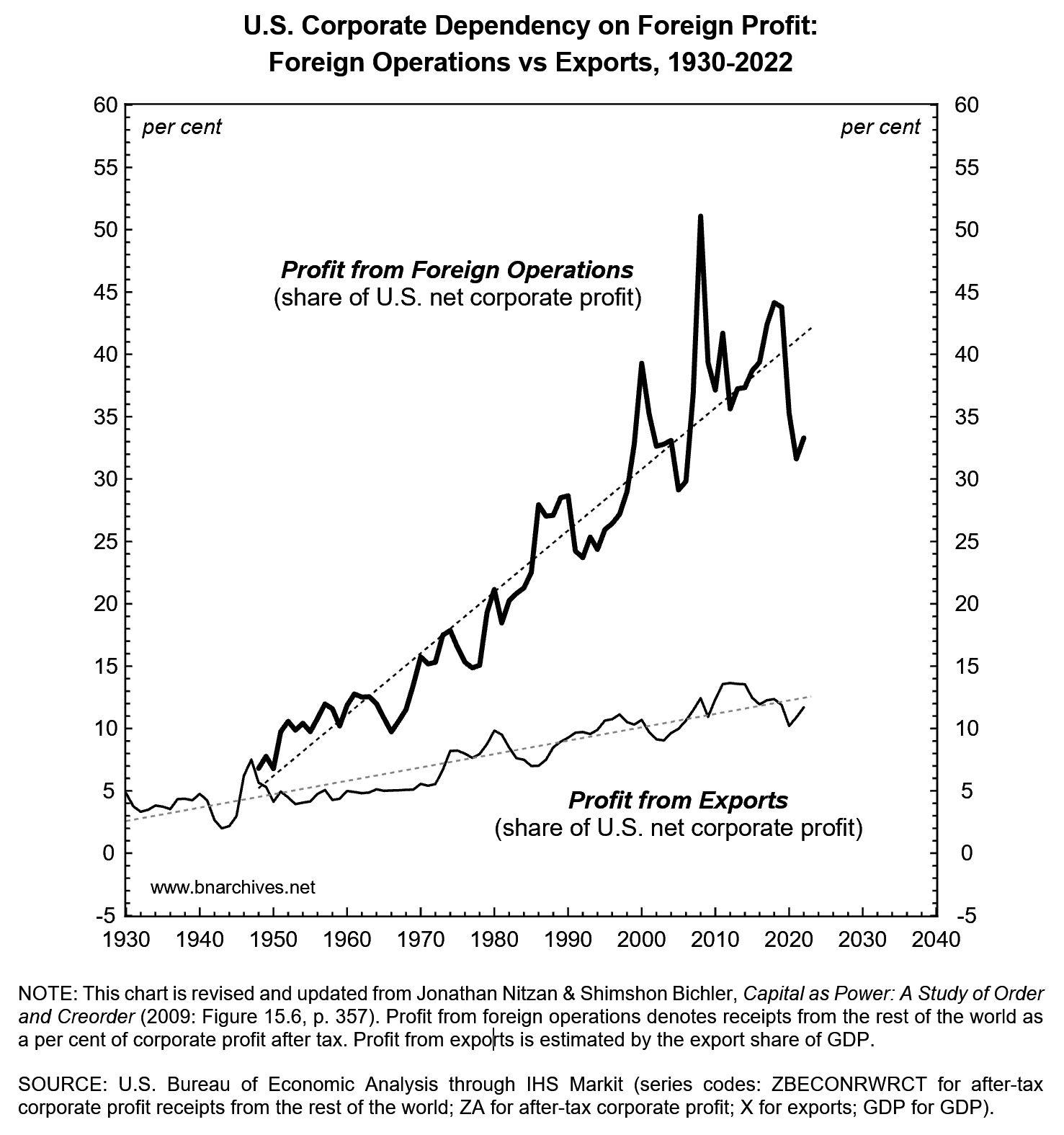

Next is our own 2019 Real-World Economics Review paper, ‘Making America Great Again’, in which we assessed Donald Trump’s aspirations to stop the rise of China. One of the figures in that paper showed the growing long-term reliance of U.S. corporations on profit from foreign sources. This chart is updated here till 2022.

https://bnarchives.yorku.ca/630/

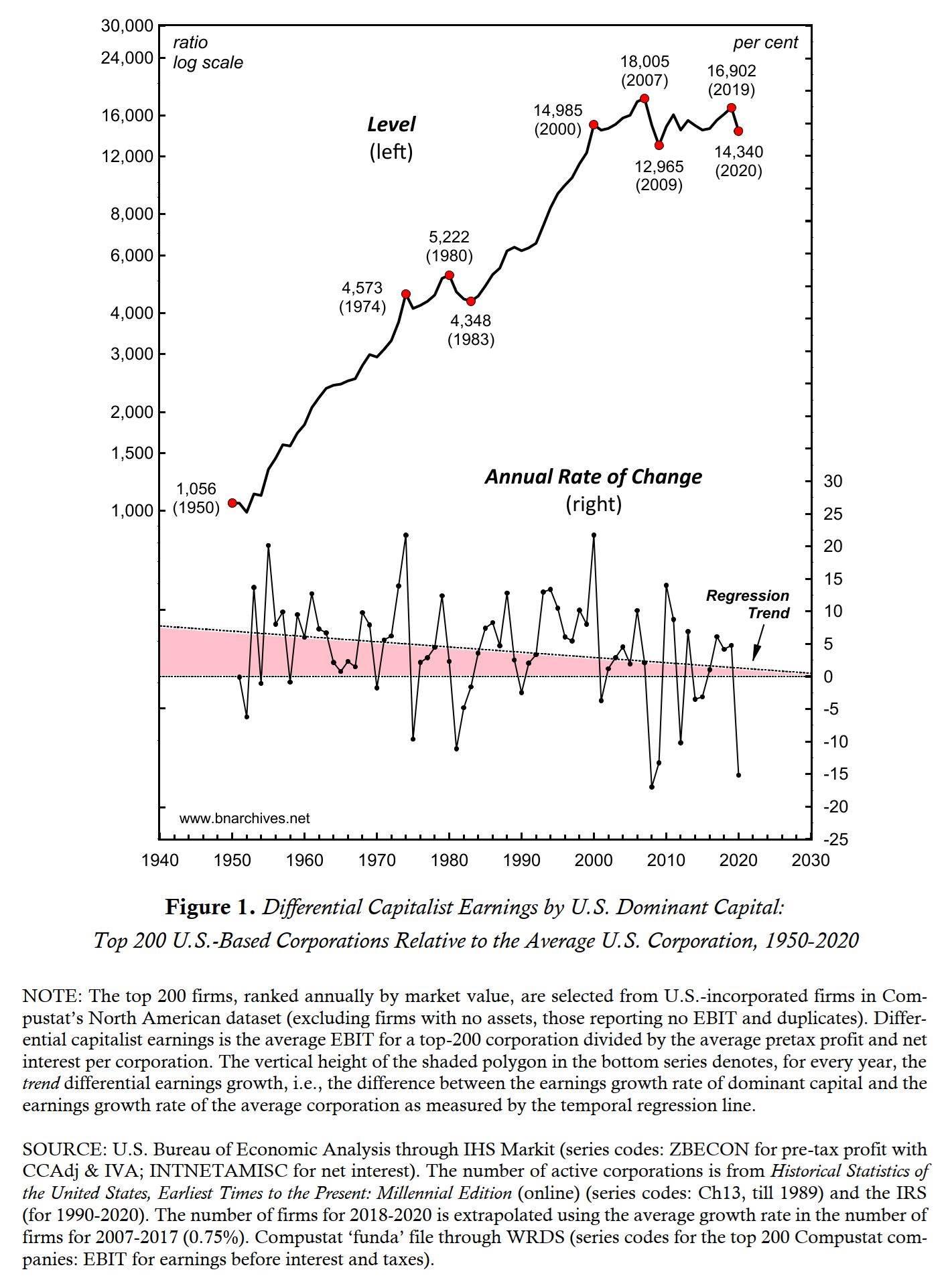

A third relevant paper is our 2021 Real-World Economics Review Blog post, ‘Dominant Capital and the Government’, which assesses the relative power of these two entities in the U.S. (though note that they are deeply intertwined). This chart shows the changing level and rate of change of differential earnings (EBIT) of the 200 biggest U.S.-incoporated firms.

https://bnarchives.yorku.ca/716/

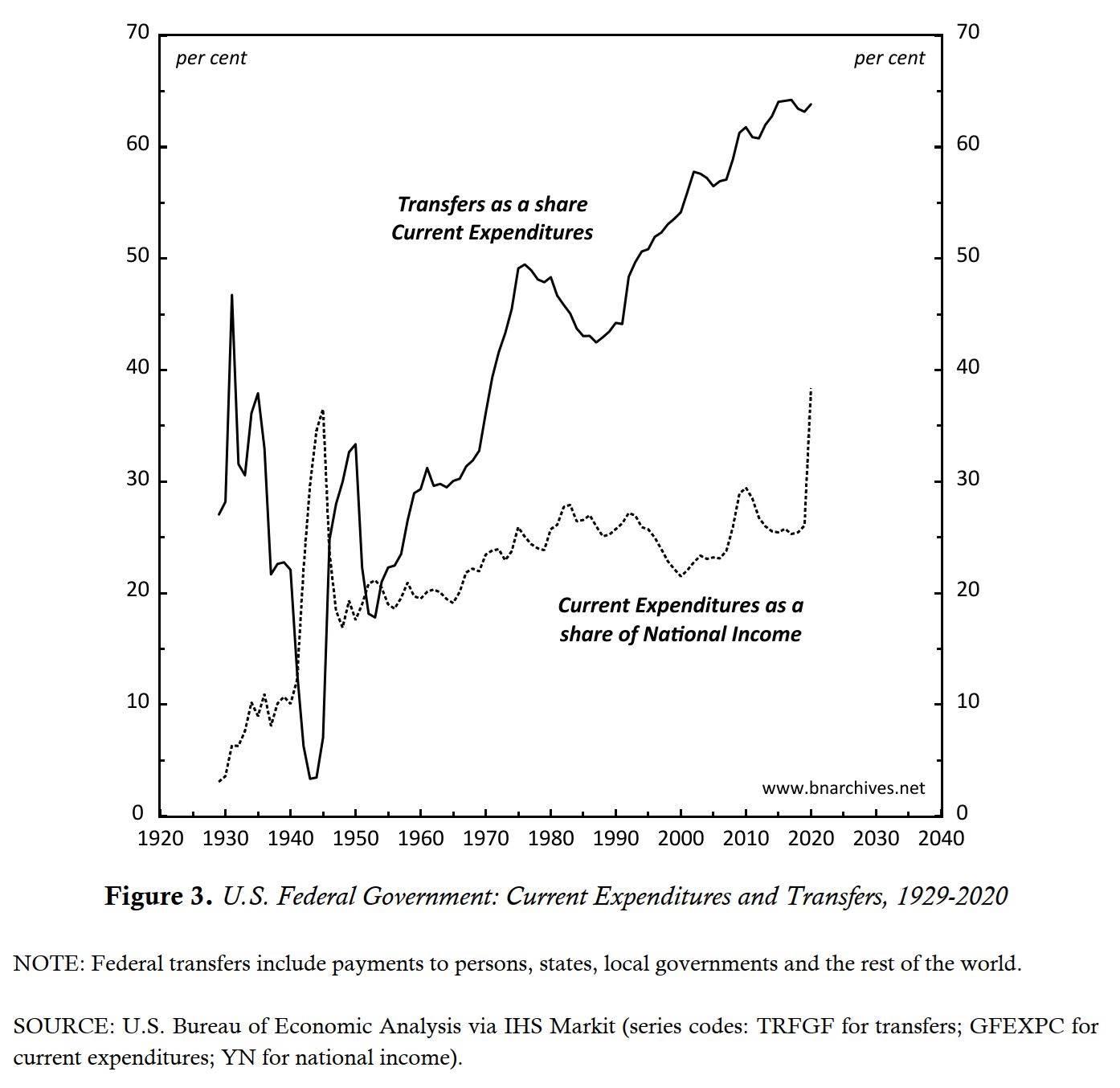

The following figure, from the same paper, shows the U.S. GDP share of Federal government expenditures and the rising proportion of those expenditures earmarked as transfers. U.S. policymakers these days have very little spending discretion.

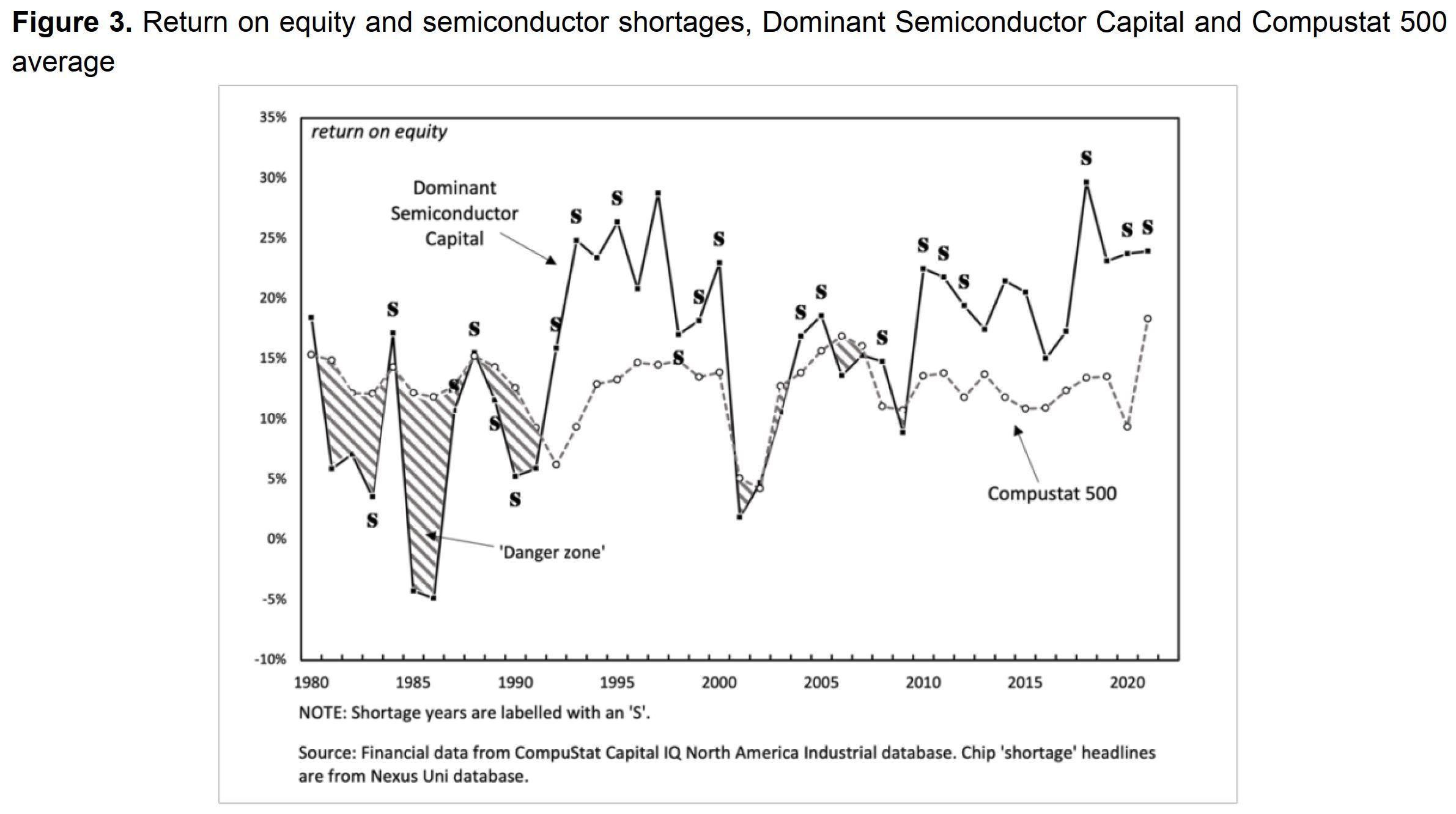

The final paper in this short list is Christopher Mouré’s ‘Technological Change and Strategic Sabotage: A Capital as Power Analysis of the US Semiconductor Business’, published in 2023 by Real-World Economics Review. The article goes into the intricacies of strategic sabotage and how manipulated ‘shortages’ affect the differential profits of dominant capital in this sector. This chart exhibits one of those links.

https://bnarchives.yorku.ca/777/

- This reply was modified 3 years ago by Jonathan Nitzan.

Interesting chart, Adam.

The negative correlation between falling differential capitalization of fracking firms and rising of anti-fracking sentiment raises the question of what exactly the public sentiment affects: differential earning, differential hype, or differential risk?

One way of answering this question, however tentatively, is to examine differential PE (fracking PE relative to S&P500 PE). This ratio removes the effect on differential capitalization of differential profit, leaving us with the ratio of differential hype to differential risk.

Granted, this is only a makeshift decomposition, since capitalization usually reflects future rather than preset profit; but still, it might be an interesting thing to examine.

- This reply was modified 3 years, 1 month ago by Jonathan Nitzan.

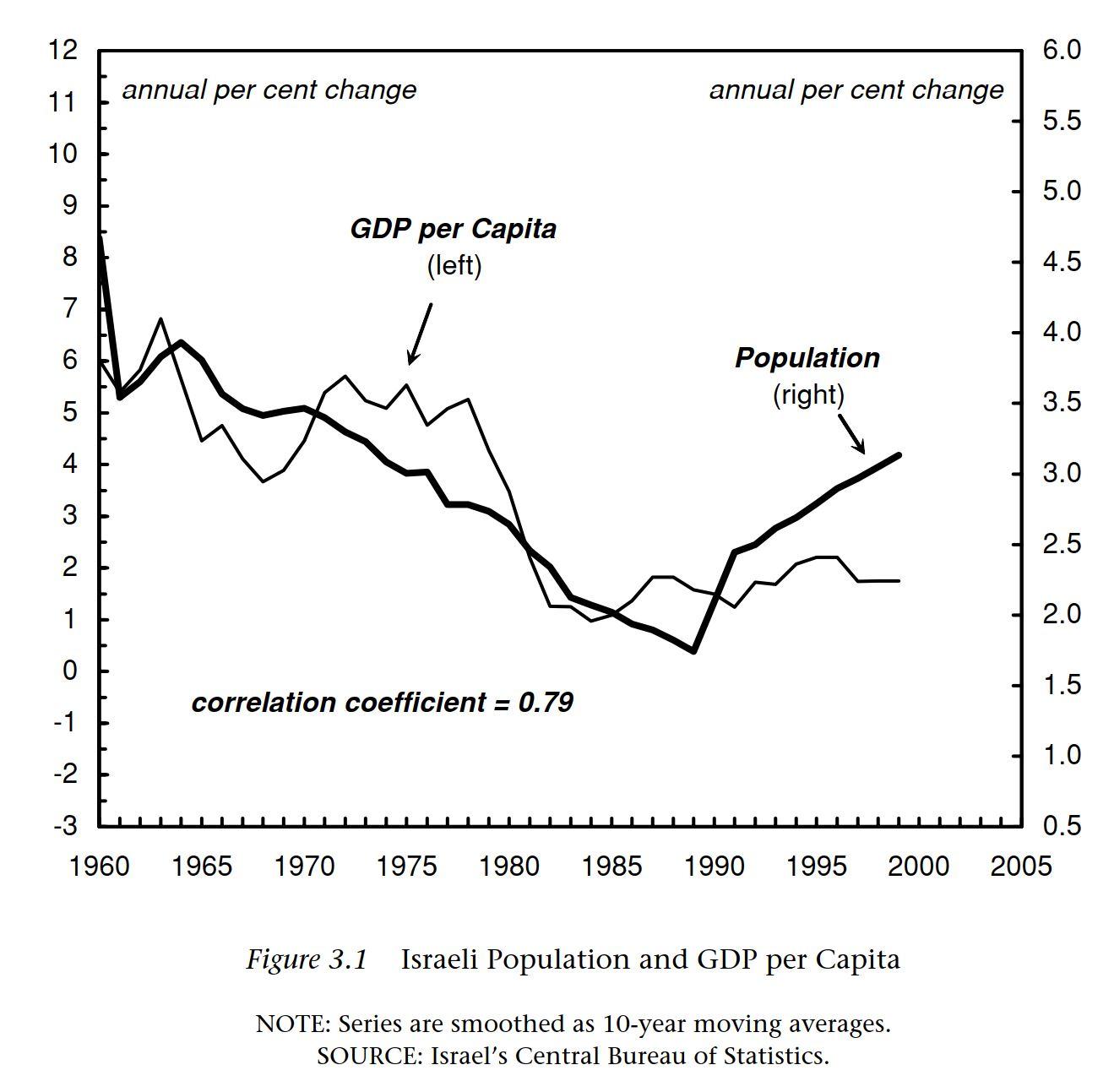

This chart from our 2002 Global Political Economy of Israel shows the tight correlation between the Israeli growth rates of population and per capita ‘real’ GDP.

Is this positive correlation the international norm? And if it is the norm, will global demographic deceleration amplify economic stagnation?

So far, the capitalist mode of power has been associated with a growing population, which raises the question of what will happen to this mode of power if the size of humanity stagnates or even falls.

I don’t know the answer to this question, but I do know (1) that prior modes of power existed with stable or only gradually rising population, and (2) that capitalism has been rather agile in responding and adapting to changing circumstances.

Humanity’s cumulative impact on the biosphere makes population de-growth likely, if not inevitable: this de-growth will come either through deliberate or semi-deliberate human action, or courtesy of a socio-ecological calamity.

Regarding the consequent prospects for capitalism, the obvious question to consider are: (1) what are the effects on capitalist power relations of population growth/decline; and (2) what capitalist organizations can do to alter these relations when populations start to stagnate or contract.

A new CasP research project in the making?

- This reply was modified 3 years, 4 months ago by Jonathan Nitzan.

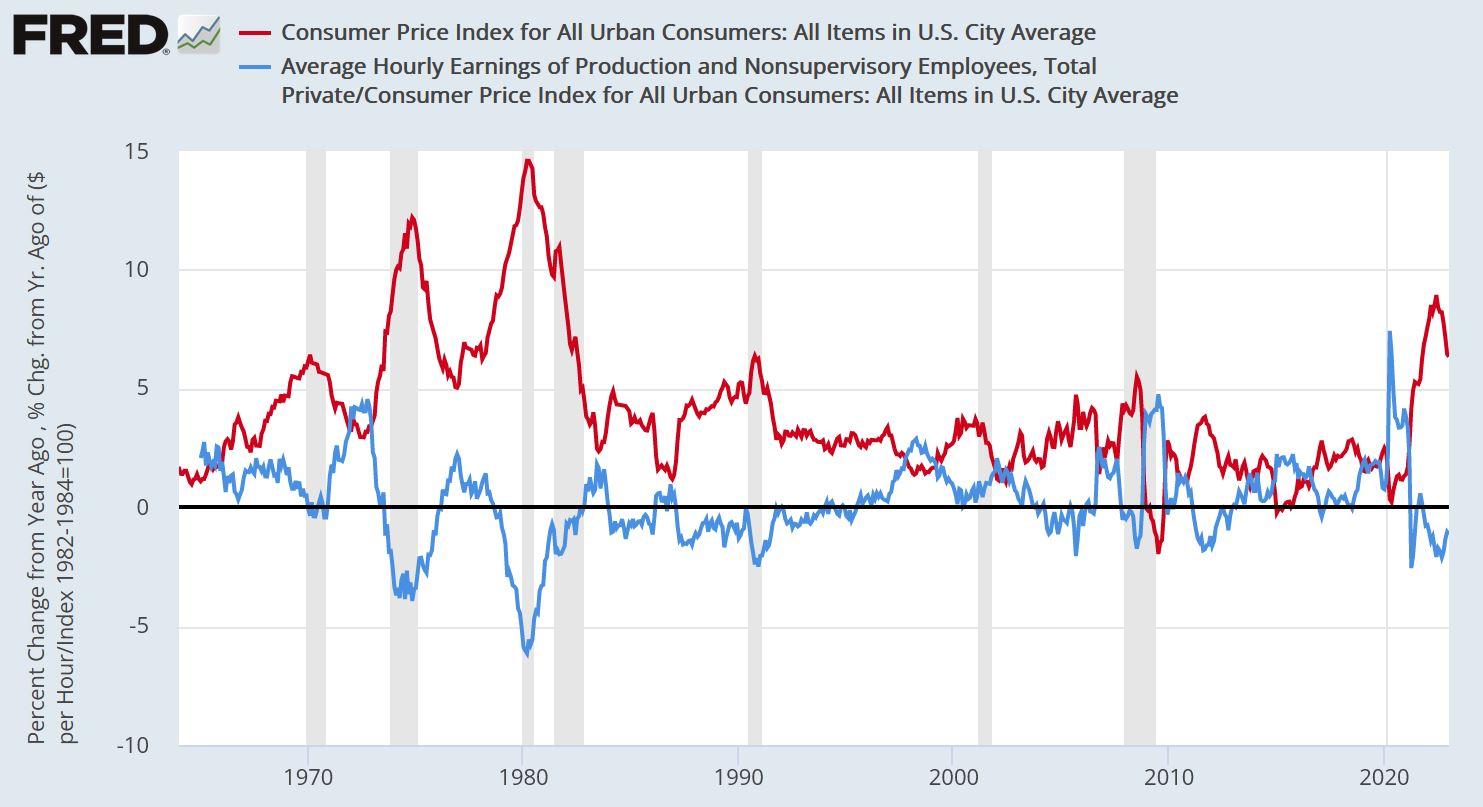

March 4, 2023 at 5:14 am in reply to: Inflation is always and everywhere a redistributional phenomenon #2489223. Redistribution tends to limit the inflationary process — as inflation redistributes income from workers to capitalists, it undermines workers’ income-read-consumption, causing the the profitability of price-setters to gradually wane. Eventually, capitalists lose their price-hike resolve, their tacit coordination fractures, and inflation decelerates.

Here is an update, with data extended till January 2023: as the purchasing power of workers declined, inflation eventually inverted.

January 3, 2023 at 1:54 pm in reply to: What’s the breadth of “Breadth”? What’s the depth of “Depth”? #248806

January 3, 2023 at 1:54 pm in reply to: What’s the breadth of “Breadth”? What’s the depth of “Depth”? #248806Shimshon and I argue that capitalized power is a quantitative relationship between entities. In its broadest sense, it is conceived as a differential, measured by the ratio between the capitalization of the entity in question (A) and the capitalization of other entities (benchmark):

1. capitalized power of A = capitalization of A / capitalization of the benchmark

We further argue that this differential can be applied to the elementary particles of capitalization, which we identified as future earnings, hype and risk (the normal rate of return, being common to both numerator and denominator, drops from the differential equation).

Looking at profit only, we get:

2. differential profit of A = profit of A / profit of the benchmark

For any capitalist entity, the following identity (and its differential parallel) always holds:

3. profit = employment * profit per employee = breadth * depth

Mathematically, the choice of this specific decomposition is arbitrary. We can easily generate other decompositions that will be equally valid. For example, profit = sales * (profit/sales), or profit = number of company cars * (profit/cars) are as valid as Equation 3.

The reason we prioritize Equation 3 over other decompositions is theoretical. In our view, social power, including capitalized power, is exercised over people and by people. The exercise and impact of this power are multidimensional, of course, spanning much of what happens in society. But it is often useful to address this exercise/impact at two distinct levels, by looking at (1) direct power over the entity’s employees (breadth), and (2) indirect power, exercised through the activities of those employees on the rest of society (depth).

Two useful points follow.

First, our breadth/depth bifurcation is one of many possible choices. We found it useful in generating and explaining DA regimes and other processes. But that’s us. If you think, for example, that under certain circumstances profit = sales * (profit/sales) is more appropriate, go ahead and use it – but note the implications. For example, unlike employment, sales involve direct as well as indirect power, since they relates not only to the entity’s employees, but also to prices paid and spending made by buyers outside the entity.

Second, the decomposition itself neither reveals nor masks the underlying exercise/implications of power. It simply attributes them in a particular way. For example, the power aspects of advertisement relate mostly to depth in our Equation 3 decomposition, but span both depth and breadth if we use profit = sales * (profit/sales) instead.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

December 24, 2022 at 12:37 pm in reply to: Effective Discount Rate or the Reciprocal of the Trailing P/E #248789Thank you for your replies, Scot.

Questions drive thinking, so I thought it was clear that, in saying that you asked many questions but that it wasn’t always clear why, I didn’t criticize you for asking them. I simply meant that I, personally, didn’t understand the reason behind them.

Let me try to clarify my thinking here.

1.

As I see it, the rate of return at any point in time is a backward-looking straightforward computation of the rate of change of the asset’s price (or total return, as the case may be).

By contrast, the discount rate at which future earnings are capitalized to give an asset its price is a much more slippery forward-looking construct. In my work with Shimshon, we suggested two things: (1) that in the mind of capitalists this rate is the product of a ‘normal rate’ common to all investments and a ‘risk coefficient’ unique to the asset in question; and (2) that both quanta vary over time and across investors and can be known only by asking them (finance manuals don’t count here, since investors are free to ignore them).

With this conceptual difference in mind, the rate of return and the discount rate will be the same only by fluke.

2.

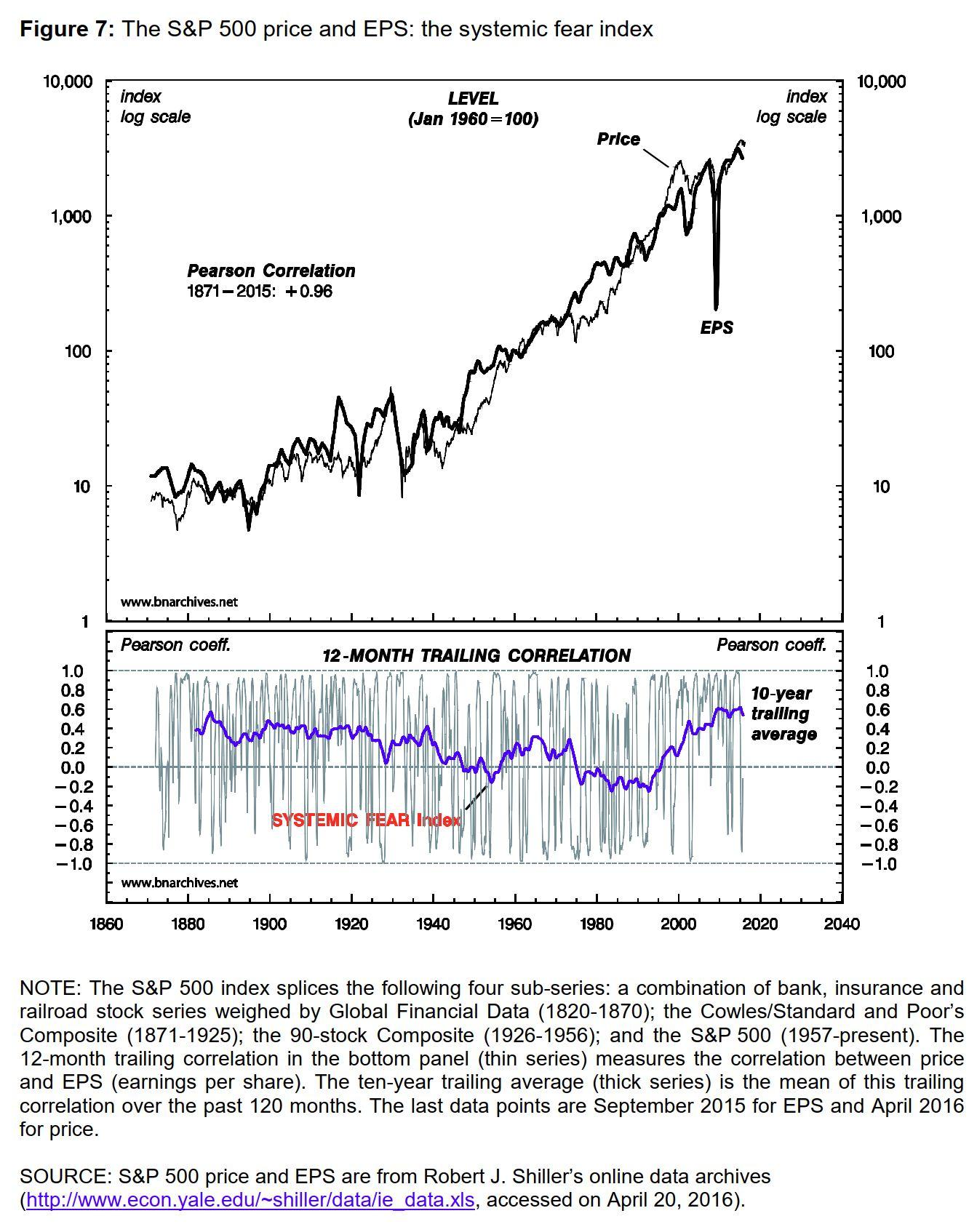

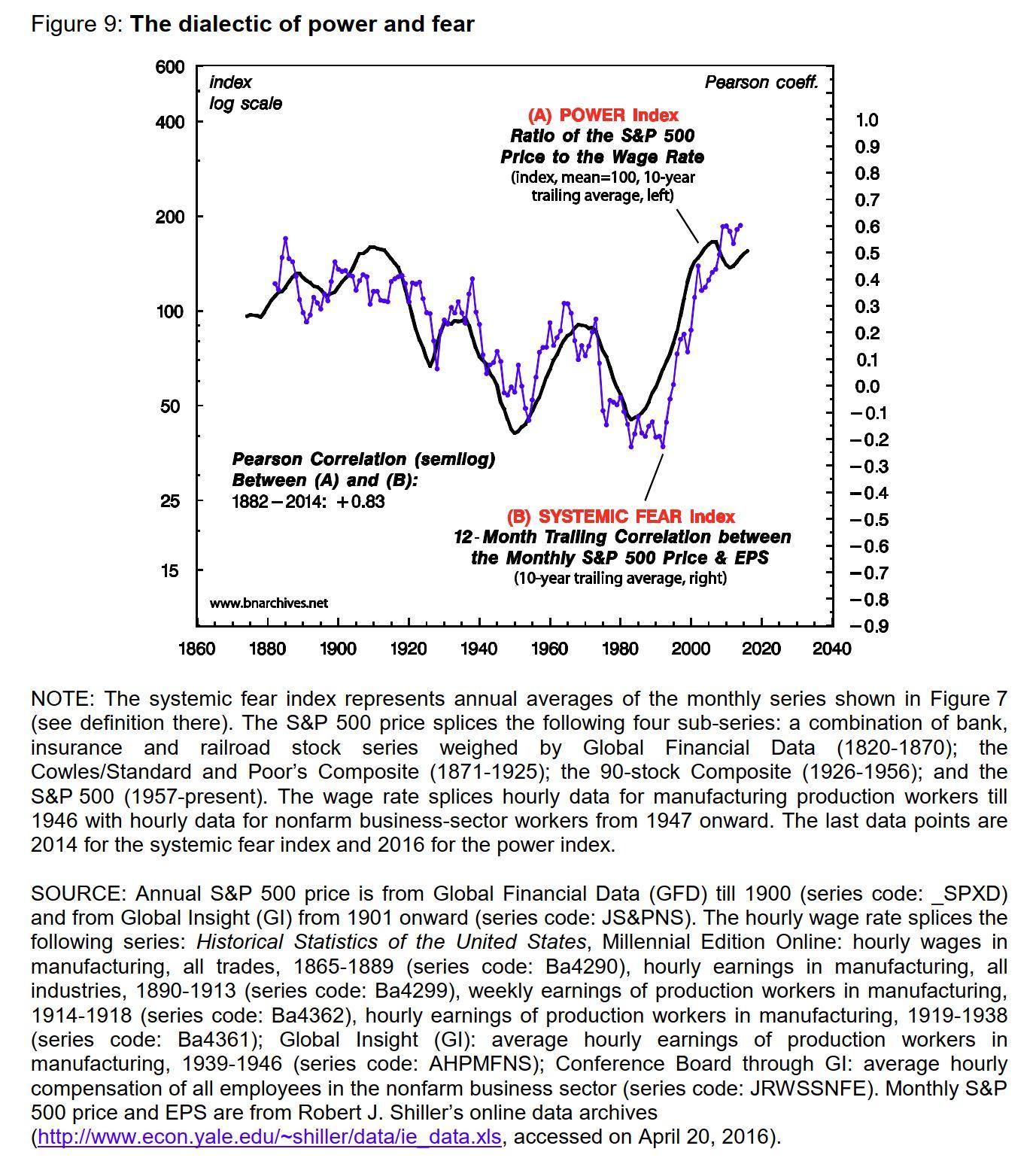

The positive long-term U.S. correlation between stock prices and trailing earnings shown in Figure 7 of our ‘CasP Model of the Stock Market’ is backward-looking and therefore cannot tell us how capitalists set asset prices looking forward.

3.

Contrary to your interpretation, we – Bichler and I – do not argue that the trailing E/P ratio is the effective discount rate. Our claim, rather, is that capitalists change the earnings they discount depending on their power relative to workers and their systemic fear. When capitalists are less powerful and more confident, they follow their dominant ritual and tend to discount expected future earnings; when they are more powerful and less confident, they tend to abandon this ritual and discount trailing earrings. The purpose of the bottom panel of Figure 7 and of Figure 9 in our ‘CasP Model of the Stock Market’ was to substantiate this proposition.

4.

Firms with similar backward-looking data can be priced differently – and yield different rates of return — because forward-looking capitalization pretends to see a future that isn’t necessarily the same as the past.

5.

You seem to suggest that finance is somehow separate from and perhaps more important than economics, and maybe you are right. In our view, though, they are not separate but integrated. I think we agree that to understand capitalism we must understand finance, among other things (in our case, because finance is the main architecture of capitalized power). But in our opinion, finance has no theoretical underpinnings of its own. Complex as it may look in practice, finance is a ritualistic derivative of mainstream economic reasoning (or, as an erudite late friend of mine once bluntly opined, ‘it’s not even a “branch of knowledge”’.)

6.

You argue that saying that ‘capital is power’ is ineffective as saying that ‘water is wet’. Somehow, I doubt you really mean it. Researching and demonstrating the ways in which capital is power helps undermine prevailing political-economy and create a new way of understanding and resisting capitalism. The fact that we personally seldom engage in ‘policy recommendations’ is because, at this point, we don’t feel there is anyone to recommend policies to. But you and others are more than welcome to do so.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

December 22, 2022 at 8:30 pm in reply to: Effective Discount Rate or the Reciprocal of the Trailing P/E #248778Scot,

You ask many questions, but it isn’t always clear why.

Obviously, capitalization/discounting/compounding can be made as complicated as you like, but in my mind, the purpose of analysis is to achieve the very opposite — i.e., to simplify. How much to simplify depends on the concrete subject of analysis, which you are yet to specify.

1. Regarding discounting with current known earnings as opposed to expected future earnings. In our 2009 book Capital as Power and later in our 2016 ‘CasP Model of the Stock Market‘, we showed that, over the very long haul, capitalization is tightly correlated with current earnings. This tight correlation is shown in the top panel of this U.S. figure from our ‘CasP Model’.

However, the bottom panel of the chart demonstrates that, over the short run (one year), the correlation between current earnings and capitalized values varies greatly, ranging between +0.6 and -0.2. In other words, in the shorter run, capitalists are very shifty.

2. What causes these changes in the impact of current earnings on capitalization? Our tentative answer was that these shifts depend on the extent of capitalized power (relative to workers): the more powerful/weaker the capitalists, the greater/smaller the correlation. The validity of this claim is shown by the chart below, which correlates capitalized power with the short-term correlation between current earnings and capitalization (taken from the previous chart).

In our work, we speculated that power is bounded. In our view, this bound means that the greater the power, the more frightened capitalists become about their ability to sustain it, and therefore the greater their reliance on visible earnings here and now when capitalizing the future. This is why we labeled the short-term earnings correlation with capitalization the ‘Systemic Fear Index’. (For more on these issues, see Baines and Hager (2020), McMahon (2021) and the work by Fix (2021) that you cite.)

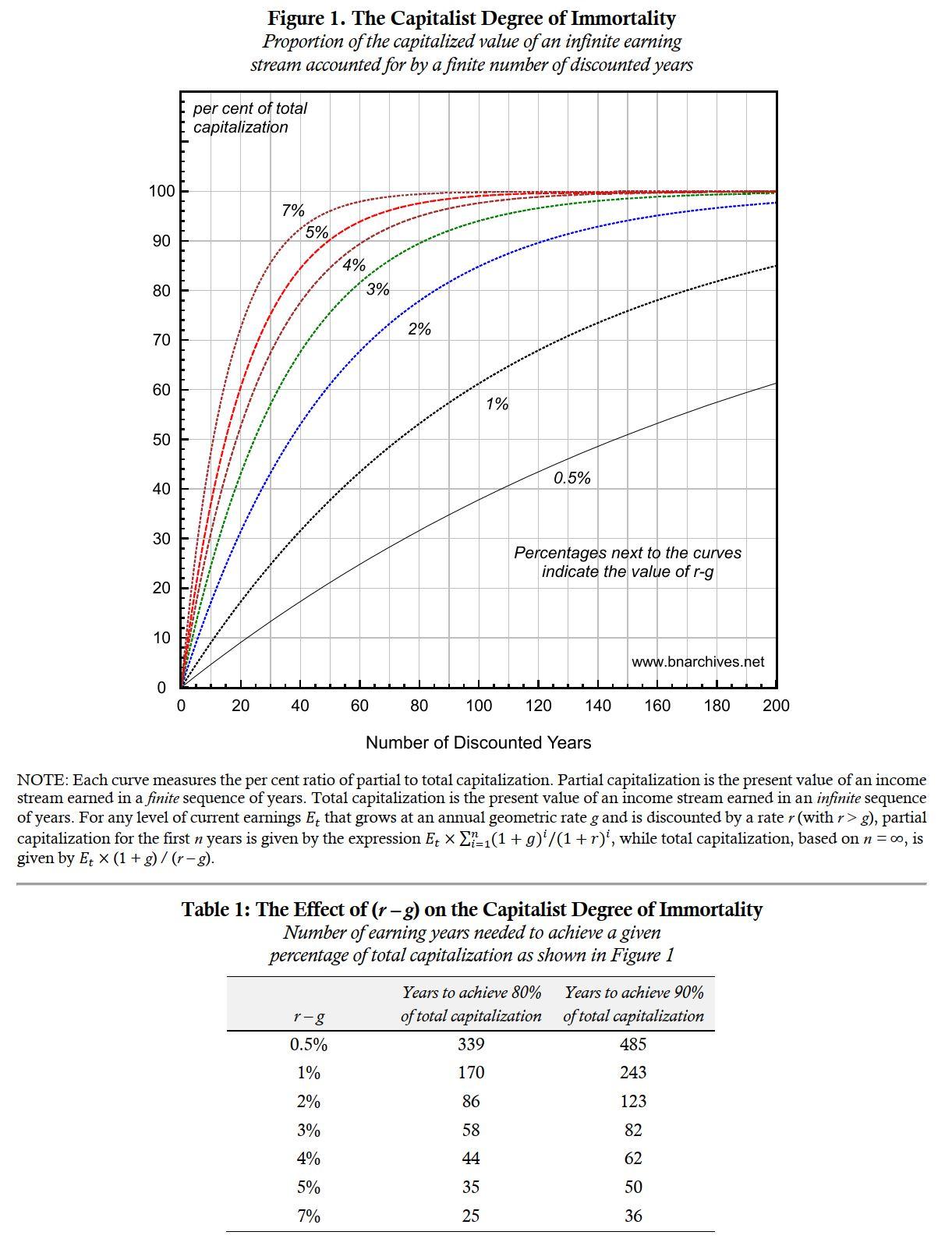

3. On the extent to which capitalists must peer into the future to capture the bulk of their earnings from here to eternity, see our ‘Capitalist Degree of Immortality’ (2021). The chart below shows these computations for various levels of (r–g), where r is the discount rate and g is the geometric long-term growth rate of earnings. It turns out that, under rather normal condition, the capitalist gaze doesn’t have to extend beyond a few dozen years….

Thank you Scot.

Perhaps you mentioned it somewhere in the thread, but it is only now that I realize you define revenues = sold capital + sold output. Since this definition is rarely if ever used either in practice or in accounting pedagogy, I won’t be surprised if others were perplexed by your derivations as I was.

Unrelatedly, there seems to be an error in footnote 20 on page 241 of Capital as Power (2009). To achieve a target return of 20%, you need a markup of 16.67%, not 10% (markup equals r/(1+r)), and 16.67% is what you get when you divide $200M in profit by $1.2B in sales (2/12 = 1/6 = 16.67%) on an initial investment of $1.0B.

Yes, there is a mistake here, but not the one you refer to.

I don’t have the book by Kaplan et al. with me, but if I recall correctly, they define the markup = profit/cost. Our mistake was to use their definition in the footnote without noting it was different than the one we used in the text. In any event, thank you for pointing it out.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

Thank you Scot.

I think we are talking past each other. Accountants distinguish between capital invested and the rate of return on the one hand, and the cost of items sold and the markup on the other, such that:

1. rate of return = profit / capital

so: profit = rate of return * capital

2. markup = profit / cost of items sold

so: profit = markup * cost of item sold.

***

In your notes, you say that:

3. profit = rate of return * cost of items sold

Unless I made a mistake somewhere, for this last equation to be true, cost of items sold = capital, which normally isn’t the case.

December 19, 2022 at 11:38 am in reply to: Proximity to Legal Authority as a Measure of Power #248754Thank you Pieter for the useful clarification.

When they first emerge, ideas and research projects often seem opaque and ‘problematic’, which is only understandable given that they are new.

A thought: perhaps you can think of the relation between capitalized power on the one hand and ‘proximity to legal authority’ (however defined) on the other non-linearly: As proximity decreases capitalized power increases as you describe, but only up to a point. After that point, when we’ve gone past the legislators, pork-barrel interest groups and the big capitalist entities and reached the underling population, lower proximity goes with lower power.

December 16, 2022 at 11:40 am in reply to: Proximity to Legal Authority as a Measure of Power #248741Counterintuitively, the most power is not held by those with direct access to the creation and re-shaping of law, but rather by those with influence over the law-makers.

In our CasP work, we tend to start with capitalized power — a concept whose magnitudes, we argue, are readily observable through differential capitalization, earnings and risk — and then correlate changes in this capitalized power with its alleged determinants, including policies/legislation.

Your notion of ‘proximity to law’ could be useful in this inquiry, because, in capitalism, the law is often a far more effective regulator of power than convention/influence, violence and illegal action.

The problem is that ‘proximity to law’ doesn’t have an easy-to-measure metric, and that is partly because the very notion of ‘distance’ here is ill defined, if not totally open-ended.

For example, in what sense can we say that legislators of intellectual property rights are ‘closer’ to the laws they draft and vote on than the people, entities and processes whose pressures they are subjected to and whose impacts their actions often mirror?

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

Thank you Julien.

1. Our Systemic Fear Index measures the short-term correlation between stock prices and current EPS. We argue that this measure indicates the extent to which asset pricing deviates from the key ritual of capitalizing expected future profits, and that this deviation indicates systemic fear because it shows the extent to which investors doubt their own central compass (A CasP Model of the Stock Market, 2016).

2. The VIX index is a short-term approximation of expected stock-price volatility (30 days to 1 year, depending on the measure).

Although both measures are related to fear, the nature of their respective fear seems different. The first measure is long term, focusing on very limits of capitalization, the second short term, focusing on stock price volatility in the near future.

Perhaps there is reason for them to correlate, though that reason doesn’t seem obvious on the surface.

-

AuthorReplies