Forum Replies Created

-

AuthorReplies

-

February 19, 2021 at 5:58 pm in reply to: Questions Regarding Mumford’s Theory of the Mega-Machine #245381

Blair, I saw your post only after posting mine, so just a small comment.

What Sober and Wilson describe is hardly ironic. It is a well-known pattern throughout history. You yourself use the term ‘competition’, but is there really competition in nature, or are we simply imposing our own concept on it? Could Darwin’s ‘natural selection’ appear before the ‘competitive’ world from which Malthus’ theory of population emerged?

February 19, 2021 at 5:35 pm in reply to: Questions Regarding Mumford’s Theory of the Mega-Machine #245378Thank you for the detailed answer, David. This is all very interesting and inseminating. I remember thirty odd years ago reading and being fascinated by Peter Russell’s work on the ‘global brain’, and I suspect that with easy computing and instant communication this line of argumentation has since exploded.

But it seems to me that the issues I have raised earlier still linger. Your descriptions of the living body and of the planetary body continue to rely heavily on the way in which we describe our society. In your 650-word post above you have used the terms ‘competition’, ‘conflict’, ‘greed’, ‘violence’, ‘reward’, ‘homicide’, ‘suicide’, ‘survival’ and ‘cannibalism’, and I think many more social terms would have crept up were we to continue.

My point: we are imposing our own social world on the natural universe around us. And we aren’t the first to do so. Human societies have always conceived the cosmos in this way. But if the natural world is a human-made mirror of our own, using it as a model is a complicating detour (hat tip to Paul Samuelson). Why not simply look at ourselves?

Regarding apoptosis, a neat video by my daughter, Elvire: https://www.youtube.com/watch?v=-vmtK-bAC5

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

February 19, 2021 at 12:03 pm in reply to: Questions Regarding Mumford’s Theory of the Mega-Machine #245372David,

1. There is no need to swear allegiance to CasP. We are doing open science, with critique as its bloodline (in honour of biology!). And your notes are all thought provoking.

2. Alternative formulations are welcome (if they weren’t, there would be no CasP theory…)

3. My main beef with biological body metaphors is that they are not very good in describing internal power struggles, let alone inherent and conscious ones.

Correct me if I’m wrong, but biologists tend to think of bodies as resonating systems whose purpose is ‘survival’ and whose ‘diseases’ are either externally inflicted or the consequence of malfunction. Human societies are different. On some level, they appear resonating. People go to work every day, they think more or less alike, they fight external enemies, they police against internal crime, etc. But much of this apparent resonance is the consequence of an ongoing struggle, often conscious, between a ruling class that seeks and generally succeeds in imposing its own order and the ruled who resist this order.

Can this ongoing internal conflict be effectively described with body metaphors? Is the brain in ‘conflict’ with other organs? Do the heart and kidneys ever try to ‘take over’ the brain in order to rule the body in its stead? Are some cells knowingly ‘fighting’ or ‘forced into submission by’ other cells?

4. And speaking about metaphors:

I believe the emergence of hierarchically organized power societies is better modeled by the emergence of early nervous systems in nature: when cells first specialized to be able to respond to changes in their local and distant environments via depolarization of the cell membrane (action potential), and began organizing into functional hierarchies and major functional systems to facilitate ever greater economies of information transfer, retention, and organization.

Notice how your biology relies on social metaphors. The terms ‘hierarchies’, ‘economies’ and ‘information’ are all borrowed from our understanding of society…

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

February 17, 2021 at 3:26 pm in reply to: Questions Regarding Mumford’s Theory of the Mega-Machine #245367Thank you David for another very interesting note.

I must admit I’m no longer sure about the point of contention. I think we all agree that humans are animate rather than inanimate, and that the laws of physics are insufficient to explain their actions and reactions. I think we further agree that there is no complete determinism in human affairs insofar as humans seem to have at least some ‘free will’ — or at least that is how it appears to us. Consequently, models of human and social interaction are open-ended.

But the models are not completely open-ended — first, because humans are conditioned by the laws of physics and chemistry as well as by their biology; and, second, because human psyche, beliefs and actions are at least partly shaped by their society. I think we probably agree on these claims as well.

With these tentative agreements in mind, the idea of a megamachine cannot be more than a loose metaphor. A society of humans cannot function like a clockwork or a Boston Dynamics army of robots. Even within the confines of physics, chemistry, biology and ideology there is plenty of room for novelty, and human beings have even started to change some of these very confines!

But when we consider society, power and resistance to power seem everyone. In this context, we might think of social power as the ability to creorder the evolution of society, and of resistance to power as attempts to oppose and prevent it. And one way of creordering society is to try and mechanize it — i.e., make it responsive, predictably, to one’s commands. This is the basic idea of the megamachine. A megamachine is always partial and never omnipotent for the reasons noted above, but its inherent incompleteness doesn’t prevent the ruling class from trying to impose it nonetheless.

Now, whether ‘mechanization’ in general and the ‘megamachine’ in particular are the most useful descriptions of this process is an open question. Looking at the world around us, I think they are. The mechanical, ‘rational’ worldview is still dominant, and it is accepted by modern rulers everywhere, perhaps more than ever. But I also agree that there could be other, equally useful or even better metaphors. And if you can think of such metaphors and show their robustness, please share your thoughts and findings!

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

February 16, 2021 at 4:37 pm in reply to: Questions Regarding Mumford’s Theory of the Mega-Machine #245360Complex societies are problem-solving organizations

The ‘problem solving’ engine takes a positive view: complexity is created because humans try to solve problems created by earlier complexity, attempts that in turn lead to more complexity, hence more problem solving, therefore more complexity, etc.

The negative view, which we much prefer, is described by Ulf Martin’s autocatalytic sprawl: social complexity is created when rulers impose their power, leading to resistance, which in turn leads to more imposition of power, more resistance, further imposition of power, etc. (see ‘Growing Through Sabotage’).

Both processes result in growing complexity, but for opposite reasons.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

February 15, 2021 at 8:36 pm in reply to: Questions Regarding Mumford’s Theory of the Mega-Machine #245344Thank you for the interesting note, David.

I think you present the metaphor of the megamachine too literally and perhaps too rigidly.

Shimshon and I understand the megamachine not as a one-to-one description of actual society, but as the way that the ruling class tries to structure society. The difference between the two views is important because the rulers are never totally successful in their impositions. And they are not totally successful because the very impositions of the megamachine create conflict and elicit resistance and struggle. This is the dialectical basis for Ulf Martin’s notion of the ‘autocatalytic sprawl’:

‘The Autocatalytic Sprawl of Pseudorational Mastery’

Now, although the ruling class is never totally successful in its impositions, it is certainly successful to some extent. In this context, I think that your point that we cannot observe social cogs harming and killing other social cogs is not well-founded. Capitalism, for example, conditions people to see themselves as stand-alone ‘individuals’ and encourages them, quite effectively, to undercut and sabotage each other, presumably for their own ‘survival’. Capitalism also enables and often drives its subjects to kill other subjects — mostly indirectly, but also directly through organized crime and armed conflict.

Similarly, the fact that the rulers are locked into and conditioned by the logic of the megamachine — for example, the ritual of differential capitalization — doesn’t prevent them from taking plenty of initiative within that logic. And in a complex setting, these multiple initiatives generate multiple conflicts and lead to unpredictable developments. Also, the fact that the impositions of the megamachine are inherently incomplete is another important source of novelty.

can you think of any examples where this would be the case (i.e. where using log scale might be counterproductive)?

The answer depends on what you wish to show.

For example, suppose you have an exponentially growing series and you wish to show its variations regardless of magnitude, a log scale will be the right choice.

But if you are interested not in the variation, but in the actual level of the series — for example, when you plot the growth rate of GDP — a log scale will give you a skewed picture: it will stretch the low growth rates and squeeze the high ones. In this case, a linear scale will be better.

Adam,

The advantage of a vertical log scale are: (1) the slope of the time series is proportionate to the series’ temporal rate of change, so you can see how fast the series changes regardless of its absolute magnitude; this is not the case with a linear presentation; (2) it is equally easy to see small and large changes, which is a nice feature when the series grows or decays exponentially; this is not the case with a linear plot.

When these features are unnecessary or counterproductive, then a linear scale is better.

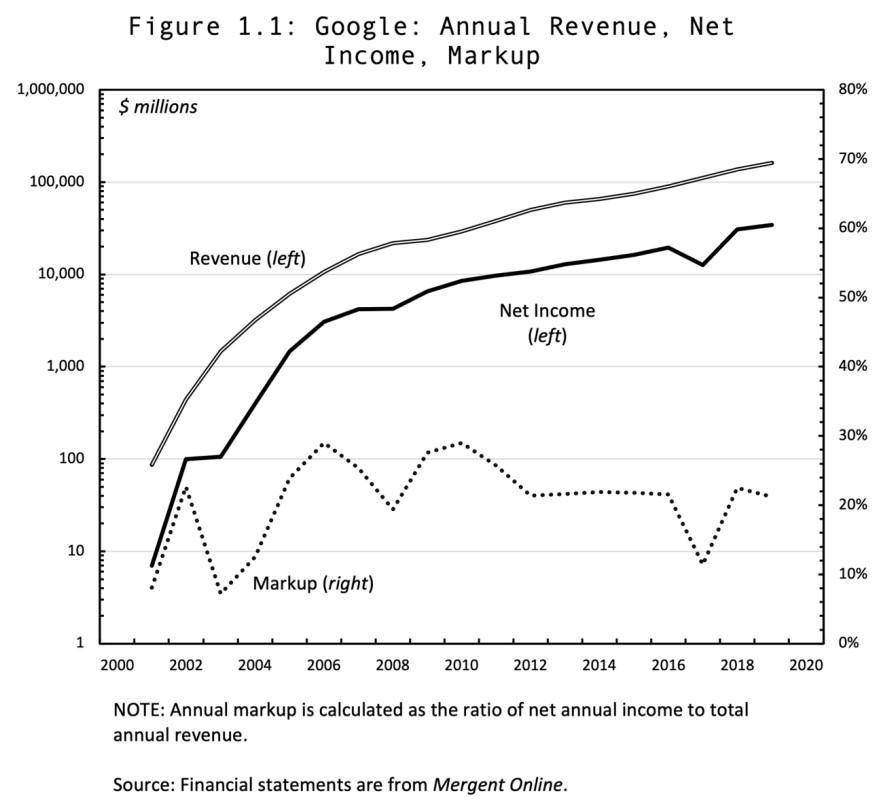

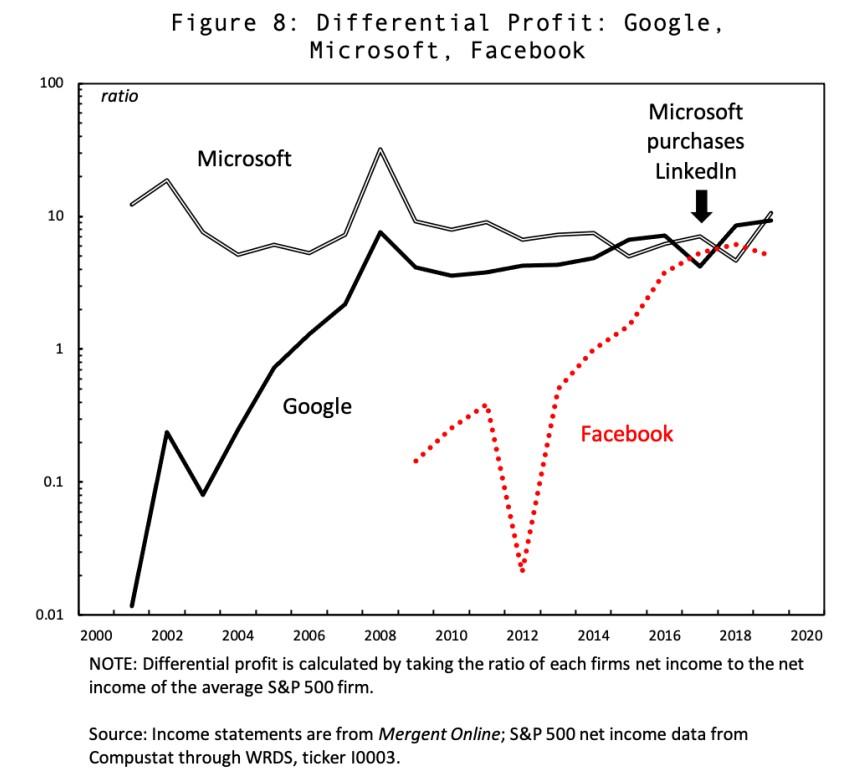

The following two charts, taken from Chris Moure’s 2021 Working Paper on Capital as Power, ‘Soft-wars‘, shows the usefulness of both log and linear scales.

The first figure shows the exponential growth of sales and profit on a log scale and the markup (ratio of profit to sale) on a linear scale.

The second chart compares the differential profit of three large firms that differ markedly in their levels and rates of change. A linear scale won’t be able to visually demonstrate these differences.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

Adam,

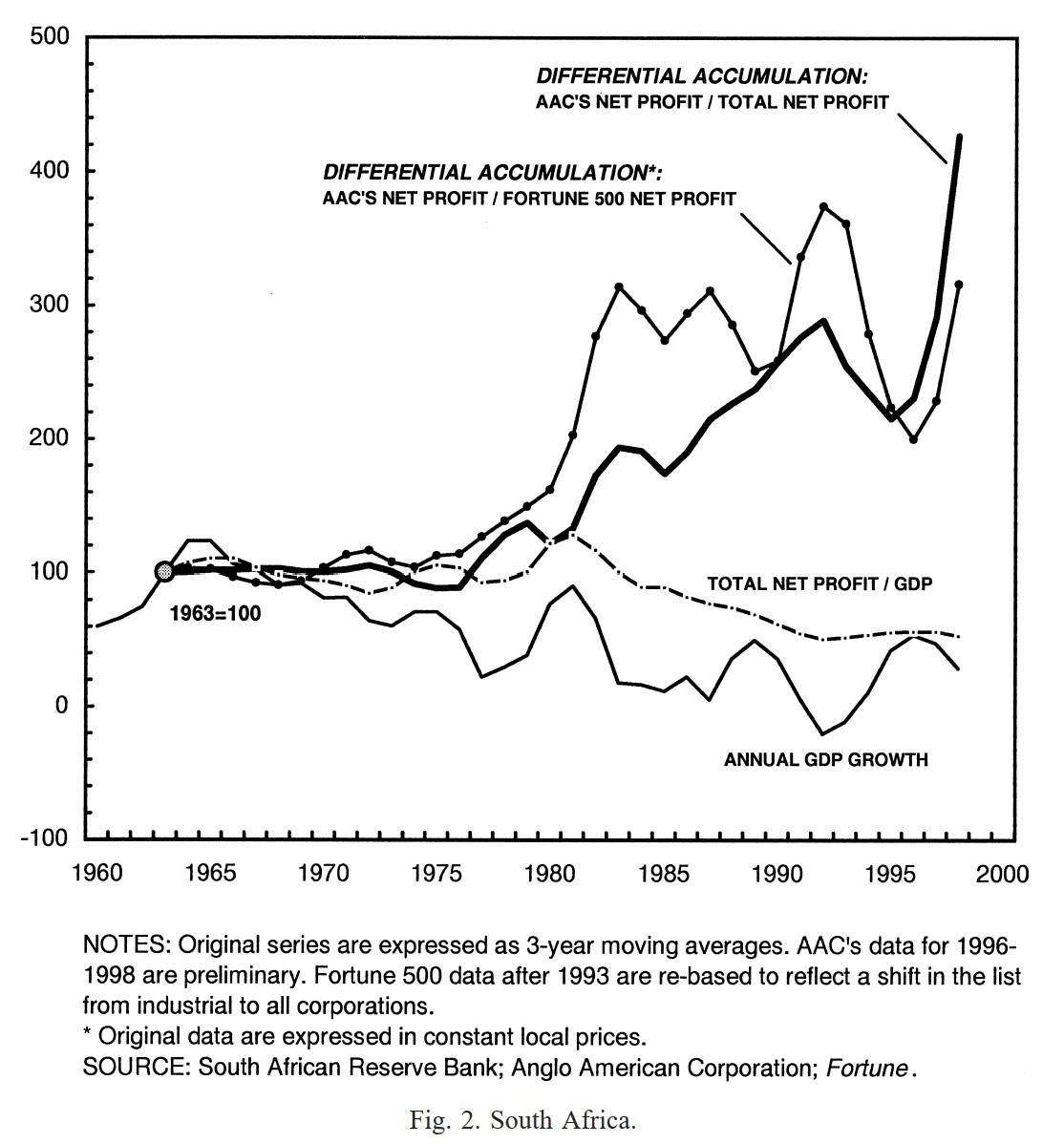

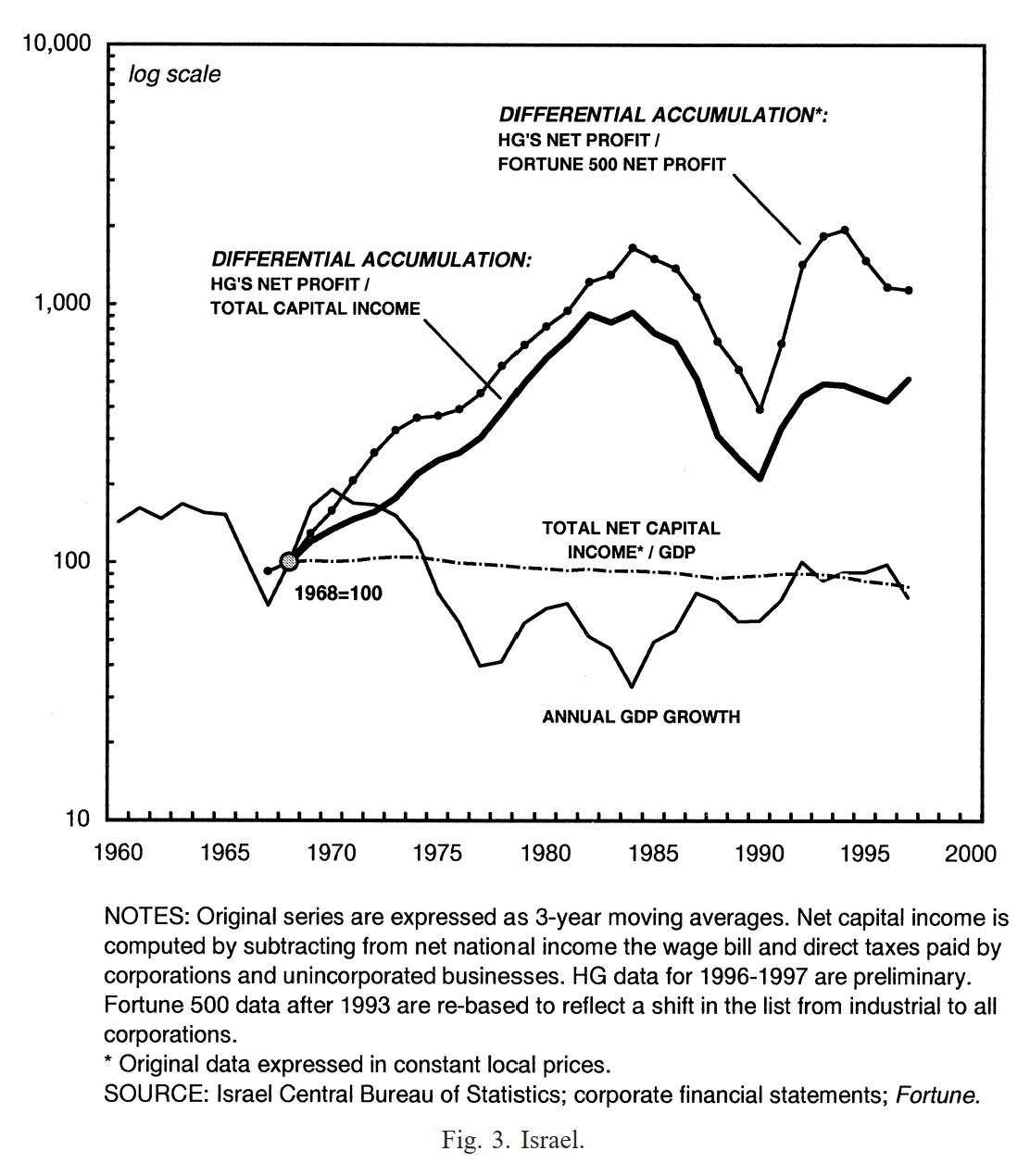

In South Africa, growth was negative in the 1990s, and you cannot compute the log of non-positive numbers. Also, the numbers in South Africa were not growing exponentially as in Israel.

Adam,

Regarding which indices to use, I think Blair’s advice is sound. Usually, more evidence makes your case more robust — although too much evidence can also clutter it.

Below are a couple of graphs from a 2001 comparative article we wrote on the dominant capital groups in South Africa and Israel and the extent to which their differential accumulation impacted the end of Apartheid and the agreement with the Palestinians. In this article, we tried to look at both global and local measures, and we often did so in the same graph.

Going Global: Differential Accumulation and the Great U-turn in South Africa and Israel

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

Some memorable war novels, many of them autobiographical, are listed below. They are all worth reading.

1. Babchenko, Arkadiæi. 2008. One Soldier’s War in Chechnya. Translated from the Russian by Nick Allen. London: Portobello.

2. Ballard, J. G. 1984. Empire of the Sun. A Novel. New York: Simon and Schuster.

3. Browning, Christopher R. 1998. Ordinary Men. Reserve Police Battalion 101 and the Final Solution in Poland. Reissued with a New Afterward by the Author. 1st HarperPerennial ed. New York: HarperPerennial. [Not a novel, but a masterpiece nonetheless.]

4. Céline, Louis-Ferdinand. 1932. [1983]. Journey to the End of the Night. Translated by R. Manheim. np: New Directions. [The first part of the book on WWI is unmatched.]

5. Cendrars, Blaise. 1918. [1984]. The Severed Hand. New York: Stein & Day Pub.

6. Clavell, James. 1962. King Rat. 1st ed. Boston: Little Brown.

7. Coonts, Stephen. 1986. Flight of the Intruder. Annapolis, Md.: Naval Institute Press.

8. Deighton, Len. 1982. Goodbye, Mickey Mouse. 1st ed. New York: Knopf: Distributed by Random House.

9. Duffy, Peter. 2003. The Bielski Brothers. The True Story of Three Men Who Defied the Nazis, Saved 1,200 Jews, and Built a Village in the Forest. 1st ed. New York: HarperCollins.

10. Fisher, David. 1983. The War Magician. New York: Coward-McCann.

11. Gary, Romain. 1960. A European Education. New York: Simon and Schuster.

12. Graves, Robert. 1929. Good-bye to All That. An Autobiography. London: Cape.

13. Hameiri, Avigdor. 1952. The Great Madness. New York: Vantage Press 1952.

14. Hasek, Jaroslav. 1937. The Good Soldier: Schweik. Translated by P. Selver. Garden City New York: The Sun Dial Press, Inc., Publishers.

15. Levi, Primo. 1960. If this is a Man. Translated from the Italian by Stuart Woolf. 2nd ed. London: Orion Press.

16. Malraux, André. 1934. Man’s Fate: La Condition Humaine. New York: Modern Library.

17. Marlantes, Karl. 2010. Matterhorn. A Novel of the Vietnam War. 1st ed. New York: Atlantic Monthly Press: Distributed by Publishers Group West.

18. MacLean, Alistair. 1955. H.M.S. Ulysses. London: Collins.

19. Monsarrat, Nicholas. 1951. The Cruel Sea. 1st ed. New York: Knopf.

20. Orwell, George. 1938. [1966]. Homage to Catalonia. (And Looking Back on the Spanish War). Harmondsworth, Middlessex, England: Penguin Books in association with Martin Segker & Warburg.

21. Remarque, Erich Maria. 1929. [1982]. All Quiet on the Western Front. New York: Ballantine Books.

22. Remarque, Erich Maria. 1954. A Time to Love and a Time to Die. Translated from the German by Denver Lindley. New York: Harcourt Brace.

23. Wouk, Herman. 1951. [2003]. The Caine Mutiny. A Novel of World War II. 1st ed. Boston, MA: Little Brown and Co.

24. Wouk, Herman. 1971. The Winds of War: A Novel. 1st ed. Boston: Little Brown.

25. Wouk, Herman. 1978. War and Remembrance: A Novel. 1st ed. Boston: Little Brown.

February 2, 2021 at 3:33 pm in reply to: Dominant Capital is Much More Powerful Than You Think #245264Thank you Blair for the interesting question.

In principle, the relevant universe is open-ended and depends on the question we seek to answer. In our work here, we compared the top corporations to all corporations. You suggest that the results might differ if we compare the top corporations to all firms — incorporated as well as unincorporated. The impact of this change can be assessed with additional research.

Some preliminary thoughts:

Your chart on ‘average firm size’ in the U.S. suggests that, compared to 1950, this size rose by about 80%. But your chart measures size in terms of the number of employees, whereas our paper here looks at size in terms of dollar amount of income — in this case, profit. And the temporal movement — and even the direction — of these two measures need not be the same.

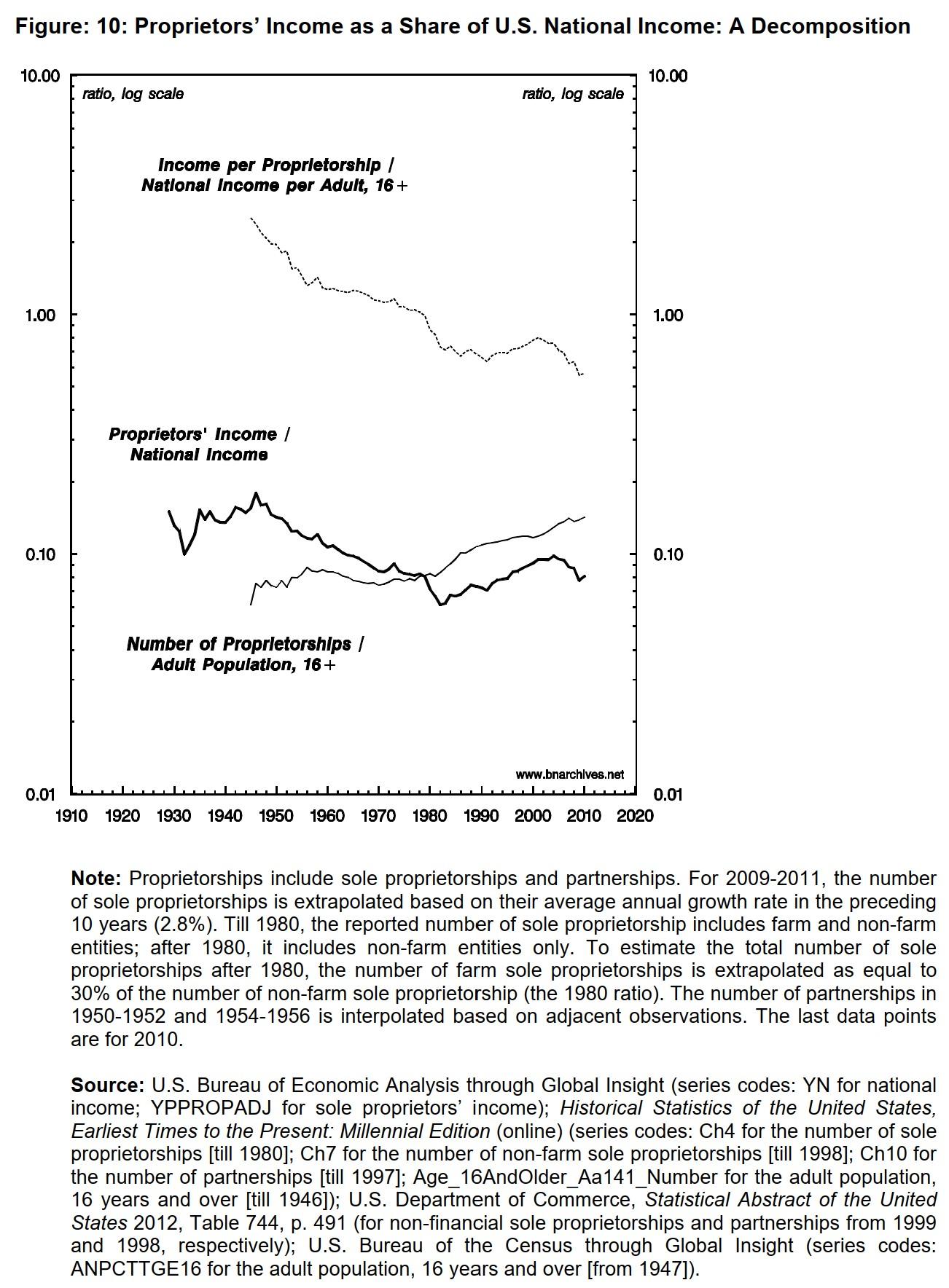

In our own 2012 paper ‘The Asymptotes of Power‘, we looked at proprietors’ income.

Figure 10 below shows that, while the number of proprietorships per adult has risen (solid thin line), overall proprietors’ income as a share of U.S. national income fell by more than 40% (thick line) and the ratio of income per proprietorship relative to national income per adult (dashed line) fell by about 75% (these percentages are all ballpark figures). So my initial impression is that the relative income size of proprietorships is falling even if their absolute employee size is rising.

Of course, the precise way in which these trends relate to the measures of our paper requires further empirical work.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

Merridale, Catherine. 2006. Ivan’s War. Life and Death in the Red Army, 1939-1945. 1st ed. New York: Metropolitan Books.

There is a huge literature on Soviet side of WWII. But this book is unique in its focus on the Soviet soldiers. Merridale, a British historian, conducted numerous interviews with war veterans and ordinary people who experienced the war first hand and weaved their recollections and thoughts with the broader history of the conflict. It reads like a story from another planet. Riveting and horrific.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

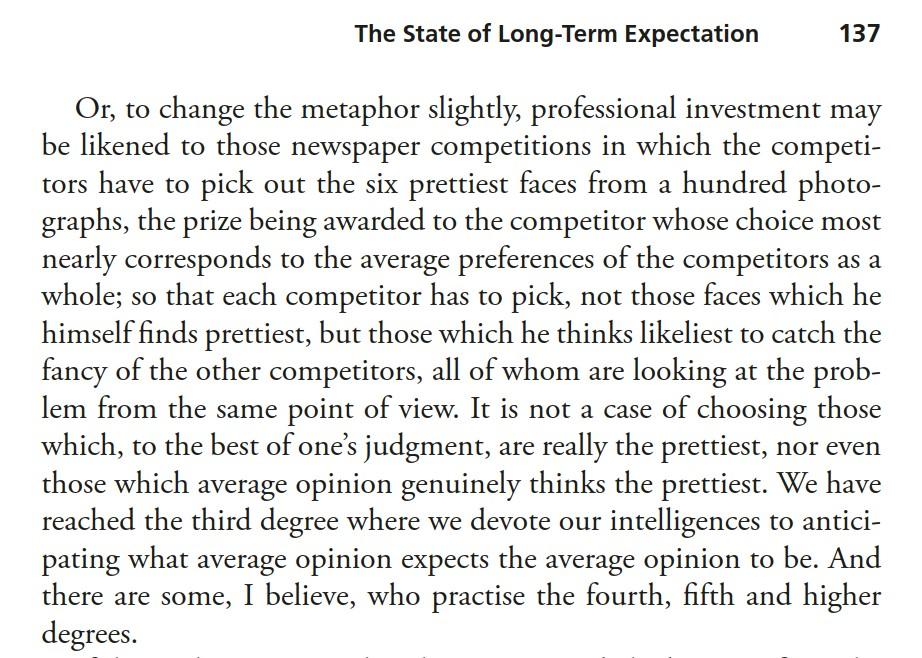

January 31, 2021 at 10:37 am in reply to: GameStop, hedge funds, and the “reality” of the stock market #245246The question is what do stock prices ‘represent’?

According to Keynes, in his General Theory, the answer is a differential guess about what others think they represent:

This tongue-in-cheek seems reasonable a description for short-term investment and for particular stocks, but over the longer term and for broad aggregates, investors price stocks by discounting risk-adjusted expected future earnings. In most cases, prices correlate positively with earnings expectations, and negatively with risk perceptions and the normal rate of return. The correlations themselves — particularly between prices and earnings — can change over time (see Figures 7 in our CasP Model of the Stock Market), but they tend to be positive.

From a capitalization perspective, terms such as ‘manias’, ‘bubbles’ and ‘irrational exuberance’ represent excessive profit expectations — or rising ‘hype’. Of course, most frenzied investors who buy into these upswings don’t think of future earnings. They follow Keynes’ narrative. But in their actions they drive up – and are further driven by — the hype.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

January 30, 2021 at 11:19 am in reply to: GameStop, hedge funds, and the “reality” of the stock market #245240Market tops are congested with hype-laden fanfare and scandals, which is where the ‘shoe shining boy’ theory of financial investment kicks in.

The theory, which many an exist-in-time mogul claim their own, posits that when you start getting investment tips from shoe-shiners and other folks who normally just work for a living, it’s time to sell your equity holdings.

-

AuthorReplies