Forum Replies Created

-

AuthorReplies

-

I look forward to your take on the conversation and the hurdles for CasP it points to.

Thank you for the question. Could you please elaborate?

October 17, 2024 at 8:01 pm in reply to: The dark matter of CasP? What can’t we observe about capitalist power? #250159The ‘dark-matter’ syndrome is inherent to scientific modelling. All scientific models are wrong to some extent – either because the modellers exclude important elements and misrepresent or omit relevant relations, or because they over-simplify. The built-in errors are not always apparent — for example, initially, Ptolemaic cosmology seemed superior to the heliocentric one. And often the errors are being hidden by inventing new terms, such as Phlogiston in chemistry, the production-function ‘residual’ in economics, and (perhaps) the ‘dark matter’ of cosmology.

I think that, as a new approach with few researches and a very limited number of studies, CasP must be full of dark matter, residuals and Phlogiston-like substances. And I suspect that its unknowns extend far beyond the black and grey economies and unreported activities. In the grander scheme of things, CasP theory is still in its early sketching stages, and even its most brilliant studies merely scratch the empirical surface.

But there is an upside. Unlike neoclassical theory, which gave up science in defence of capitalism, and contrary to Marxism, which has been impaired by dogma and/or surrendered to postism, CasP is still young and uncommitted and therefore able to plow through many of these difficulties — at least for the time being!

- This reply was modified 1 year, 8 months ago by Jonathan Nitzan.

Svetlana Alexievich’s Secondhand Time chronicles the transition from the Soviet mode of power to Russia’s new capitalist mode of power. And it is unique because it is written not from the top, but from the bottom. The book is a collection of interviews conducted over a period of more than twenty years following the fall of communism. Alexievich spoke with many people from all walks of life, old and young, communist and anti-communist, those who lived in the Soviet Union and others born after its collapse. None of them belonged to the elite. They were all from the underlying population.

The stories are riveting, sometime mind-bending and often horrific. They are also very diverse and therefore difficult to generalize, certainly not after the first read.

But one lesson seems clear: hierarchical modes power, be they communist, capitalist or something else, are incredibly powerful. Stalin’s regime, like its tsarist predecessors, managed to butcher, enslave, terrorize and condition Russians in the millions. And the capitalist oligarchs and their current czar, Putin, use new social technologies to achieve similar ends.

Faced with these mega-machines, the path toward direct democracy is daunting indeed.

- This reply was modified 1 year, 8 months ago by Jonathan Nitzan.

- This reply was modified 1 year, 8 months ago by Jonathan Nitzan.

I agree with your hesitancy, James. However.

I think Whitehead did a very good job describing the mental state on which U.S. slavery was built.

I thought that the most unsettling parts of the book were those describing the honorific cruelty against captured runaway slaves, cruelly that often served as lunchtime entertainment for the puritan masters and a stern warning to their remaining slaves.

This cruelty was made possible by seeing slaves as ‘non-persons’. Even where salves were liberated, like in North Carolina, they were often turned into state property, and, as such, were fair game for biological experimentation.

Slave hunters continued to operate in ‘free states’, where slavery was prohibited, on the premise that the sanctity of property trumped over the sanctity of life. These hunters acted like ‘private’ IRS or FBI agents, with trans-border privileges, to find and return runaways to their ‘legal owners’.

Finally, and perhaps most devastatingly, the slaves themselves often lacked the most basic sense of self. Families disintegrated, children were sold, parents were murdered. There was no ‘community’, let alone a stable one, so there was no social locus to relate to and construct one’s own social personality.

- This reply was modified 1 year, 8 months ago by Jonathan Nitzan.

- This reply was modified 1 year, 8 months ago by Jonathan Nitzan.

- This reply was modified 1 year, 8 months ago by Jonathan Nitzan.

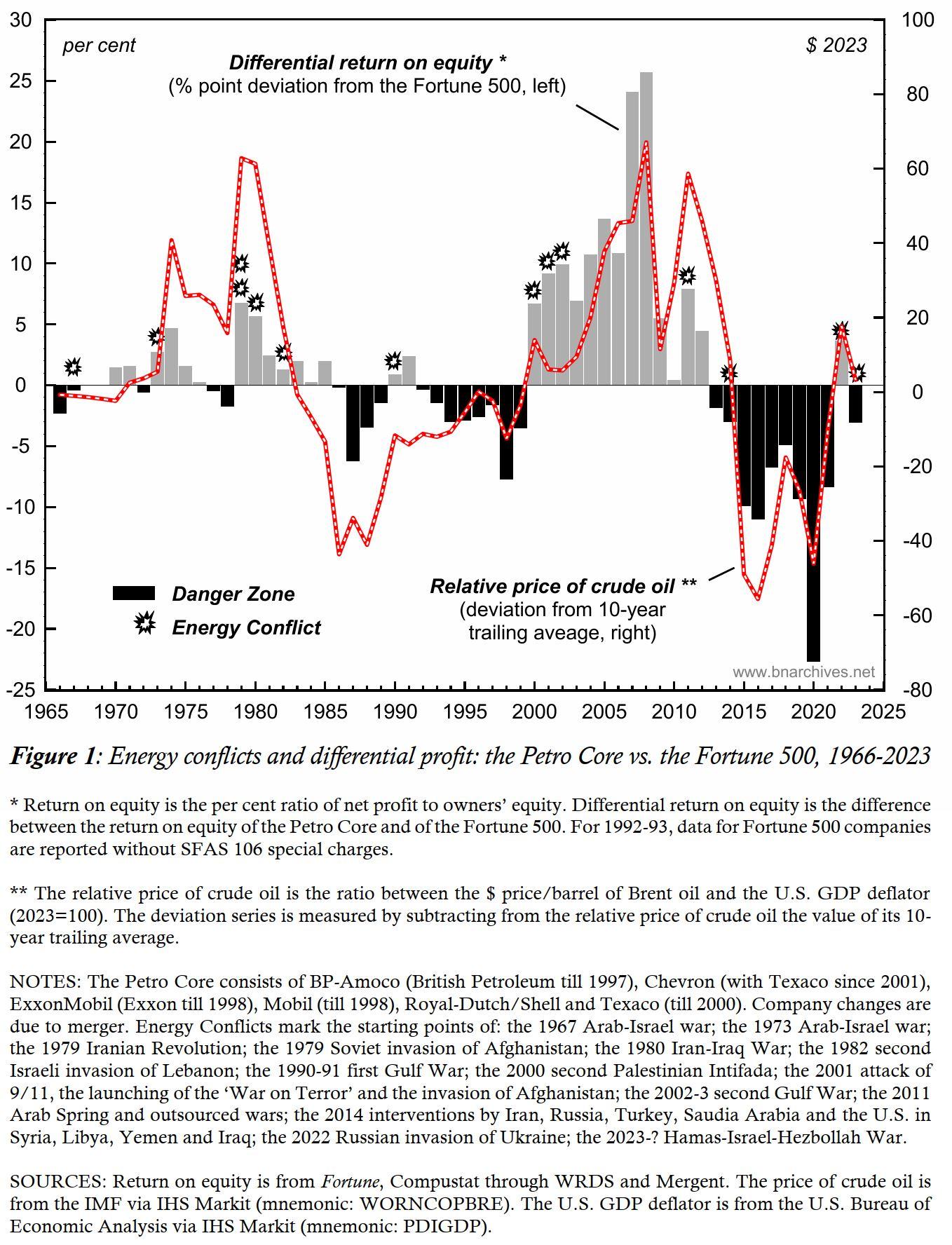

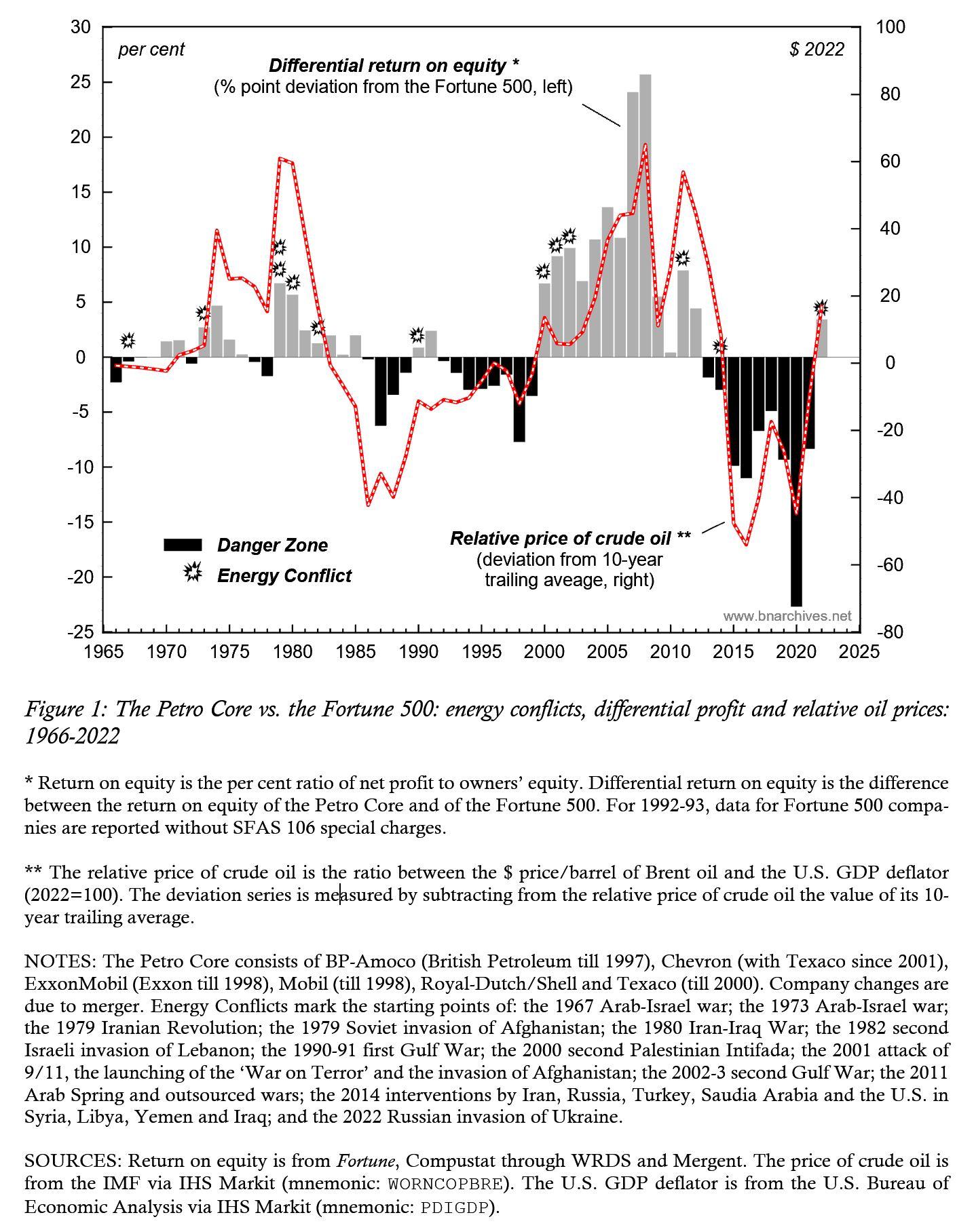

Blood and Oil in the Orient: A 2024 Update

After years of falling relative oil prices and differential oil losses, the 2022 Russian invasion of Ukraine boosted both and helped pull the Middle East out of its ‘danger zone’.

A year later, the war that broke out between Israel on the one hand, and Hamas-Islamic Jihad-Hezbollah-Iran on the other, promised to increase those relative prices and differential returns even further.

But these hopes were dashed.

As the figure below shows, in 2023, relative prices and differential profits both sank, pushing the Middle East once again into the ‘danger zone’.

- This reply was modified 1 year, 10 months ago by Jonathan Nitzan.

- This reply was modified 1 year, 10 months ago by Jonathan Nitzan.

Jiang, Rong. 2008. Wolf Totem. Translated by Howard Goldblatt. New York: Penguin Press.

A semi-autobiographical novel about a Chinese student sent during the Cultural Revolution of the 1960s to live as a herder in Inner Mongolia.

The broader context is the impact of population growth on the changing balance between agricultural and nomadic life and the inevitable destruction of the latter by the former.

The focus is the radically different worldviews of the two groups — the complex, long-term holistic perception of the nomads versus the one-dimensional, short-term emphasis on the farmers.

The main axis are the wolves: their pivotal role in regulating the ecology of the steppe, their impact on the consciousness and behaviour of both humans and animals, and their lasting imprint on the historical development of Mongolia and beyond.

Thrilling.

- This reply was modified 2 years ago by Jonathan Nitzan.

- This reply was modified 2 years ago by Jonathan Nitzan.

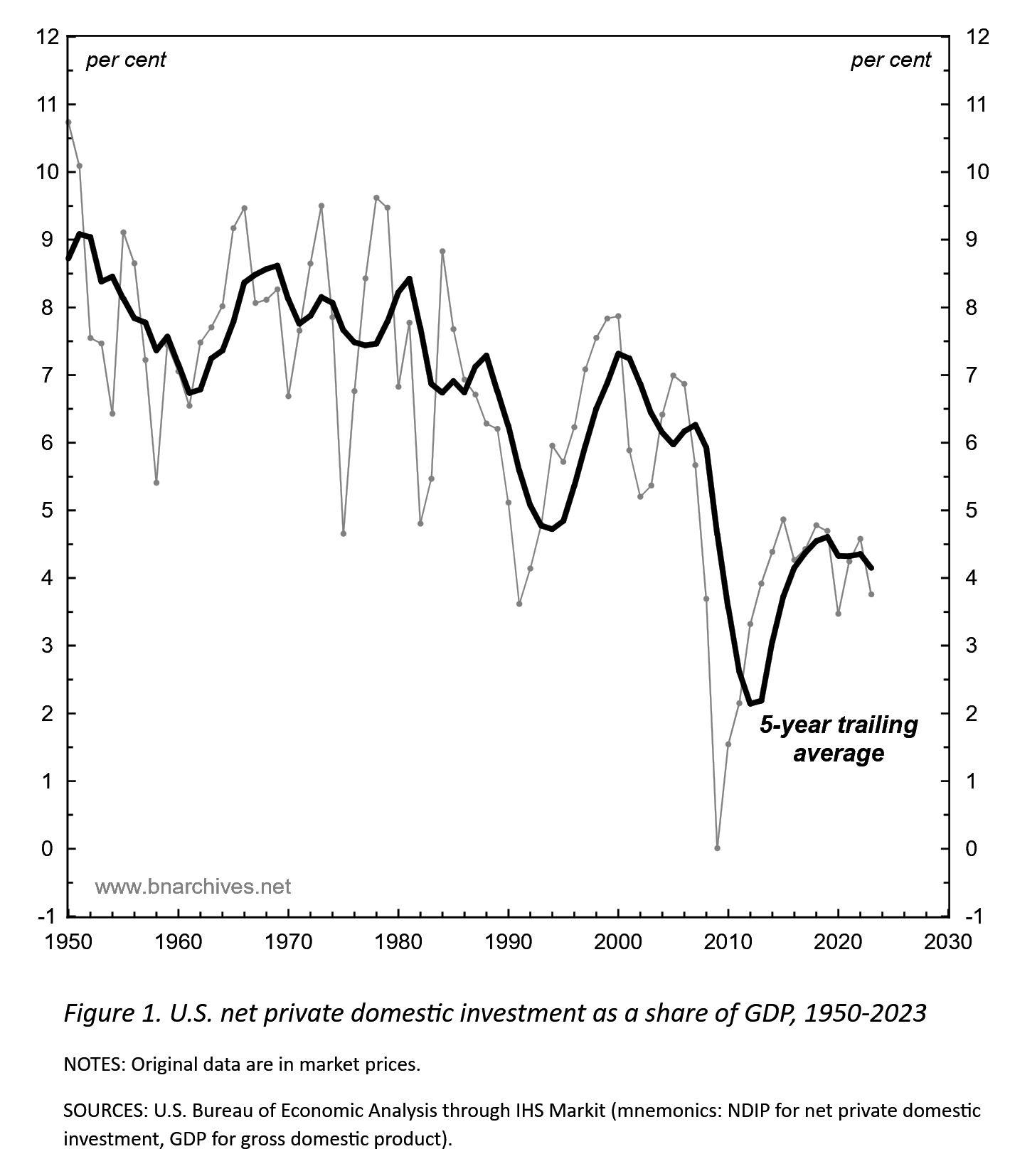

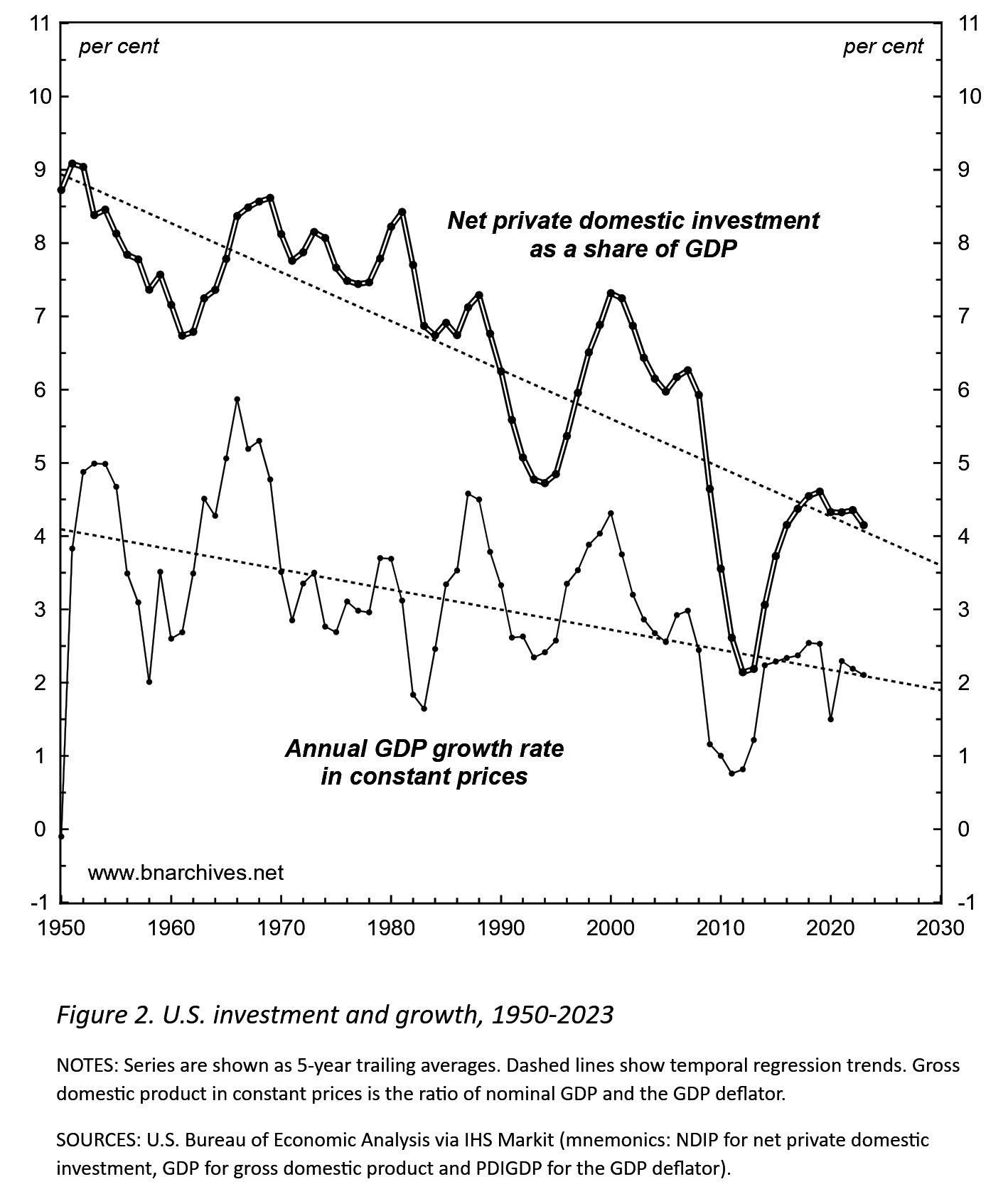

True — but (1) a significant part of this increase is due to input-price inflation, and (2) construction is roughly 4% of U.S. GDP, so its impact on the overall growth trend is limited.

The ‘external breadth’ of accumulation can be measured in different ways. Here are two simple figures to put the prospects of a new U.S. external breadth regime in historical context.

Figure 1 shows U.S. net private domestic investment as a share of GDP (gross investment less depreciation). Figure 2 contrasts this share with U.S. GDP growth.

Both series show long-term deceleration. They also don’t indicate recent upticks.

Here is the relation between the Petro-Core’s differential earnings, energy conflicts and the relative price of crude oil.

- This reply was modified 2 years, 6 months ago by Jonathan Nitzan.

Pertaining to the second question, it would then seem that there is not much separating CaSP from say Marxist opposition to capital, other than the theoretical conception of the system, right? Beyond that, it seems you are both fighting the same cause.

Given that actual Marxist-informed regimes have tended to develop into dictatorships, I very much doubt that CasP and Marxists are ‘fighting the same cause’.

Dear Byron,

I don’t know how much you know about CasP, so my answers here are very general.

1) How does CaSP interpret headlines of S&P upgrades and credit ratings in general? Within the CaSP framework, what do these indicators mean, and what are their effects for the broader political economy, its population, businesses, and governments.

When I worked at the BCA Research Group, most editors dismissed the rating agency reports as lagging indicators: belated reflections of what the ‘market’ (read analysts and capitalists) has already expressed through the buying and selling of financial assets weeks and months earlier. I agree with this assessment, though I’d add that the rating agencies do serve a role: they offer a consensus benchmark for the ‘appropriate’ lending/borrowing premiums for different countries and companies. In generating this benchmark, though, the rating agencies – just like the capitalist organizations and governments they serve – are slaves to the capitalized worldview and rituals that CasP analyzes and criticizes. In this sense, the common bedeviling of these agencies as a discretionary imperial hand of the West is exaggerated if not totally misplaced in my view.

2) Does CaSP offer any new ways of acting within capitalism? Whether resisting it, or working with it, does CaSP offer new ways for the proletariat or businesses? Or does it only offer a better theoretical understanding of capitalism?

As advocates of human autonomy and voluntary collaboration, Shimshon and I resent power and sabotage as such. And as scientists, our research tells us that the effect of capitalized power on much of humanity and its environment tends to be negative and — because capitalized power knows no bounds — potentially disastrous (I use ‘tends to’ and ‘potentially’ because the issues here are never simple). For these reasons, we think capitalism should be changed and, if possible, replaced by a more autonomous and directly democratic human collaboration. And although we haven’t done much work on this subject ourselves, the very gist of CasP research indicates, by way of negation, what a better society might want to resist and move away from.

Form more on these issues, see our 2018 paper, ‘Theory and Praxis, Theory and Practice, Practical Theory’ https://bnarchives.yorku.ca/539/

As a bonus, it would be nice to relate answers to other political economic theories (Marxism and Liberalism).

On the relation between CasP on the one hand and Marxism and liberalism on the other, see our 2023 piece: ‘The Capital As Power Approach. An Invited-then-Rejected Interview with Shimshon Bichler and Jonathan Nitzan’ https://bnarchives.yorku.ca/799/

September 30, 2023 at 7:12 pm in reply to: Mark, Engels, and Public/Private Credit as Power Index Precursor #249804Nice be so highly graded, if only among the non-sequiturers!

September 28, 2023 at 7:48 pm in reply to: Mark, Engels, and Public/Private Credit as Power Index Precursor #249800The tail that wags the dog?

The accumulation of ‘actual’ capital is counted in backward-looking labour time, while the confidence of the accumulators relies on the forward-looking ‘fiction’ of credit (or the other way around). Adhering to this house of mirrors keep Marxists stuck in no-man’s land….

- This reply was modified 2 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 2 years, 8 months ago by Jonathan Nitzan.

1. It would be nice to offer solutions, but first we need to convince our audience there is a problem. We have been trying to do so for over 40 years, and truth be told, it seems that we don’t even have an audience…. For example, our 2022 Hebrew book, Capital and its Crisis, received a grand total of zero reviews. We continue to research and publish regardless; but our ability to influence the course of history seems rather limited.

2. On a more positive note, have a look at our 2018 paper, ‘The CasP Project: Past, Present, Future‘. Section III: Future, suggests seven research trajectories. Pursuing them might help construct a better world (if you prefer watching, here is the video).

3. And then, there is the younger generation of brilliant CasPers, whose research is almost always impressive and occasionally mind boggling. A lot of promise there, or so I hope!

- This reply was modified 2 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 2 years, 9 months ago by Jonathan Nitzan.

-

AuthorReplies