Forum Replies Created

-

AuthorReplies

-

Thanks, Max.

Granted. But all the examples you provided are “short-term” fluctuations which are easily “explained” by all sorts of regular “market failures”. I was asking about the “long-term tendency of the oil business…” because I think it’s somewhat harder, for the neoclassicists, to brush away the problem in the same manner. And I was wondering if you encountered any concrete examples of them trying to tackle the subject head-on.

No, we haven’t encountered neoclassical attempts to tackle long-term ‘distortions’ head on — either in the oil sector or elsewhere. And I can think of two reasons why. One is that distortions are external to their theory and often to economics more generally, so they are ill equipped to explain them. The other and more important reason is that they cannot even observe let alone measure their own explanatory variables of demand/supply/equilibrium, so how can they pin down their presumable aberrations?

Wouldn’t you agree that without renewed qualitative research into the subject (like the one you and Shimshon conducted more than 20 years ago), and given the somewhat fuzzier quantitative results (see my remark above, about “varying time lags for different “danger zones””) — the interpretation seems a bit less persuasive than it used to be?

Of course, new research, both qualitative and quantitative, is welcome and indeed necessary. Regardless of whether our work was and/or remains persuasive, it barely touched the surface of these central processes. Plus, the world keeps changing.

- This reply was modified 1 month, 1 week ago by Jonathan Nitzan.

- This reply was modified 1 month, 1 week ago by Jonathan Nitzan.

From CasP perspective, is it basically mainstream economists “discovering” strategic sabotage?

From Shimshon and Jonathan:

1. In our view, the underlying framework of mainstream economists makes it difficult if not impossible for them to ‘discover’ strategic sabotage — at least not in the sense that CasP uses it.

2. All neoclassicists agree that, unfortunately, power exists; that, unfortunately, it distorts markets; and that, unfortunately, it generates imperfections. Some of them – in this case, Acemoglu & Restrepo — try to measure these power distortions (in their case, struggles over ‘rent’ that is ostensibly collected by workers) and assess their negative effects.

3. To do so, they measure power and its distortion as residuals: they (i) relate actual incomes (which are presumably distorted by power) to theoretical incomes (which would exist in perfectly competitive markets, where factors of production get remunerated proportionately to their marginal ‘real’ contributions); (ii) interpret the resulting residual (expressed as a ratio or difference) as a measure of power; and (iii) relate this residual to various phenomena to assess the effect of that power.

4. The problem is that, since perfect markets do not exist, and given that nobody can measure ‘real’ economic quantities, let alone the alleged contributions of their factors of production, the ideal income benchmark – along with its power-distorted residuals – are effectively assumed out of thin air.

5. The CasP approach is very different. Not only does it reject the measurability of ‘real’ output and the existence of individual productivity, but it also argues that relative incomes are determined by the ability of different groups to differentially sabotage the integrated process of societal reproduction. With these fundamental incongruences, it seems that the only way for neoclassicists to ‘discover’ CasP’s notion of strategic sabotage is by rejecting their own framework and adopting ours.

6. Note that the barriers imposed by one’s initial framework are not limited to neoclassicists. Critical political economists – including Marxists, neo-Marxists and institutionalists – are limited by them as well. Here is how we summarized the difficulty on Page 142 of our 2023 paper, ‘The Capital as Power Approach’:

For Kalecki, as for Veblen, accumulation is an absolute process of amassing more and more claims on real assets. In this context, power, however important, is a means to an end, not the end itself. And this assumption leads to conclusions that are opposite to ours. For instance, in his paper ‘Political Aspects of Full Employment’, Kalecki argues that under certain circumstances — such as a long boom that empowers workers — capitalists would willingly sacrifice profits to defend their hegemony.[1] A similar view is marshalled by Stephen Marglin, who claims that capitalists often forego efficient innovations to safeguard their overall power.[2] And the same perception underpins the broader Monopoly Capital notion of an underconsumption crisis, where the increased power of capitalists, revealed by their higher degree of monopoly, undermines their ultimate interest in growth-led accumulation.[3] On these matters, CasP argues instead that capitalists scarcely sacrifice their accumulation interests to regain their power. They don’t have to. Their very differential capitalization is driven by and represents their power to start with.

Notes

[1] Kalecki, Michal. 1943. [1971]. Political Aspects of Full Employment. In Selected Essays on the Dynamics of the Capitalist Economy. 1933-1970. Cambridge: Cambridge University Press, pp. 138-145.

[2] Marglin, Stephen A. 1974. What Do Bosses Do? The Origins and Functions of Hierarchy in Capitalist Production. Review of Radical Political Economics 6 (2, July): 60-112. https://scholar.harvard.edu/marglin/publications/what-do-bosses-do

[3] Bichler, Shimshon, and Jonathan Nitzan. 2014. How Capitalists Learned to Stop Worrying and Love the Crisis. Real-World Economics Review (66, January), Box 1, p. 69. http://bnarchives.yorku.ca/390/

- This reply was modified 1 month, 2 weeks ago by Jonathan Nitzan.

Thank you, Ulf. It’s always good to hear from you.

A few general points before turning to your individual items.

A. We (Shimshon and I) see capitalism as a totalizing mode of power which emerged in the European Bourgs sometimes in the 14th century, spread throughout the world and is now the dominant way of organizing society everywhere.

B. The key interrelated features of this mode of power are: (i) that it is organized quantitatively; (ii) that its unit of organization is money price; (iii) that organized power gets increasingly quantified as ‘privately owned’ (read exclusionary) capitalized assets; (iv) that capitalized power gets measured and assessed differentially, relative to other capitalized powers; and (v) that this power is created and modified through various forms of strategic sabotage.

C. These power features of capitalism, we argue, are universal and dominant everywhere. But they are also intertwined in various ways with both non-capitalized forms of power as well as collaborative forms of social relations, and the differences between the resulting combinations account for the so-called ‘variety of capitalism’ around the world (say, United States vs China vs Iran vs India vs. Brazil, etc.)

D. Our own research of the capitalist mode of power focuses mostly on the generalized, quantified features listed in (B), trying to discover and analyze the relations between differential capitalization and its components on the one hand and their underpinning strategic sabotage on the other. We often contextualize our analysis in relation to various ‘agents’ – capitalists, state officials, political parties, church leaders, crime gangs, ideologues, etc. – but we view the actions of those agents mostly as enfolded in and derived from the mode of power they inhabit rather than as its causes.

E. Using this perspective, we discovered in the late 1980 and early 1990s a rather systematic relation between the differential profits of the large oil companies and exports of OPEC on the one hand and relative oil prices on the other, and we showed that their historical ups and downs have been closely connected with Middle East energy conflicts.

F. Contextualized within the broader political economy of the Middle East, the heart of this research relies on the universal properties of the capitalist mode of power. And with this analytical hierarchy in mind, the question of whether the relevant energy conflicts have been caused – ‘manufactured’; ‘engineered’; ‘triggered’; etc. — by certain entities/persons is superfluous to our findings and, more importantly, apparently impossible to answer objectively. (What constitutes the ‘manufacturing’ of a conflict? Who/what count as the ‘engineers’ of a given conflict? How do you weigh the conflict’s various ‘triggers’?)

***

1. Do you think that Petro Core manufactured the Iran war to generate higher profits? (Werner Rügemer sent me this question.)

To reiterate our preamble, we don’t know – and doubt that this is a knowable fact to start with – who ‘manufactured’ the U.S.-Israel-Iran-Hezbollah war, and whether these ‘manufacturers’ have done it to boost their profits (absolutely and/or relatively).

Similarly to Poulantzas’ critique of Miliband, our work has focused less on agency and more on the structure (or rather on the re–structuring, or better still, on the creordering) of Middle East energy conflicts as a major form of strategic sabotage. Since the mid-1980s, characters of the Trump and Netanyahu type have played a rather minor role in steering the neoliberal regime: much like small market investors, they have tended to react rather than dictate its major processes — and that remains true in their current skirmishes with the oligarchies in Iran and the rest of the region.

What we do know, though, is (i) that, like in the past, the differential profits of the oil companies, both in the United States and globally, predicted the current round of regional hostilities; and (ii) that in due course, it will be possible to infer the correlations between relative oil prices and differential earrings across the political economy — correlations that will in turn tell us, however tentatively, who benefited and who lost from the conflict.

2. Is it just about oil prices or also who makes the profits? If American-based investors profit from (expensive) fracking products but not chaep Iranian oil that goes straight to China, wouldn’t there be an incentive to specifically target Iranian production units?

In our view, price is a means to the end of differential capitalization (determined by differential future earnings, hype and risk). A rise in oil prices ripples throughout the political economy, boosting the differential capitalization of some entities, while undermining that of others. And, in principle, all those affected have reason to support/oppose higher oil prices, though only very few have the ability to do something meaningful about it.

3. What is the role of “capital organizers” (Werner Rügemer) like Blackrock, Vanguard etc. in current global capitalism? Rügemer in “The Capitalists of the 21st Century” argues that these now organize the direction of capitalist development with their sheer weight of “wealth” (“capital might” as I like to call it, see my essay from 2019). Blackrock alone operates $12 trillion. (a) https://norberthaering.de/en/news/capitalists-of-the-21st-century/

In the past, the experts spoke about ‘rating agencies’, like S&P Global, Moody’s and Fitch, as the whips that kept states and corporations in line with neoliberalism, while now many love to blame mutual and pension funds like Blackrock, Vanguard, Fidelity, State Street and JPMorganChase for promoting financialization and undermining the good-old productive capitalism.

In our view, these claims, both old and new, seem to put the cart before the horse. As we see it, it’s not the rating agencies and fund managers that impose capitalization on the world, but rather it is capitalization that rules the heart and mind of the modern capitalist subject, including those of the owners, managers and analysts of the rating agencies and fund managers.

4. Your analysis is based on stock and other data. But I understand that this is mostly US data. How can you know that accumulation regimes e.g. in China or Russia is based on the same interests?

You are correct.

As a preamble, we haven’t analyzed the capitalist mode of power in either China or Russia, and it is certainly high time for others like yourself to do so – hopefully with the aid of new data, new sources and new methods that go beyond the more traditional means employed in our own research.

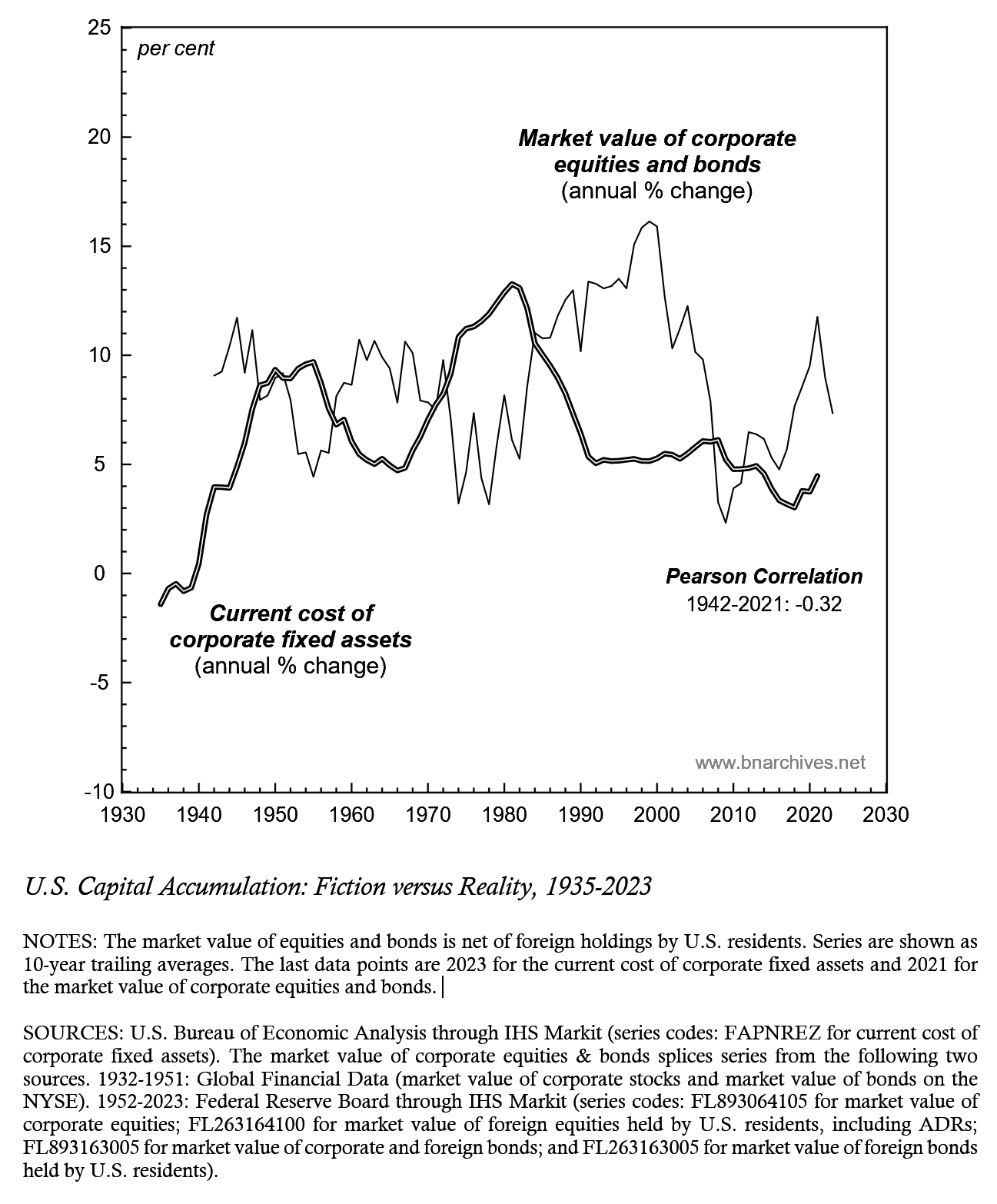

And to your point: it is indeed likely that Russian capitalism with its heavy reliance on oil exports and China with its heavy dependence on oil and other energy imports relate to the price of oil differently than the United States does. (That being said, though, note that Figure 2 above, which is based on global profits, yields pretty much the same results as Figure 1 which focuses mostly on U.S. profits.)

5. Related to 4. Would it be conceivable that there is a bifurcated structure in the global “state of capital” with “America” and “China” being distinct “state platforms” but the latter has so far escaped your largely US-based analysis? (a) https://journals.sagepub.com/doi/10.1177/0308518X221146545 (b) https://doi.org/10.1080/14650045.2023.2253432

Yes, on the face of it, the Chinese and American versions of the state of capital seem different. However, I’d venture to say that the differences between the two versions are probably far smaller today than they were half a century ago. On this subject, see our 2010 ‘Notes on the State of Capital’ https://bnarchives.net/id/eprint/282/

6. What is the role of long term power projections of US military planning units like T2COM, e.g. “Win in a Complex World” with its time frame from 2020 to 2040, in your energy-conflict scenario? According to e.g. Wolfgang Effenberger the current Iran war fits to the general time frame of that document suggesting that it is not “just” about oil but US global dominance. (a) https://www.army.mil/article/288779/turning_the_page_tradoc_inactivation_marks_new_chapter_in_army_transformation (b) https://ntrl.ntis.gov/NTRL/dashboard/searchResults/titleDetail/ADA611359.xhtml

We have not studied the subject and therefore cannot comment on it.

7. What do you think of the “Omniwar” concept by David Hughes? (a) https://dhughes.substack.com/p/omniwar-exposing-and-ending-the-invisible

We haven’t read Hughes’ book, but it seems to us that the ‘omniwar’ of the rulers against their subjects started not in the 21st century, but six millennia ago, with the rise of the first statist mode of power in Mesopotamia and Egypt.

- This reply was modified 2 months ago by Jonathan Nitzan.

- This reply was modified 2 months ago by Jonathan Nitzan.

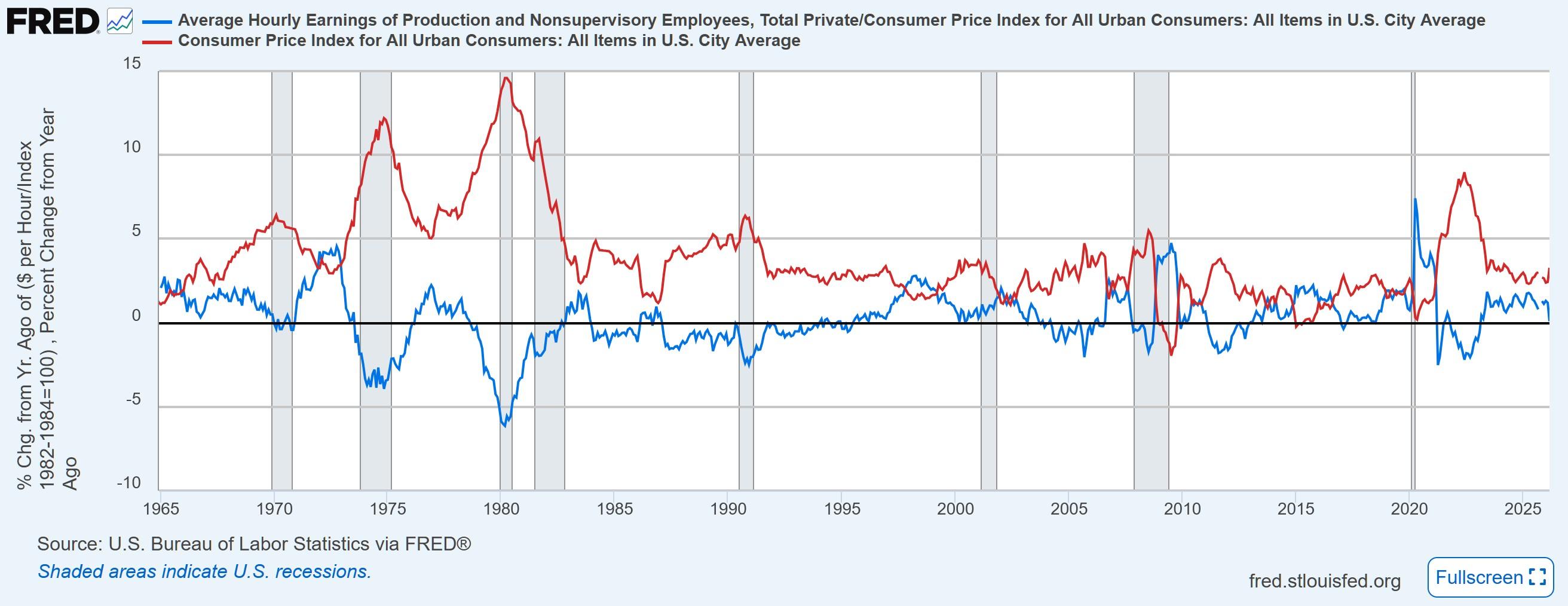

April 11, 2026 at 6:44 pm in reply to: Inflation is always and everywhere a redistributional phenomenon #250581Back in June 2022 we suggested — and in retrospect, correctly — that because inflation redistributes earnings away from workers, the post-Covid bout of inflation would be self limiting.

Now it seems that the same thing is likely to happen if the ongoing Middle East energy conflict (U.S. & Israel contra Iran) were to rekindle another overall surge in prices.

U.S. workers are in no position to retort meaningfully to such a price surge, which means that there will be little or no price-wage spiral and therefore no protracted rise in inflation. Instead, the short general bout of price increases will redistribute income from workers to capitalists, and then the rate of inflation will subside.

Custom graph link: https://fred.stlouisfed.org/graph/?g=1UEp0

- This reply was modified 2 months, 1 week ago by Jonathan Nitzan.

1.

Sure, but also besides the point is the neoclassicist view in toto. This argument can come as easily from a neo-Marxist, assuming chronic over-production in the oil industry; or just any skeptical radical, taking the analysis on its own terms.

Yes. Neo-Marxists, skeptical radicals and others can make these arguments. But it seems to me that in making them, they would reiterate or concur with the neoclassicists.

2.

Though I’m curious, how do those “hard-core neoclassicists” explain the long term tendency of the oil business to revert (between “external shocks”) to uncompetitive capital returns? Surely, it can’t be explained as a result of low risk. So why does the dis-equilibrium over-capacity persist?

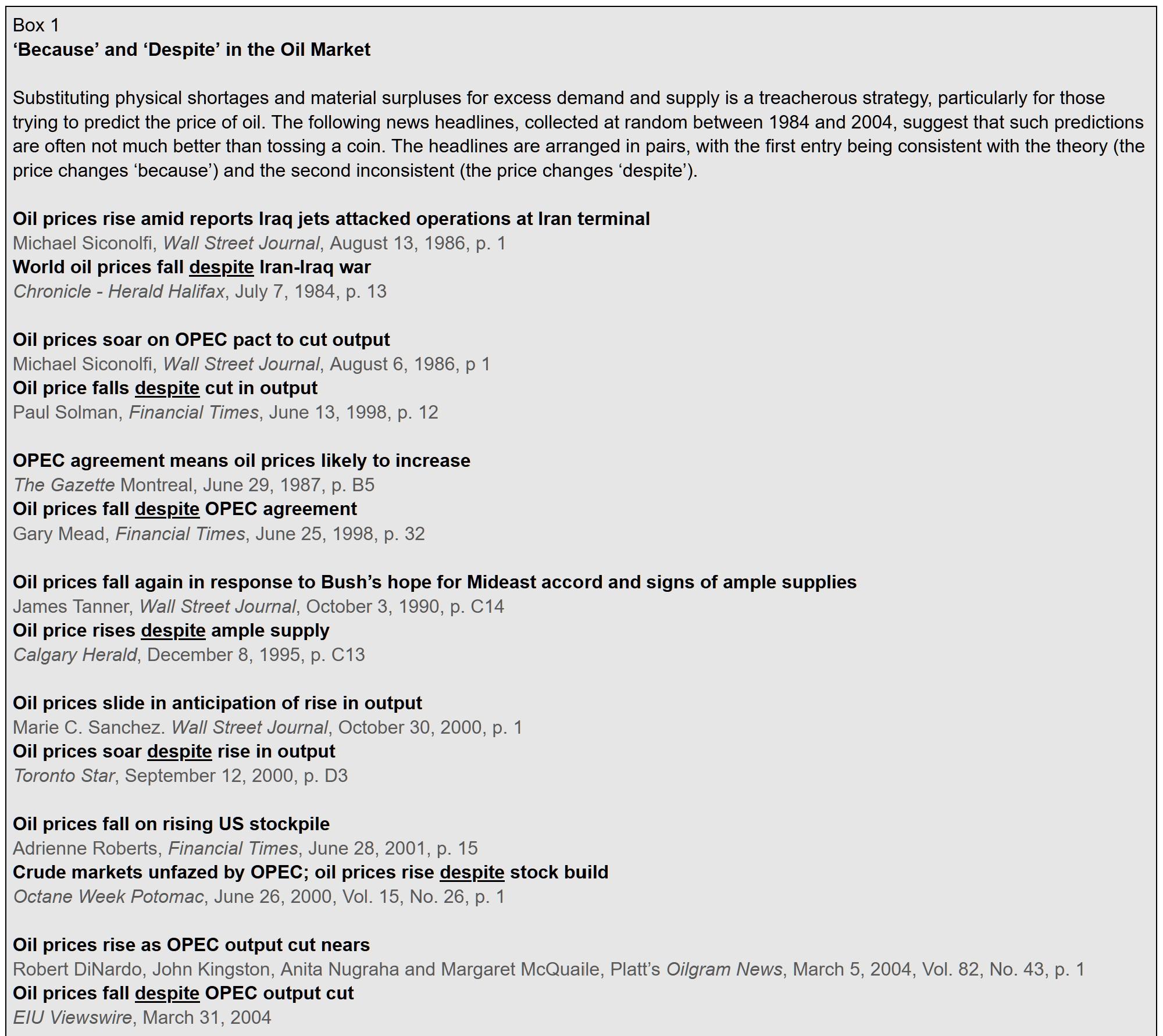

As we see it, the terms ‘uncompetitive returns’, ‘low risk’, ‘dis-equilibrium’ and ‘over-capacity’ are neoclassical images with no objective empirical contents. Neoclassicists explain them, or use them to explain other things, but without being able to prove or refute their explanations. Here is how it works (or rather doesn’t) with respect to oil prices: https://bnarchives.net/id/eprint/432/

3.

Regarding ‘danger zones’. The difficulty here is that causality cannot be scientifically proven. In terms of the correlations we present, most people are likely to treat ‘energy conflicts’ as relevant but exogenously determined, as you suggest. We think they are causally intertwined with the high politics of differential oil prices and profits. Unfortunately, there is no way prove either of those causal views.

If we are to follow Occam’s razor, there is no need for “danger zones” as an element of a casual interpretation. The simpler explanation above should suffice: decumulation does not necessarily predict conflict, it’s just what we would expect when conflict subsides, and when war appears* (due to its own regional-internal reasons) the oil business simply hitchhikes on it to its differential benefit.

Of course you can make this argument.

In fact, this is what hard-core neoclassicists have insisted all along: (1) there is a pure economic system; (2) this system is subject to unfortunate exogenous shocks (intervening governments, labour unions, monopolies, the weather gods, and recently also oil sheiks, Islamic terrorists and similar irrationalities) (3) these shocks rattle supply and demand; (4) this rattling changes the equilibrium price and/or quantity; and (5) in the case of oil, these changes affect oil company profitability exactly as NC demand/supply/equilibrium theory would predict.

(Of course, the bifurcation between the pure economy and the rest of society is a pure economic fiction, as are the neoclassical concepts of demand, supply and equilibrium — though that, clearly, is besides the point https://bnarchives.net/id/eprint/722/).

January 17, 2026 at 7:29 pm in reply to: The dark matter of CasP? What can’t we observe about capitalist power? #250452A very enlightening and accessible exposition, Blair. Thank you.

- This reply was modified 5 months, 1 week ago by Jonathan Nitzan.

December 4, 2025 at 7:26 pm in reply to: The dark matter of CasP? What can’t we observe about capitalist power? #250426Yes, corporate delisting is ongoing, but it isn’t clear that ‘private capital’ is replacing or overpowers ‘listed capital’.

According to Siblis Research (https://siblisresearch.com/data/us-stock-market-value/), between 2012 and 2024, U.S. stock market capitalization more than tripled — from $18.7 to $62.2 trillion (though the rate of expansion might be different if we include outstanding credit and real estate).

See Section 5 in our 2019 paper, ‘Making America Great Again’ (https://bnarchives.net/id/eprint/630/)

- This reply was modified 6 months, 3 weeks ago by Jonathan Nitzan.

Keynes considered the accumulation urge useful in bringing humanity to a state of material bliss, after which it would be recognized for what it was — a pathological condition befitting the psychiatrist couch. Had he though about it as the power drive that organized the capitalist world, he wouldn’t conclude it could be easily discarded.

Interesting proposal, Pieter.

If I understand you correctly, your aim is to create a taxonomy for mapping the processes of coordination, of which power relations are a subset.

Two comments come to mind.

1. Regardless of its specific details, such taxonomy is likely to face the built-in challenge of quantifying qualities – i.e., of bringing the incommensurate aspects of coordination into one or more common denominators without which quantification and aggregation are difficult if not impossible.

2. In some sense, your universal articulation, however tentative, puts the analytical cart before the empirical horses. I think it would be useful – for yourself and for others – to concertize the elements of your proposal with empirical examples and/or research, so as to assess both their logical validity and empirical fruitfulness. In my own experience, concrete examples often proved a useful check against going astray.

- This reply was modified 1 year, 2 months ago by Jonathan Nitzan.

An empirical rather than analytical observation, right?

I think a bit of both.

1. Replacement cost is based on prices of newly produced capital goods. Unlike the prices of existing capital goods, which reflect the changing capitalization of their risk-adjusted expected earnings, among other factors, those of new capital goods are commonly ‘administered’ by their producers in line with normal cost and desired markup. During times of inflation and high interest rates, these administered prices tend to rise.

2. Market capitalization is affected by inflation positively (mainly by boosting expected profit in the numerator), as well as negatively (by increasing the discount rate in the denominator). However, the capitalization formula suggests that the latter (-ve) impact will usually outweigh the former (+ve) impact. For example, all else remaining the same, a 5% increase in expected future profit due to 5% increase in prices, accompanied by a 5 percentage points increase in the discount rate from 3% to 8%, will reduce capitalization by roughly 60%.

Obviously, these are partial back-of-the envelope arguments that invite further research….

Thank you for the thoughtful comments, Max. Here are three observations.

1. Our figure uses replacement cost because, in principle, this is what national-account statisticians use to impute the ‘real capital stock’ (= replacement cost / price index of investment goods). In other words, when economic researchers – be they NC or heterodox – use the ‘real capital stock’, they use not its utils or SNALT content, but the capitalized price of ‘capital goods’, corrected, or so they believe, for price changes. And since this ‘real’ measurement template applies not only to capital goods, but to all commodities, it follows that value theories are not only conceptually circular/arbitrary but also lack an objective measure to quantify the ‘real economy’ they theorize.

2. Why does the replacement cost of the capital stock oscillate inversely with corporate capitalization? Although we haven’t researched this question, one possible answer is the co-movement of inflation and interest rates, which tends to have a positive effect on the replacement cost of the capital stock and a negative impact on corporate capitalization.

3. You suggest that established heterodox political economists are busy analyzing the ‘distortions’ of finance and other extra-economic ills and are unaware of or indifferent to the fact that they do not have a consistent theory of value to stand on. I agree – but, based on our long experience, I don’t think this is a trap we can easily trick or lure them out of. We are likely to be better received by younger thinkers — though even here, the window of opportunity tends to close rather quickly.

“…the real capital stock, which political economists see as the beginning and end of capitalism, has nothing to do with (tangible) book value, which is the sole god of heterodox, anti-finance, economists.”

While this statement may be theoretically correct, it is NOT what we want to say.

Our point, rather, is that forward-looking capitalization and backward-looking real capital are de-linked (and in the U.S. case inversely correlated, as the figure below shows).

I think that Hudson’s reference to ‘book value’ here is misleading; as I indicated above, book value represents forward-looking capitalization at the point of its recording and therefore includes rent which Hudson wishes to exclude…. From his vantage point, it would be more accurate to talk of ‘real capital’, and specifically, of the direct + indirect ‘labour cost’ of producing it.

I think that Hudson’s reference to ‘book value’ here is misleading; as I indicated above, book value represents forward-looking capitalization at the point of its recording and therefore includes rent which Hudson wishes to exclude…. From his vantage point, it would be more accurate to talk of ‘real capital’, and specifically, of the direct + indirect ‘labour cost’ of producing it.- This reply was modified 1 year, 3 months ago by Jonathan Nitzan.

March 12, 2025 at 10:33 am in reply to: Capital as Power in the 21st Century: A Conversation #250239If I understand you correctly, your question concerns the difference between ‘real capital’ and ‘book value’.

REAL CAPITAL is an economic concept, denominated in universal units of either neoclassical utils or Marxist SNALT (socially necessary abstract labour time). The utils/SNALT presumably contained in any real capital were generated/produced in the past. Economists claim they can measure real capital, but as we explain in Chapter 8 of Capital as Power (2009), their measurement is entirely arbitrary if not circular.

BOOK VALUE is an accounting concept, denominated in dollars and cents. Usually, it denotes the money price of the asset at the time of its purchase. In Capital as Power (pp. 255-256) we note that book value represents the asset’s forward-looking capitalization at the time of its acquisition (the oil-tanker example). This feature means that, unlike the fluctuating market capitalization on the stock and bond markets, once set, book value no longer changes.

Are these two concepts related? Perhaps — but only in a perfectly competitive equilibrium with a perfectly known future (+ other assumptions that eliminate all resemblance to any known society).

- This reply was modified 1 year, 3 months ago by Jonathan Nitzan.

- This reply was modified 1 year, 3 months ago by Jonathan Nitzan.

Responding with fundamental critiques of neoclassical or Marxist value theories is not really effective in this context. So a reorientation of exposition and argument might be required if we to facilitate more fruitful engagements.

So far, our exposition — namely, a critique of existing neoclassical and Marxist frameworks and findings + an articulation of CasP’s own framework and research — seems to have resonated with young, free-spirited researchers (like yourself) and to have elicited more or less dead silence from established political economists.

So something in our exposition (and substance) speaks to one group while deterring another, and I wonder how you and others think this exposition can be ‘reoriented’ to make engagements more fruitful without diluting CasP’s contents.

- This reply was modified 1 year, 3 months ago by Jonathan Nitzan.

- This reply was modified 1 year, 3 months ago by Jonathan Nitzan.

- This reply was modified 1 year, 3 months ago by Jonathan Nitzan.

-

AuthorReplies