Forum Replies Created

-

AuthorReplies

-

January 29, 2021 at 4:21 pm in reply to: GameStop, hedge funds, and the “reality” of the stock market #245236

Thank you Jeremy and Blair.

Capitalization is the ‘operational symbol’, to use Ulf Martin’s language, that creorders the capitalist mode of power. If this statement is correct, abolishing financial markets implies abolishing capitalism, or at least changing it so drastically that it becomes unrecognizable.

In the last section of our 2018 paper, ‘Theory and Praxis, Theory and Practice, Practical Theory’, titled ‘bridgehead’, we suggested one possible first step toward that end. It goes as follows:

[…]

Bridgehead

These considerations make praxis crucially dependent on fusing political action with ongoing empirical and theoretical research. To illustrate this necessity to know what we are doing, consider the following thought experiment. What if, instead of creordering the entire fabric of society, we start with a narrow bridgehead? Rather than trying to revolutionize the whole thing, we focus on one well-defined sphere. We inject into this sphere greater autonomy, cooperation and creativity, and then gradually tie these changes with, pull in and transform additional social spheres and processes, as well as our very understanding of society.

One promising site for such a bridgehead is the intersection of housing and pensions. The rapid urbanization of the planet makes affordable housing a key concern – and increasingly an impossible dream – for most wage earners. Similarly with pensions. According to the International Labour Organization, the vast majority of the world’s working-age population – up to 90 per cent – is not covered by pension schemes capable of providing adequate retirement income (Gillion et al. 2000). Left unattended, these trends are akin to social time-bombs. Used wisely, though, they might offer a leverage for autonomous social change around the world.

If we could come up with a democratically managed system that ploughs pension contributions into affordable housing and uses mortgage repayments and rent to pay pensioners, we might be able to align with and mobilize large chunks of society. And that’s just for starters. Affordable housing can be tied to sustainable urban planning, with creative architecture and new forms of public transportation to counteract and reverse the ecological devastation ushered in by uncontrollable sprawl. Those who live in autonomously developed urban areas and experience the democratic process might in turn wish to reform the educational system and broaden their self-government. The conceptual challenges created by a democratically managed pension-housing system might give rise to alternative accounting methods based on computations of public welfare rather than individual utility. Success in any of these areas could spill over into other areas of society, while failure would encourage rethinking and exploring of alternative routes. What started as a mere bridgehead could gradually expand into a broad creordering of society at large.

Can this thought experiment be translated into praxis? Perhaps – but only if we are able to conceive, develop and implement it in conjunction with ongoing empirical and theoretical research.

There are three related reasons for this requirement. One is that the changes outlined above constitute a direct assault on the capitalist mode of power: to democratize housing is to undermine the concentration of private real-estate ownership and management; to withdraw pension funds from the stock market is to arrest asset-price inflation and deprive capitalists of the nearly total leverage they have over middle-class incomes and the middle-class way of life; to demonstrate the efficacy of self-management in more and more realms of society is to delegitimize the sanctity of private enterprise and sound the death knell for accumulation.

So dominant capital and its power belt of government officials, economists and public-opinion makers are bound to fight this process nail and tooth. They will dismiss its underpinnings and attack its supporters. They will thwart its planning and sabotage its implementation. They will use sticks and carrots, brainwashing and threats, persuasion and violence. There is no way for us to withstand, resist and overcome these attacks without understanding – in general and in detail – the power logic they obey and the power structures they mobilize. And that understanding requires relentless, in-depth research.

Another reason is that even if we succeed and see our bridgehead gaining traction and spreading into other areas of society, initially these areas will have to coexist and interact with parallel structures of capitalist power. To put this parallelism in context, note that the modern capitalist principles of investment and accounting, discounting and finance and wage labour and increasing efficiency emerged in the early part of the second millennium AD, but that until very recently – perhaps as late as the nineteenth century – they operated within and alongside the logic of feudalism. And if that proves to be the case with post-capitalist alternatives, our praxis will depend crucially on understanding the ever-changing dynamics of capitalist power in which these alternatives exist.

Last but not least, enfolding research with praxis could boost the morale and optimism of progressive groups around the world. To show that democratic schemes such as pension-supported housing can actually work – i.e., that they serve the autonomy and wellbeing of their members while weakening the power logic of capital – is to demonstrate that we understand capitalism and can do better; that alternatives to capitalism can be imagined, planned and implemented.

This understanding, however, is difficult if not impossible to gain when we embrace academic dogma, cling to outdated political slogans and shun empirical research. The only way to achieve it – certainly on any meaningful scale – is through a series of autonomous, non-academic research institutes that are informed by and cater to societal action. These are not mere sidekicks. In our complex world, they have become a prerequisite for effective praxis.

On this subject, you might want to read:

Blair Fix, 2017, ‘Energy and Institution Size‘.

Bichler & Nitzan, 2020, ‘Growing Through Sabotage: Energizing Hierarchical Power‘.

***

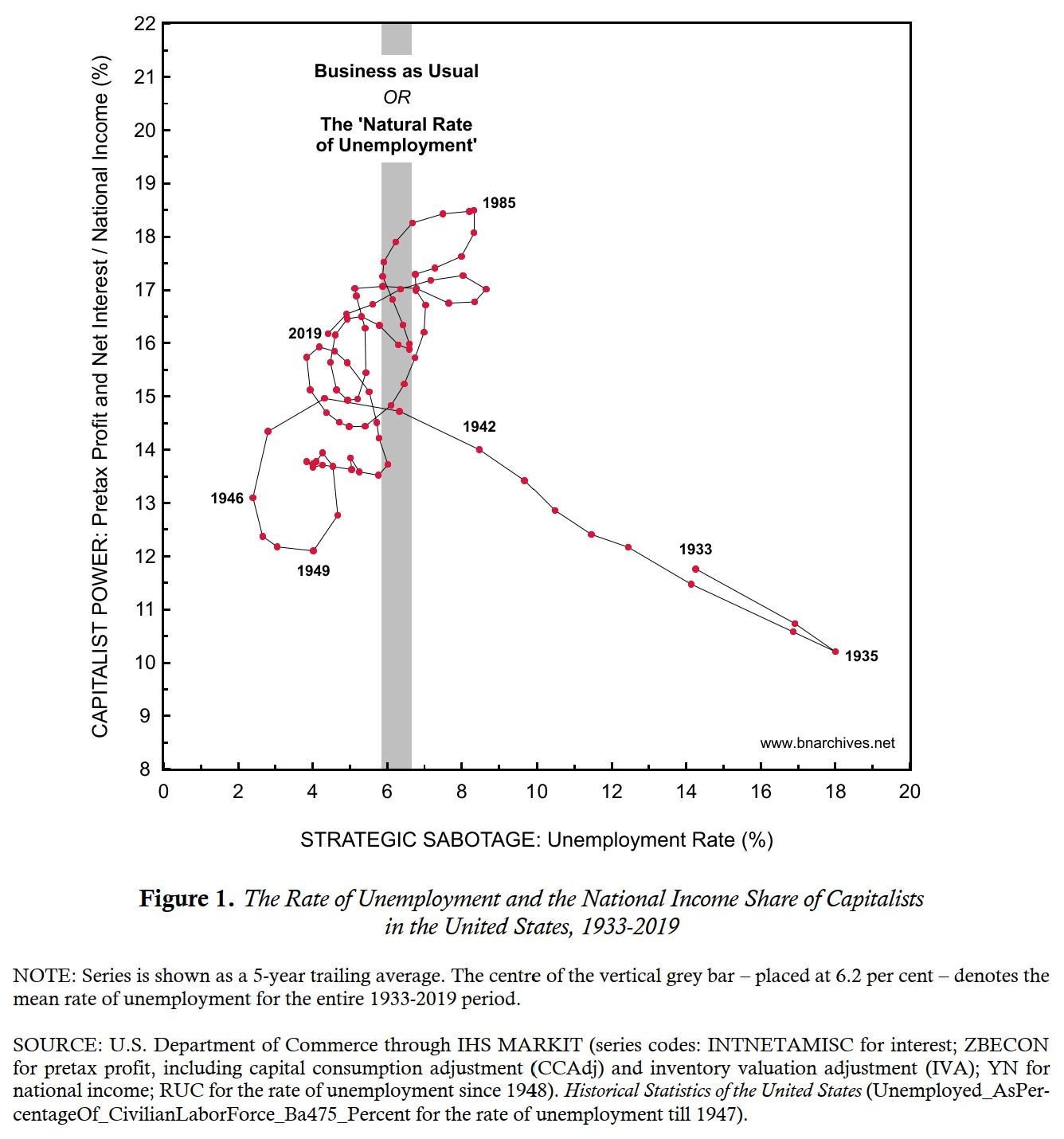

The chart below, taken from our recent paper ‘The Limits of Capitalized Power. A 2020 U.S. Update‘, suggests that U.S. capitalists require not absolute, but strategic sabotage: not too cold, not too warm.

Like with Goldilocks, too much sabotage reduces their earnings share, but so does too little sabotage. The optimal level of sabotage — otherwise known as ‘business as usual’ — is what economists call the ‘natural rate of unemployment’.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

How much difference do you think the ongoing economic reorganization toward already dominant, quarantine-readied businesses like Amazon, Walmart, etc. during the current health crisis will make for this regression trend?

It’s hard to tell. On the dominant capital side, some online firms have seen their EBIT rise significantly in 2020, but others have suffered. With smaller firms, if the carnage decimated mostly those at the very bottom of the distribution, the effect would be to increase the average EBIT. On balance, then, it’s hard to guess the direction differential EBIT took in 2019-2020.

[D]oes this annual rate of change graph look about the same if viewed with the top 50 firms rather than 200? What about the top 10?

Don’t know, we haven’t done the empirical work using different thresholds.

Is this tendency for the annual rate of change to regress the CasP version of Marx’s tendency for the rate of profit to fall?

Interesting question. Marx proposed that, over the long run, the organic composition of capital tends to rise faster than the rate of exploitation, and that this differential implied that, over the long run, the rate of profit will tend to fall. In our CasP case here, the downward tendency comes from the growing difficulty of keeping the pace of corporate amalgamation in particular and the growth of power in general.

The difference is threefold.

1. To demonstrate Marx’s tendency of the rate of profit to fall requires leaps of faith, particularly in defining the “proper” rate of profit. In CasP, the measurement of differential earnings and differential capitalization is relatively straightforward.

2. The reason for the downward tendencies is different. In Marx, it is inherent, in CasP it depends on the dynamics of power.

3. Marx’s claims have been researched for over a century. CasP work is in its infancy.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

December 30, 2020 at 11:37 am in reply to: Control over skill realization: A response to Fix in RWER (2019) #245166There is plenty of research on institutionalized waste and inefficiency in capitalism, dating back to the early neo-Marxists and Veblen, among others.

Institutionalized waste and inefficiency are often seen as a ‘trick’ designed to create additional demand to ‘absorb’ the ever-growing surplus output generated by capitalism. They are presented as paradoxical, since the assumption (including of Veblen and the neo-Marxists) is that capitalists try to maximize profit, and that this maximization is generally presumed to require efficiency and abhor waste.

In CasP, the focus is not on maximum profit but differential profit, which often requires inefficiency and waste (and which can easily sustain both insofar as they are universal).

The tongue-in-cheek equation you refer to is written from the perspective of the individual manager (or rather the theorist of the individual manager), not the differential accumulators. And it seems nearly if not totally impossible to operationalize.

1. Do you know of any papers/books that analyse the crisis of 2007-08 through the lens of CasP?

Yes.

‘Systemic Fear, Modern Finance, and the Future of Capitalism’ (2010) http://bnarchives.yorku.ca/289/. This paper elicited a critique and reply here: http://bnarchives.yorku.ca/314/ and eventually led to our ‘CasP Model of the Stock Market’ below.

‘The Asymptotes of Power’ (2012) http://bnarchives.yorku.ca/336/

‘Can Capitalists Afford Recovery? Three Views on Economic Policy in Times of Crisis’ (2014) http://bnarchives.yorku.ca/414/

‘A CasP Model of the Stock Market’ (2016) http://bnarchives.yorku.ca/494/. Additional work on the subject by Hager and Baines: http://bnarchives.yorku.ca/599/ and McMahon: http://bnarchives.yorku.ca/643/

2. How would you go about assessing the power of organisations for which market cap data doesn’t exist

Unlisted assets, although having no observed market value, can be examined through estimates of sales, markups and profits. I’m not aware of CasP research on this subject.

3. [H]ow easy it is to do a CasP analysis when the powerful/controlling interest is a private entity (i.e. a private equity firm) who own a public company that is weak on paper with a low market cap?

When small assets are part of larger firms or conglomerates, they are hard to analyze independently – not only for CasP researchers, but for anyone. James McMahon grappled with this question in his 2015 PhD on the large entertainment conglomerates and their movie subsidiaries http://bnarchives.yorku.ca/463/.

- This reply was modified 5 years, 7 months ago by jmc.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

We just posted a new WPCASP, titled ‘The Limits of Capitalized Power: A 2020 Update’ http://bnarchives.yorku.ca/663/. The paper shows the significance of strategic sabotage for the distribution of income between capital and labour and between large and small firms. The purpose of strategic sabotage is to control production (among other things), so as to redistribute income and assets. If capitalists ‘liberated’ themselves from this process, how could they control it?

Reading suggestions:

- If you need the Full Monty, the place to start is our 2009 book: http://bnarchives.yorku.ca/259/

- A shorter up-to-date summary is offered in this botched interview: http://bnarchives.yorku.ca/640/

- A 2018 summary of CasP research — including the research of others — is given here: http://bnarchives.yorku.ca/536/

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

Labban asks: “Has capital accumulation been completely liberated from production? This seems to be the conclusion drawn from reading Nitzan and Bichler.”

Hmmm.

I have no idea where Labban concocts this claim from. It certainly doesn’t come from us, or from any CasP work I know of.

Our research reiterates, again and again, that capital is not about production, but about the control of production. But that doesn’t delink capital from production. Indeed, the very purpose of CasP research – our own as well as that of others — is to understand the ways in which capital creorders – or creates the order of – society, including its productive activity.

Now, given that capital is partly about the control of production, it is rather obvious – although not to Labban — that it cannot be ‘liberated’ from it.

But, then, maybe I misunderstand Labban’s misunderstanding….

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

You haven’t misinterpreted anything, Adam: qualitative research is as important as quantitative research, and facts always require theoretical interpretations — just as theory can rarely stand without empirical work.

Thanks for your posts Adam.

1.

Irrespective of your theoretical approach and whether you will be able to incorporate it in your PhD dissertation, empirical analysis is important. In many cases it’s essential. Without it, you often end up wandering in the dark, getting your cues from other blindfolded writers who in turn get theirs from other blindfolded experts. From my own experience, empirical analysis is important for the answers it gives, but more so for the questions it raises. It will likely change your research trajectory many times over, and in ways that cannot be achieved without it.

One of my former graduate students was once advised by a Marxist professor to not engaged in empirical work. Empirical work, the professor observed, can get you entangled (in other words, prove your Marxist theory wrong).

But what dogmatic adherents cannot risk, scientists must.

2.

I think that DT Cochrane has done some work on the triangle of differential accumulation, risk and activism. Perhaps he can contribute something to this exchange.

- This reply was modified 5 years, 7 months ago by Jonathan Nitzan.

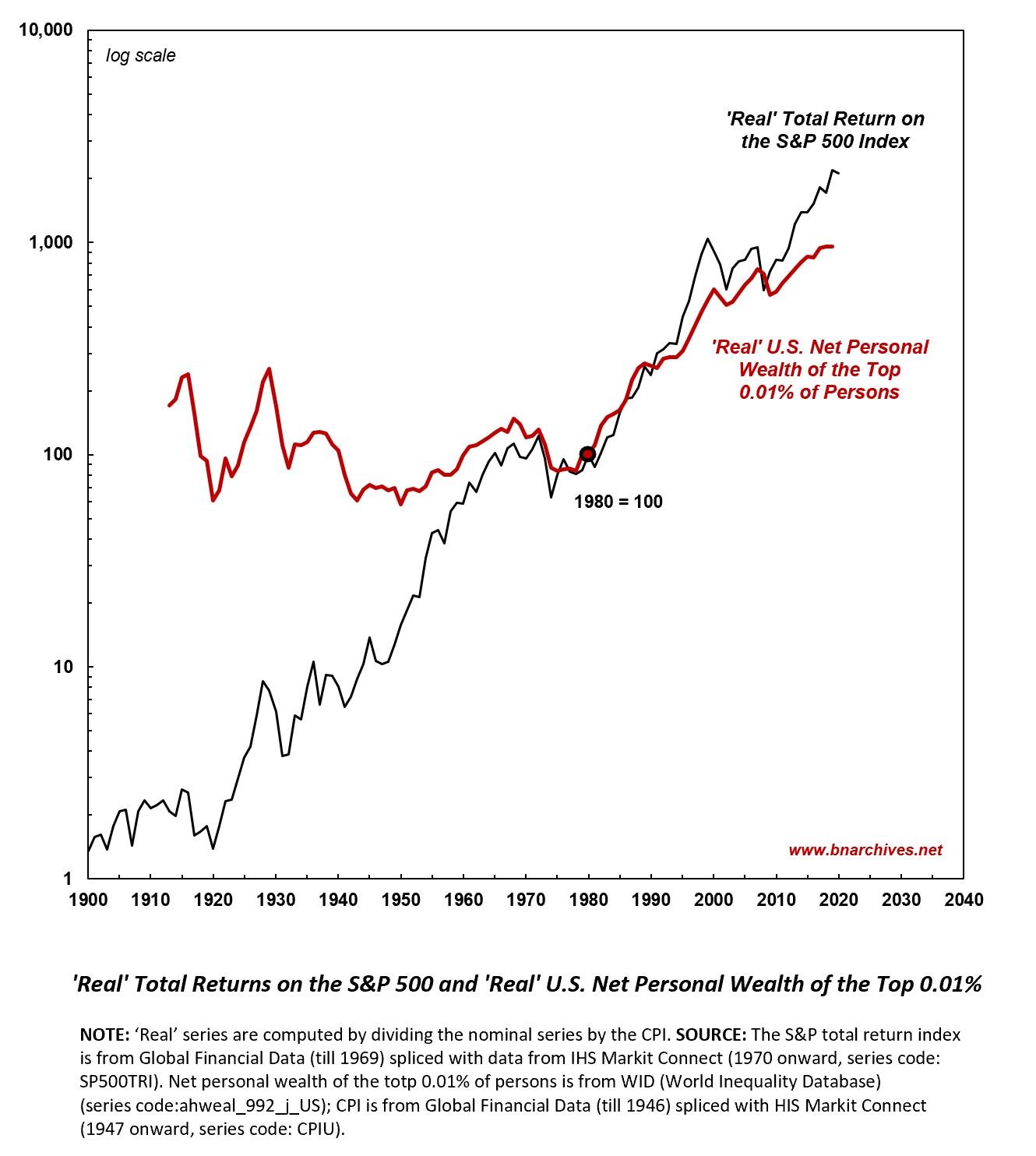

Nice chart. Here is my simplistic guess at what has happened since the 80s.

The causes you cite may affect the ‘real’ total return on the S&P 500. But how do they impact the correlation between the ‘real’ total return on the S&P 500 and the ‘real’ net assets of the top 0.01%?

The latter magnitude is determined by the portfolio of the top 0.01% and by the different ‘real’ returns on the various assets in that portfolio. As this portfolio changes, so will the correlation with the ‘real’ total return on the S&P 500. No?

Here is a comparison between the ‘real’ total return on the S&P 500 index (market value + reinvested dividends deflated by the U.S. CPI) and the ‘real’ net wealth of the top 0.01% of persons in the U.S. (also deflated by the CPI).

We can see that the two indices go pretty much together from 1980 onward, but that prior to 1980 their movement was cyclically similar by very different in trend.

I doubt that the reason for these variations is that, prior to 1980, the top 0.01 of persons did not reinvest their dividends in something.

A more likely reason, I think, has to do with the way in which the portfolio the top 0.01% has been reallocated over the years. For example, if a relatively small portion of this portfolio was in equities till 1980, and if that portion rose dramatically since 1980, we would expect the correlation between the two series to increase, as it has.

Of course, these are just guesses. The answer requires a much closer look a the data.

- This reply was modified 5 years, 8 months ago by Jonathan Nitzan.

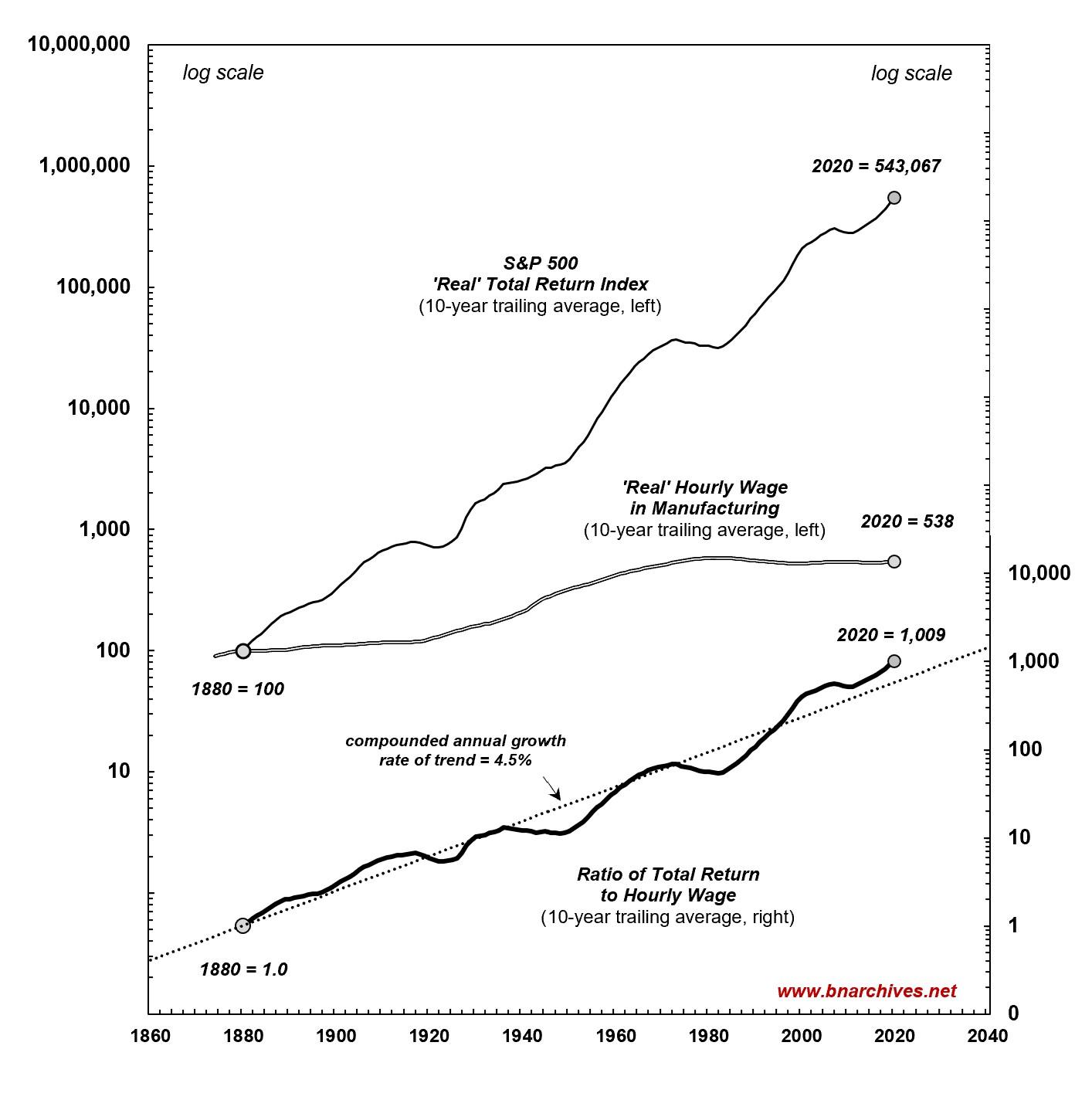

Neat, James!

Would be nice to see both charts combined + detailed footnotes on sources since the series are surely spliced many times over.

November 28, 2020 at 4:05 pm in reply to: Can Capitalists Continue to Squeeze the Income Share of Employees? #4562Thank you James.

The answer to the question of what drives these two opposite trajectories and how these drivers relate to strategic sabotage is not self evident. Hopefully, someone will think it worthy of investigating.

- This reply was modified 5 years, 8 months ago by Jonathan Nitzan.

Good questions, James.

Our figure simply suggests that the vast majority of the population — i.e., those depending on labour income, small business income and state handouts — have gained little, and since the early 1980s, nothing, from the stock market’s glory. The stock market tide doesn’t lift all boats. It lifts only a tiny fraction of them. So while the business of America is business, most of its population is not in that business.

But then, probability notwithstanding, roughly half the U.S. population are made to believe that they are going to be rich; i.e., that some day they will ride the upper series instead of the lower one. That hope makes them admire those who are already rich. And that admiration makes them susceptible to stock market glorification.

I don’t know if that suffices as an explanation, but it flows.

Over the past 140 years, the total return on U.S. equities (capital appreciation plus reinvested dividends) grew 1,009 times faster than the manufacturing wage rate. Since the 1980s, the increase was due entirely to the rising stock market. Hourly wages, measured in ‘constant’ dollars, moved sideways.

In the United States, celebrating the stock market is celebrating the victory of the capitalist mode of power. The underlying population — made mostly of wage earners, small business people and those who are unemployed or not in the labour force — rarely if ever contests this celebration. This silence suggests something about the future of this society.

- This reply was modified 5 years, 8 months ago by Jonathan Nitzan.

-

AuthorReplies