Forum Replies Created

-

AuthorReplies

-

May 24, 2021 at 8:17 am in reply to: Is the economics/politics duality Capitalism’s Noble Lie? #245689

Thank you Scot.

fiat money is not the issue, credit money is.

Yes, the issue is credit/debt money, but the system of credit/debt money cannot exist with commodity money. It needs fiat money – money by decree — as its denominator.

a commercial lender puts no existing capital or money at risk when it extends interest-bearing credit to a “borrower,”

I’m not sure I follow. Loans and the interest on them — including those made by commercial banks — are expected to be paid in the future. The fact that borrowers may not repay them makes these ‘extensions’ risky. This risk is mitigated by different forms of power, including government backing of the private banking system, but to say it does not exist seems to me odd given the nature and turbulent history of credit and banking more specifically. (Perhaps you mean that banks lend other people’s money rather than their ‘own capital’, but that fact makes them no less risky.)

credit money is what drives the need for the perpetual exponential growth of credit, money end economic growth, as well as “differential accumulation” more broadly

We’ll have to disagree on that. In my view, credit money is a facet of capitalization, not the other way around.

the discussion of “rituals” and “symbols” (and “COP-MOP” pairs) makes it more difficult to understand CasP and its value in providing a framework for describing Capitalism as a control system

Needless to say, you are welcome to offer easier-to-understand explanations!

- This reply was modified 5 years, 2 months ago by Jonathan Nitzan.

May 22, 2021 at 6:17 pm in reply to: Is the economics/politics duality Capitalism’s Noble Lie? #245683[…] it is the delegation of the sovereign power of money to private parties that is the ultimate source of capital’s power, e.g., […] it is private control over money, wages and prices that gives rise to the “depth regime” of sabotage.

Thank you Scot for the clarification.

I think there is a certain tautology to your argument. You say, and I paraphrase a bit, that the privatization of money is an important if not the ultimate source of capital’s power. You can similarly say that the private control of pharmaceuticals, energy, transportation, entertainment, construction, agriculture, biotechnology, education, advertisement, religion and what not are also sources of capital’s power.

According to CasP, capital is private by definition, so for something to become capital, it must first be privately owned.

Regarding the argument that the privatization of money creation is the ‘source’ of capital’s power.

(1) I think the issuance of money is never entirely private; like all forms of private power, it too is always backed by and intertwined with some form of governmental agency. Without this fusion, private money is bound to collapse (think of the early princely bonds issued by medieval rulers to private investors, or speculate what will happen to the U.S. private banking system without government oversight and backup).

(2) Conceptually and ontological, fiat money is based on forward-looking credit: i.e., the capitalization of risk-adjusted expected future returns. To get the process of money creation going, private banks have to issue loans, and these loans are nothing but capitalized profit expectations. In this sense, the modern system of money is a derivative of capitalization, not its cause. And if this argument is correct, the privatization of money cannot be thought of as the ‘source’ of capital’s power.

(3) More generally, in our opinion (Shimshon’s and mine), power has no single ‘source’, or ’cause’, let alone an ultimate one. In modern times — say since 1600 — power is considered a quantified relationship between entities. In society, these quantified relationships are creordered by human beings and organizations through various hierarchies of sabotage and resistance. Increasingly, these powers appear as as differential relations of capitalization/credit (including the institution of fiat money), but this appearance is not a cause, at least not in our opinion. It is merely the ‘operational symbol’, in Ulf Martin’s language, the quantified ritual with which modern capitalism expresses and negotiates its various hierarchies. At any given time, these symbols serve restrict and condition the boundaries of the possible, but they are also incredibly flexible, so that, over time, they can accommodate ever new forms of hierarchical power.

- This reply was modified 5 years, 2 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 2 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 2 months ago by Jonathan Nitzan.

May 22, 2021 at 12:10 pm in reply to: Is the economics/politics duality Capitalism’s Noble Lie? #245680From this perspective, the outright rejection of these foundational false dualities prevents CasP from fully understanding the source and nature of capital’s power

I’m not sure I understand your claim. Perhaps you can use the following example to illustrate it.

In our work, we suggested that, during the second half of the 20th century, the Weapondollar-Petrodollar Coalition supported Middle-East Energy Conflicts to boost its differential accumulation-read-power (for example, ‘New Imperialism or New Capitalism?’ 2006, http://bnarchives.yorku.ca/203/).

Do you think that ignoring the presumable politics-economics duality here prevented us from understanding the power of this coalition?

***

To clarify, we do not ‘reject’ the politics-economics duality. As we reiterate in our work, this duality is inherent in the way capitalism is framed virtually by all observes (except CasPers, maybe). Instead, we argue that, when it comes to the actual processes of accumulation, this duality has no operational meaning in the sense that capital discounts all forms of power, regardless of the specific rubrics they are hashed into.

- This reply was modified 5 years, 2 months ago by Jonathan Nitzan.

Some thoughts.

1. “The” market is vague enough to pin down, so it is hard to decide whether it “exists” or not. Conceived as the overall system of pecuniary exchange, I think we can say it exists. The thing is that there is no agreement on the precise nature of this system, and it is this lack of agreement that makes the question of whether “the” market exists or not difficult to answer.

2. “A” market is less vague. Economists usually define any given market by (1) the commodity in question, (2) the geographical scope and (3) the time frame. Of course, here too there are ample disagreements — first on the boundaries of these three items, and second and more broadly on the institutions that underpin them. Ask economists to define the “market for computer chips”, “automobiles” or “health services” and you get more answers that you wish to consider and no clear way to decide which of them is “valid.”

3. I think that in capitalism, the only safe way to use the term “market” is in reference to pecuniary exchange. For example, we can say that “we live in a market society” (i.e. a society dominated by pecuniary exchange), or that there is a “market for cars” (a physical/virtual space where cars are traded for money). But the specific character of this pecuniary exchange is open-ended, both ontologically and epistemologically.

I’m sure more words can be spilled on this subject, but I’ll stop here.

Thank you for the interesting reply, Scot.

1. Bridges would be very nice, provided they are not forced or impossible. In general, we find CasP bridges difficult to build since, in certain important respects, CasP is incommensurable with conventional political economy. (See ‘Unbridgeable’, 2021, http://bnarchives.yorku.ca/681/.)

2. You disagree with our claim that all commodities are ‘creatures of the social imagination’, writing that ‘Wheat is wheat. Steel is steel. Labor is labor. Etc.’ But wheat, steel and labor are not commodities. They are mere objects. They become commodities only when they are priced. As an object, a ‘ton of steel’ is qualitatively different from a ‘common stock of Tesla’. As commodities, though, they are qualitatively identical and differ only in price. From a CasP viewpoint, this latter universality — the fact that both can be quantified in dollars — is a creature of the social imagination.

3. You suggest that ‘the Market’ does not exist. Perhaps, but to assess this claim we must first agree on what ‘the Market’ is.

I think Polanyi is correct in saying that the idea and institutions of the so-called “self-regulating market” were enforced on society rather than emerged from it organically.

But in one crucial respect, Polanyi’s view is still completely different than if not totally opposed to CasP.

Polanyi claims that the politics-economics duality is both real and false. And yet, when it comes to capital, he accepts it fully. Like all other political economists, capital for him is an ‘economic’ entity. His Great Transformation is concerned almost solely with the emergence of capitalism. It offers no alternative concept of capital. In fact, it does not deal with this concept at all. He accepts the triple economic division of industrial-commercial-financial capital, and he goes on to argue that humans, land and money are ‘fictitious’ commodities – implying that other commodities are not.

In CasP, there is no division between industrial, commercial and financial capital: all capital is finance and only finance. Moreover, all commodities – i.e. all priced items — are creatures of the social imagination. Lastly and most importantly, capital is the commodification of power writ large, and therefore transcends the politics-economy duality to start with.

I should also mention that Polanyi’s notion/critique of the ‘self-regulating market’ — which he shares with many other heterodox thinkers — is also very different than CasP’s. The following section is from our Capital as Power (2009: 306-7):

The power role of the market cannot be overemphasized – particularly since, as we have seen throughout the book, most observers deny it and many invert it altogether. Analytically, the inversion proceeds in three simple steps. It begins by defining the market as a voluntary, self-regulating mechanism. It continues by observing that such a mechanism leaves no room for the imposition of power. And it ends by concluding that power and market must be antithetical, and that they can coexist only insofar as the former ‘manipulates’ and ‘distorts’ the latter.

An example of this inversion is Fernand Braudel’s historical work Civilization & Capitalism (1985). According to Braudel, capitalism negates the market. In his words, there is a conflict between a self-regulating ‘market economy’ on the one hand, and an anti-market ‘capitalist’ zone where social hierarchies ‘manipulate exchange to their advantage’ on the other (Braudel 1977; 1985, Vol. 1: 23–24 and Vol. 2: 229–30). A similar sentiment is expressed by Cornelius Castoriadis, when he proclaims that ‘where there is capitalism, there is no market; and where there is a market, there cannot be capitalism’ (1990: 227).

The root of the error here lies right at the assumptions. Capitalism cannot negate the market because it requires the market. Without a market, there can be no commodification, and without commodification there can be no capitalization, no accumulation and no capitalism. And the market can fulfil this role precisely because it is never self-regulating (and since it is never self-regulating, there is nothing to ‘manipulate’ or ‘distort’ in the first place). Price is not a utilitarian–productive quantity, but a power magnitude, and the market is the very institution through which this power is quantified. Without this market mediation of power, there can be no profit and, again, no capitalization, no accumulation and no capitalism.

And there’s more. The market doesn’t merely enable capitalist power, it totally transforms it. And it achieves this transformation by making the capitalist mega-machine modular. The blueprint of this new machine, unlike those of earlier models, is very short. Its essential component is the capitalization/accumulation formula. The formula is special in that it doesn’t specify what the mega-machine should look like. Instead, it stipulates a ‘generative order’, a fractal-like algorithm that allows capitalists to reconstruct and reshape their mega-machine in innumerable ways. The algorithm itself changes so slowly that it seems practically ‘fixed’ (the basic principle of capitalization hasn’t changed much over the past half-millennium). But the historical paths and outcomes generated by this algorithm are very much open-ended, and it is this latter flexibility that makes the capitalist creorder so dynamic.

- This reply was modified 5 years, 3 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 3 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 3 months ago by Jonathan Nitzan.

1. Interaction versus dissolution

In my work with Shimshon, we have argued that the ‘politics-economics’ duality, born from the early consternation of feudal power by the rising European burgs, has become a fetter on our understanding of capitalism.

This duality, which is imposed on, exists and accepted as a symbolic fixation at the lower levels of the social hierarchy, is lessened as we move up the scale until it disappears completely at the top levels of dominant capital. For the dominant capitalist-governmental rulers, the categories of ‘economics’ and ‘politics’ (or ‘society’ more generally) dissipate and are replaced by notion of differential power and the various forms of strategic sabotage that underpin it.

This perspective is quite different from Polanyi, for whom the issue is the interaction between the spheres, rather than their very dissolution.

2. Creorder

In CasP, the capitalist creorder — i.e., the ongoing creation of the capitalist order — is applied to the nature of capital. Capital, we argue, is not a productive economic entity but a symbolic financial ritual. It represents neither utility nor productivity, but the creording of differential power writ large.

It is true that many political economists, including Polanyi, have examined the effect of power on accumulation, whether negative or positive. But to the best of our knowledge, none (not even Veblen) have proposed — let alone theorized and researched — the notion that capital as such is a financial representation of power and nothing but power.

For more:

The Capital As Power Approach. An Invited-then-Rejected Interview with Shimshon Bichler and Jonathan Nitzan, 2020, http://bnarchives.yorku.ca/640/

CasP’s ‘Differential Accumulation’ versus Veblen’s ‘Differential Advantage’ (Revised and Expanded), 2019, http://bnarchives.yorku.ca/583/

- This reply was modified 5 years, 3 months ago by Jonathan Nitzan.

Reviewing Polanyi’s The Great Transformation, it struck me that many of his observations are consistent with and predict CasP

Polanyi is famous for arguing that people, land and money are ‘fictitious’ commodities, and that subjugating them to the ‘free market’ is bound to end in a backlash.

The idea that the economy ‘interacts’ with society is common to liberalism (through distortions) and Marxism (via the base/superstructure distinction). Can you explain how, in your view, it is consistent with/predictive of CasP?

- This reply was modified 5 years, 3 months ago by Jonathan Nitzan.

- This reply was modified 5 years, 3 months ago by Jonathan Nitzan.

From my brief glance I’m sort of surprised CASP doesnt appeared to have been reviewed much by some people in the field

For more on the relationship of mainstream and Marxist political economists to CasP, see “Manuscripts Don’t Burn” http://bnarchives.yorku.ca/641/, written to contextualize the rejection of our invited interview with Revue de la régulation: http://bnarchives.yorku.ca/640/.

I think what i consider the best ‘neo/classicals’ –the ones who did the theory—Arrow, Hahn, Samuelson, Mantel, Debreu, Sonnenschein..–i dont think either misunderstood or misrepresented the world anymore than anyone else before or after. I think they were quite clear that they were making an ideal model which did not apply to the real world . They just understood their model and made no claims about the real world.

Many neoclassical economists hide behind this Teflon veil: it’s ‘just math’.

The high and low priests who engage in this type of ‘just math’ call themselves economists, not ‘mathematicians’. And I think it is wrong to say that they do not intend their models to apply to the real world. They don’t speak about abstract X, Y and Z entities, but about social concepts such as rational agents, markets, utility maximization, productivity, growth, income, etc (as well as the ‘distortion’ that upset these pristine social concepts). They also tend to be highly biased in favour of capitalist ideology, both in terms of the questions they ask and the answers they give. Last but not least, they never turn down a Nobel Economics prize, least of all on the grounds that they are ‘not economists’ and that their theories are not about the ‘economy’.

So when economists assume ‘perfect information’, I think they are convinced that this concept represents how the world works or at least should work, and that it should be the basis on which economists could, at some point, be able to understand it. In doing so, they mislead themselves and their followers to never look at many of the things that actually mater in capitalists society. In my view, this is the main reason why they are heavily supported and often exclusively subsidized by corporations and governments.

I doubt that any of this can be said about theoretical physics, at least not in this harsh way.

For more on these issues, see our “Capital Accumulation: Fiction and Reality” http://bnarchives.yorku.ca/456/

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

Would profit exist in a world characterized by perfect, symmetrical information?

Let’s assume that: (1) profit is a manifestation of power; (2) power depends on the use/threat of (i) physical force and (ii) mental/emotional control; and (3) perfect, symmetrical information removes (ii). With these assumptions, profits will depend only on the use/threat of physical force and therefore will be greatly reduced.

However, a world of perfect, symmetrical information is a logical impossibility.

It is impossible because (1) if there is even a whiff of free-will, the future is unknowable; (2) “knowledge”, even of the past, depends, often greatly, on open-ended interpretation; (3) human beings do not have access to all facts, theories and interpretations — and even if they had such access, they don’t know how to tease “perfect” information out of it; (4), and crucially, even if in principle some human beings can have access to all facts, theories and interpretations, and even if they can objectively combine them, in practice, they can always block others from accessing such information, perfect or otherwise….

This is why neoclassicists assume perfect information: it enables them to misunderstand and misrepresent the world, perfectly.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

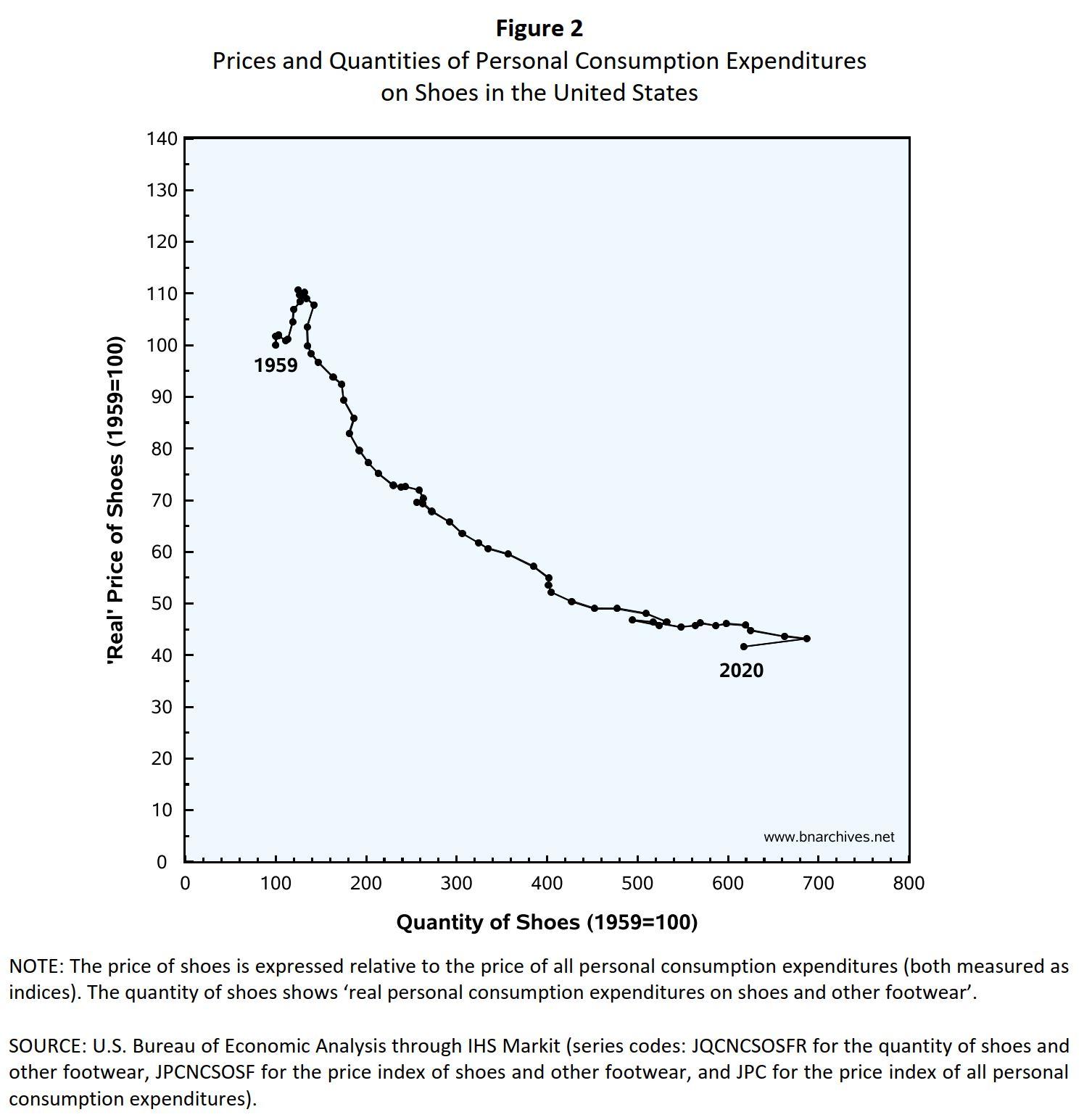

In my classes, both undergraduate and graduate, I present students with this empirical chart and ask them whether the time series in it represents supply, demand, both, or neither. Many students, like Professor Douglas, think that because the curve slopes downward it must be the demand curve, not realizing that their answer implies that none of the underlying parameters changed (or that they changed in a way that their different impacts exactly offset each other). They also don’t realize that whatever their answer, it can never be verified.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

This is a reply to our Working Paper by Alexander Douglas.

It is taken from his blog here: https://axdouglas.com/2021/03/17/defending-microeconomics/ and can also be found here: http://bnarchives.yorku.ca/679/

***

Defending Microeconomics?!

by Alexander X. Douglas

I was sent a link to this article by a colleague, who was concerned with the boldness of the central claim – that standard economic theory explains nothing about market behaviour. I thought I might as well share the outline of my response here.

I’m far from being a defender of the foundations of mainstream microeconomics. But this attack goes much too quickly, in my view. I find myself in the odd position of defending something I don’t believe in from an attack I think is unfair – indeed counterproductive.

Bichler and Nitzan attack the textbook explanation of prices and quantities as determined by an equilibrium between supply and demand.

Textbook economics represents market equilibrium, for a given commodity, as the intersection between a supply curve and a demand curve. Bichler and Nitzan notice that we never observe demand or supply curves. Of course not, because these represent counterfactuals: the maximum amount consumers would buy if the price were higher/lower, the minimum price firms would charge if the quantity purchased were higher/lower. The famous ‘scissors’ diagram in all the textbooks is not a picture of different states that a system could be in at different times; it’s a picture of a single moment in time, along with a bunch of counterfactuals for that same moment. As Joan Robinson said, time is at right angles to the diagram. So yes, of course supply and demand curves can’t be observed. We don’t observe counterfactuals; we only observe factuals, if I can say that. That is, we only see the price and quantity determined by the actual (factual?) market. So far what Bichler and Nitzan say is obviously true. How do they get from an obvious truth to a devastating critique?

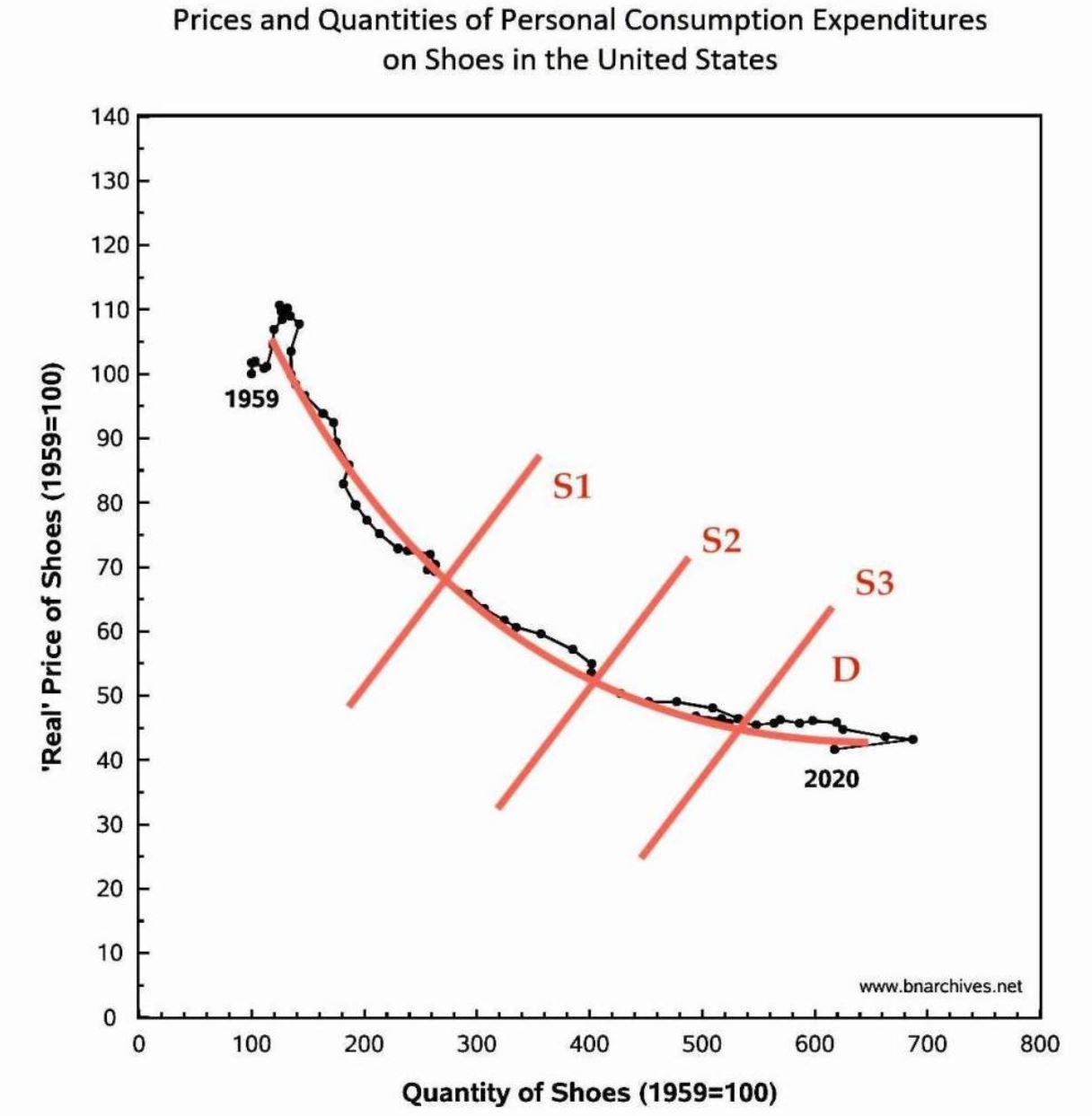

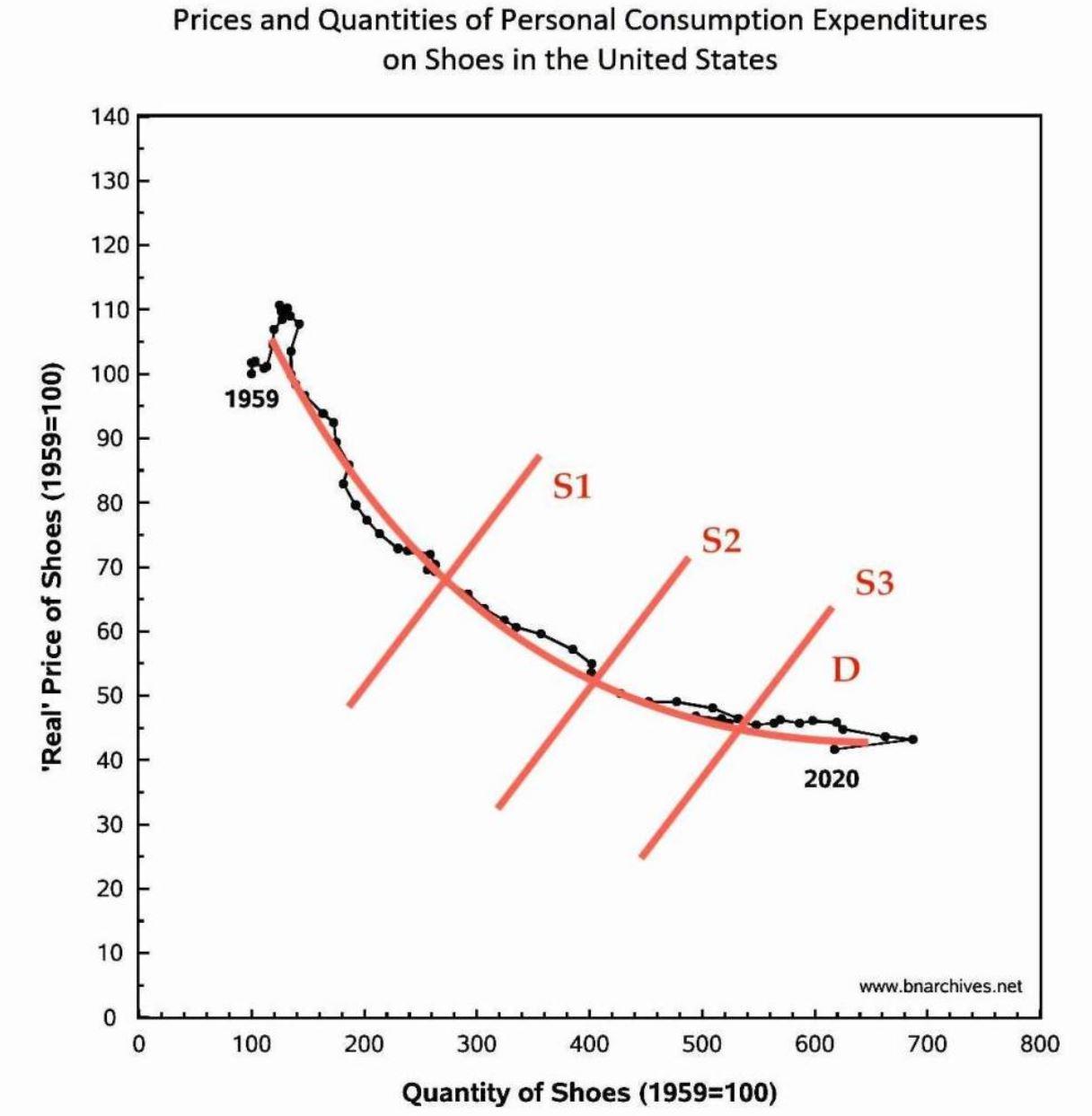

First, they look at a time-series of actual market data. Each point represents the quantity of shoes purchased in a given year (in the US) and the average price paid for a pair of shoes in that year:

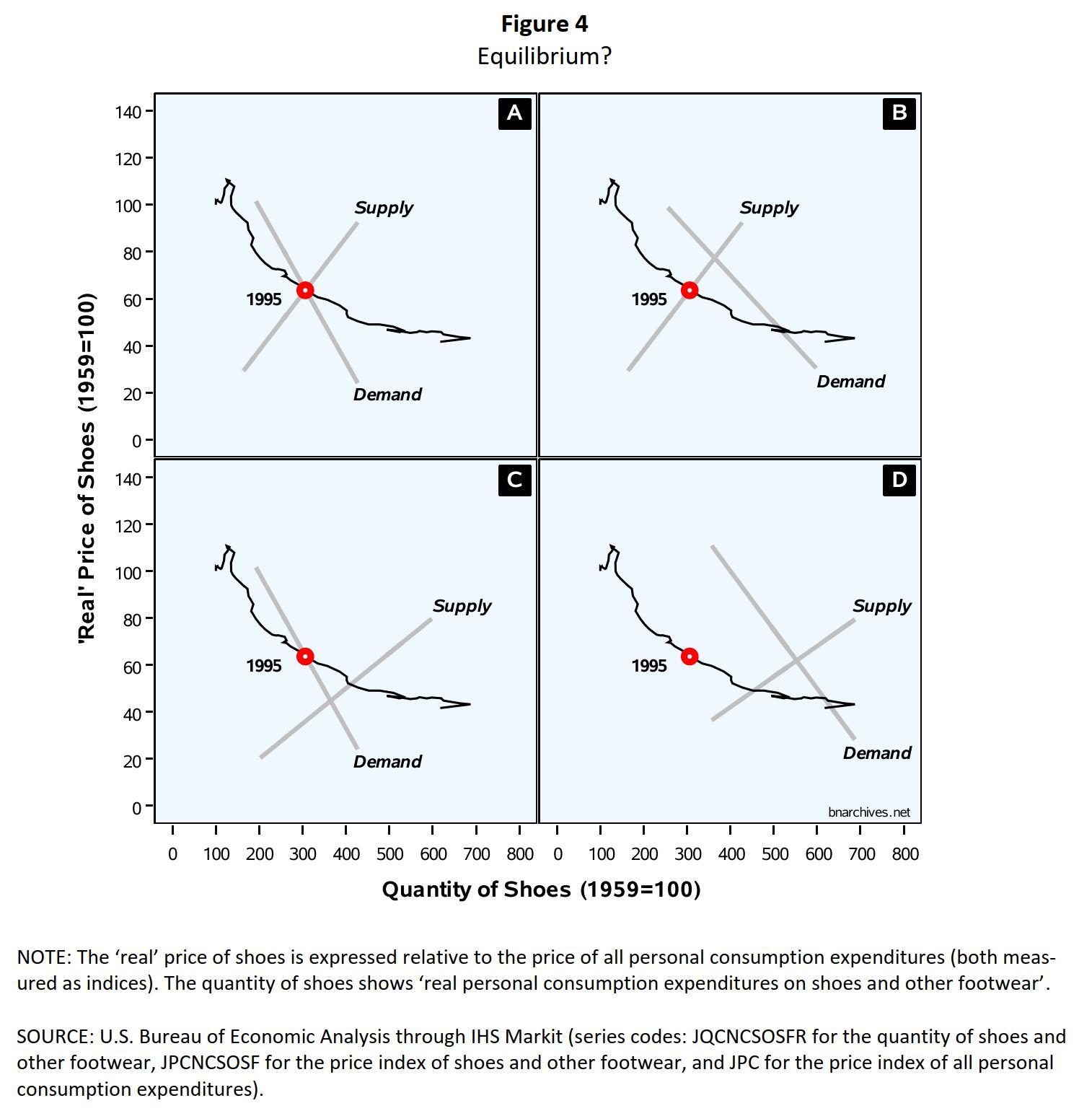

They then point out that this data is consistent with each point being a market equilibrium between a different supply and demand curve:

But it’s also consistent with each point being off the equilibrium in any number of ways:

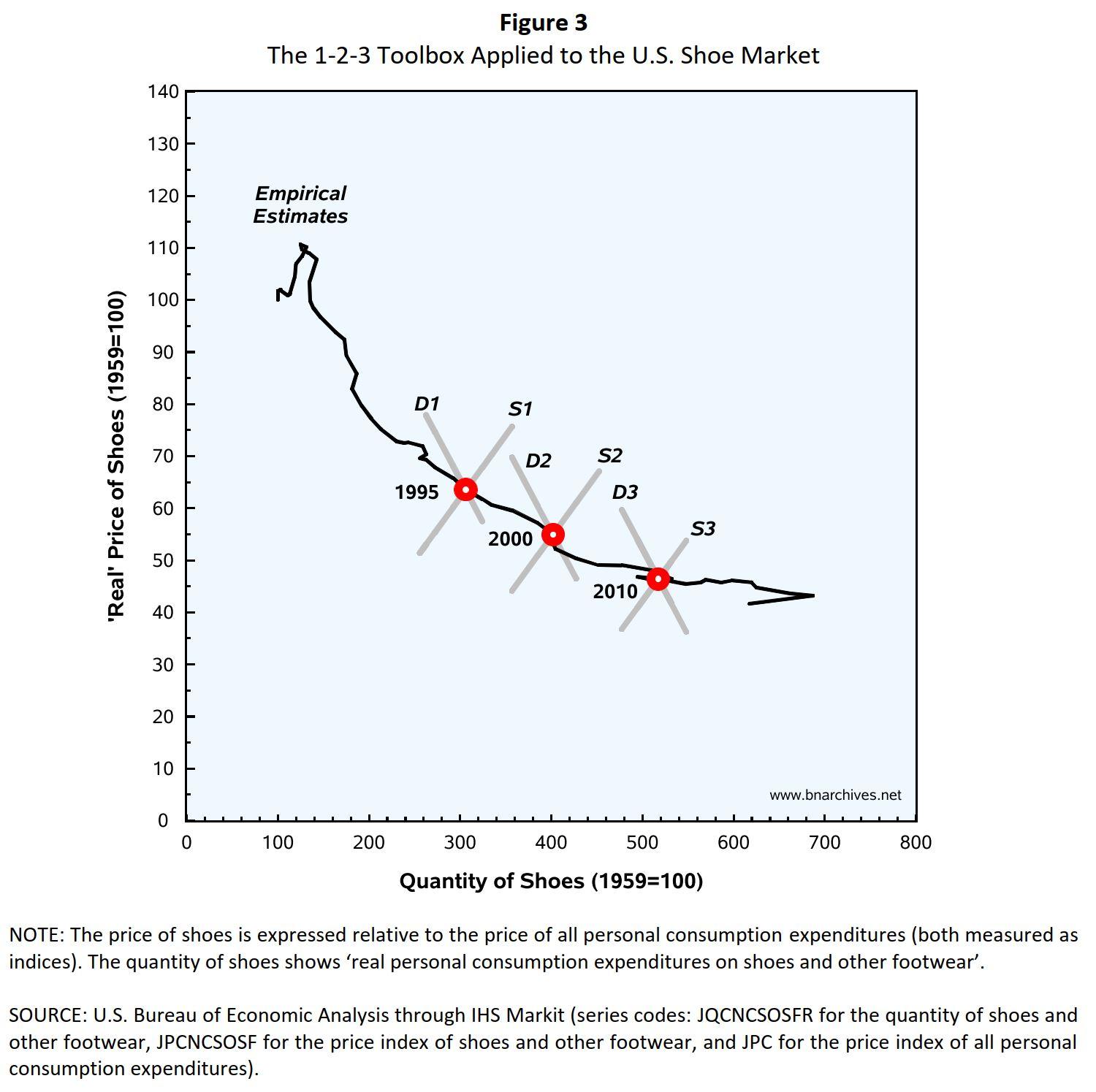

What does this prove? Not much, in my view. It’s hardly news that supply and demand curves can be drawn so as to intersect at any point you like. Since they can’t be observed, they must be constructed on the basis of assumptions. Bichler and Nitzan draw their curves arbitrarily, but they propose that neoclassical economists do the same:

But how did we know what these curves looked like and that they indeed equilibrated at those designated points?

The answer is we didn’t. Just like the neoclassicists, we have no idea what actual demand and supply curves look like. Just like the neoclassicists, we simply plotted them so that they intersected in the observations for 1995, 2000 and 2010. And like the neoclassicists, we did so because these intersections are consistent with the neoclassical doctrine.

But the “just like the neoclassicists” clauses here don’t seem right to me. The ‘neoclassicists’ would surely require some rationale for drawing supply and demand curves a certain way. The curves are counterfactual and unobservable, but they’re meant to represent plausible counterfactuals – plausible given certain assumptions. You can’t just draw them anywhere you like; you need a story about why you draw them where you do.

Now the shifting supply curves drawn by Bichler and Nitzan – S1, S2, S3 – make sense on standard neoclassical assumptions. The years seem roughly to move from left to right in this time-series. A standard assumption is that technology improves over time, and better technology means more efficient, lower-cost production. So this will constantly push the supply curve outwards.

But the shifting demand curves drawn by Bichler and Nitzan – D1, D2, D3 – seem entirely unmotivated. Of course demand changes. Tastes change; changes in income affect demand; changes in one market act unpredictably upon the conditions of all other markets; policy changes have their effects, etc. etc. But I can’t think of any reason the ‘neoclassicists’ would have for supposing a constant outward shift of the demand curve over time. On the contrary, I think the ‘textbook’ assumption would have stable demand – a single demand curve intersected by the outward-shifting supply curves. The curve might jump around a bit, but the jumps could be assumed to go in random directions and thus cancel out over a long period. Then you’d get this:

And this seems to show at least a part of the textbook theory being confirmed in the data. A crucial part of the standard theory is that demand curves slope downwards: as price falls, consumers want to purchase more. Of course here there’s some curve-fitting to make the demand curve match the data. But its basic shape can also be supported on ‘plausible’ assumptions: as markets get saturated, the demand elasticity decreases – thus the flattening out of the curve towards the east.

The above plotting of supply and demand curves isn’t purely arbitrary; it’s based on standard assumptions. So with those (textbook) assumption in place, we have a confirmation of the textbook theory. Nor are the curves simply plotted to match the data, as Bichler and Nitzan’s are; they are justifiable on standard assumptions.

It’s odd to me that Bichler and Nitzan present this data against the mainstream case. I must admit that the part of me that wants textbook microeconomics to fail was disappointed by how well this time-series actually bears out the textbook story. I was actually surprised to see that people really do seem, like the consumers in the textbooks, to buy more shoes as technology reduces the price.

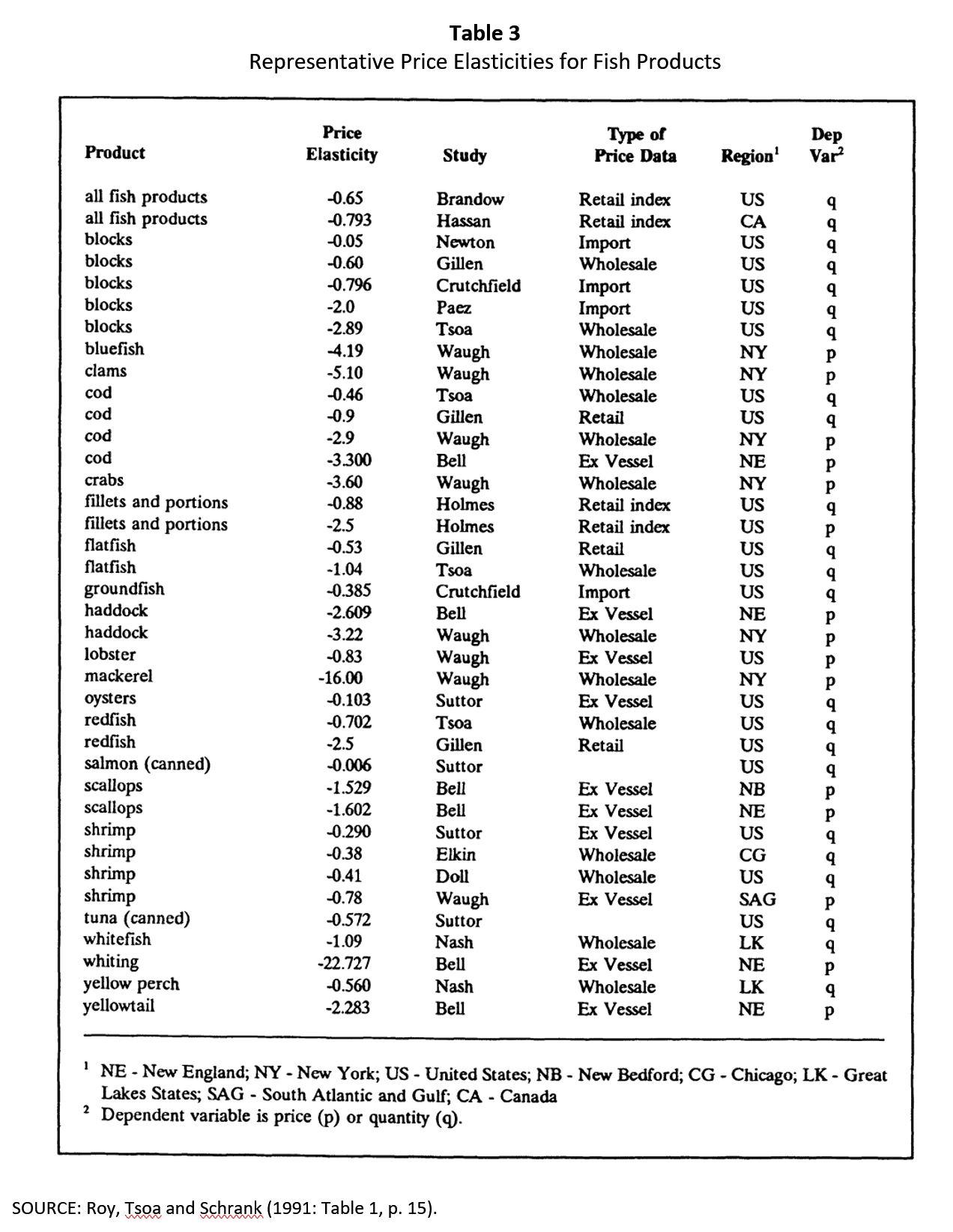

Bichler and Nitzan also cite data showing that the elasticity of demand for different goods varies widely:

This is another case where, aiming to undermine the textbook story, they manage to find data that confirms it! If we were judging the empirical confirmation of a specific economic model we could look at things like the demand elasticity it assumes and see whether this is confirmed in the data. But Bichler and Nitzan are judging textbook microeconomic theory in general. That theory says nothing at all about the specific slope or shape of demand curves. It states only that they slope downwards, and that is, apparently, confirmed in the data.Standard economic theory makes only very generic predictions – more specific ones need specific models. An example of a generic prediction is what appears to be confirmed in Bichler and Nitzan’s Figure 2: as the price falls, people buy more. Of course the data doesn’t confirm that prediction on its own. You need to assume a stable, downward-sloping demand curve. But Bichler and Nitzan inadvertently find empirical support for that also: they have a table that seems to show that, whatever shape the demand curve might have, it’s generally a downward-sloping one.

To repeat, my reservations about their critique don’t stem from a strong faith in the explanatory power of standard microeconomics. My worry is that the material their critique presents seems to be precisely the sort of thing a textbook might include as a defence of the theory. As a critique of textbook microeconomics, this might be a step backwards.

- This reply was modified 5 years, 4 months ago by Jonathan Nitzan.

March 1, 2021 at 10:04 pm in reply to: GameStop, hedge funds, and the “reality” of the stock market #245396Hi Jeremy:

1.

The percentage of pension ‘coverage’ per se does not tell us the $ size of pension assets saved by different groups.

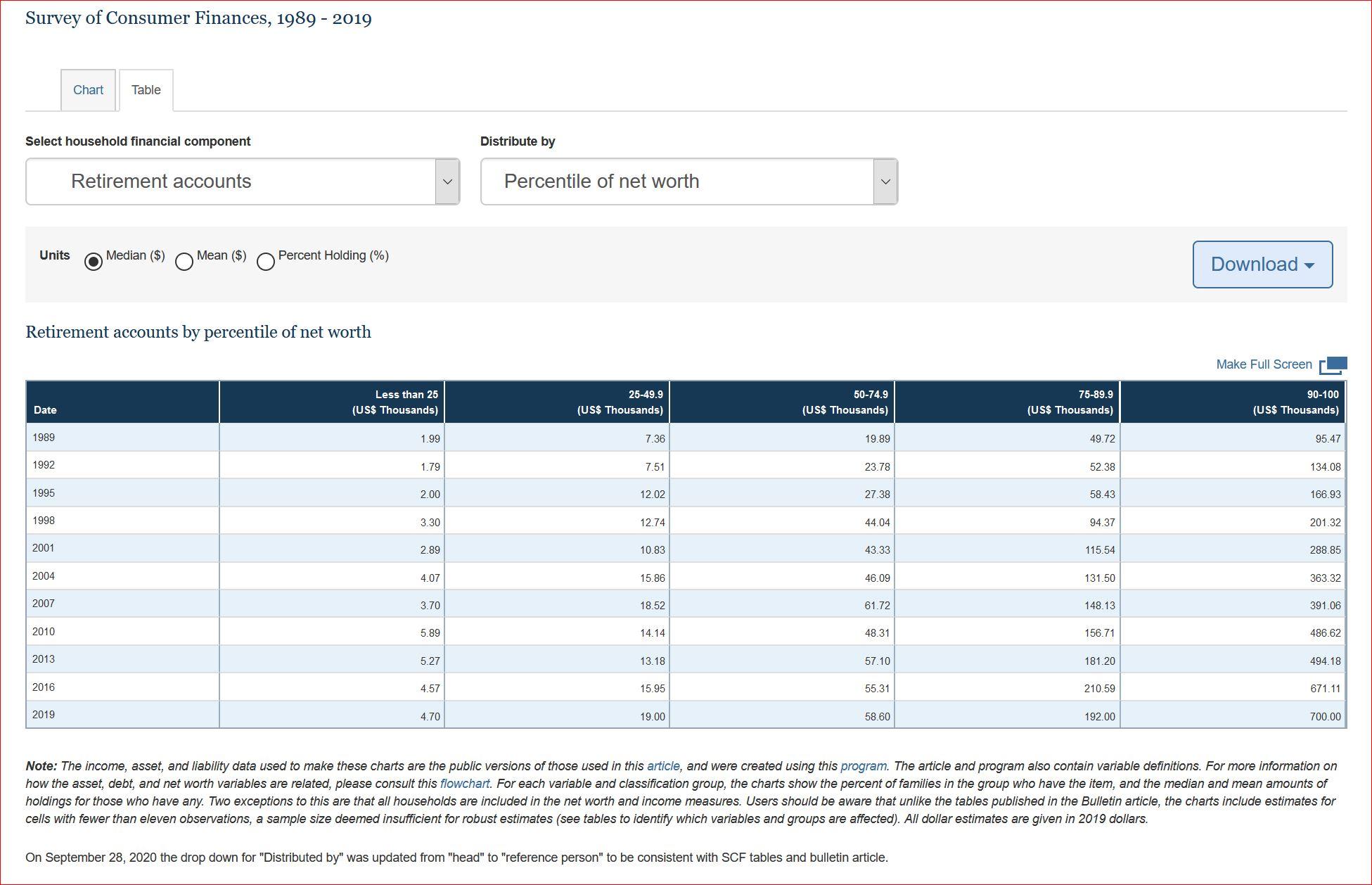

Here is a table from the U.S. Survey of Consumer Finance, showing the size of retirement accounts by percentile of net worth:

The table suggests that, in 2019, the bottom half of the population has very small retirement account saving: the poorest 25% of households have $4,700 per family, and the next 25% have $19,000 per family. The next 25% have more, but scarcely enough to retire. These savings have risen only marginally over the past 20 years.

2.

Regarding the use of higher returns to lure the underlying population away from the stock market. The vast majority of those who would join such a project are not “invested” in the stock market, certainly not in a meaningful way (you can verify it by looking at the tables offered by the Survey of Consumer Finance). And the attractiveness of the bridgehead program, I think, is not its differential rate of return, but the housing and retirement security it offers and the participation in shaping one’s own life.

- This reply was modified 5 years, 5 months ago by Jonathan Nitzan.

February 20, 2021 at 1:00 pm in reply to: Questions Regarding Mumford’s Theory of the Mega-Machine #245384Yes, we often project our social order onto the natural world. But we shouldn’t take this as far as the post modernists, and conclude that we can never understand the natural world because everything is clouded by ideology. Despite our tendency to delude ourselves, good science does happen.

At a risk of sounding simplistic, I’d say that human thinking requires categories; categories imply ‘likeness’; and metaphors are a major form of likeness: they compare and in some sense unite previously orthogonal domains.

Metaphors are everywhere in human thinking, and they pervade both organized religion and science.

One key difference between organized religion and science, is that organized religion worships its own inventions as if they are hetronomously given, while science is painfully aware that its frameworks and theories are its own Protagorean making.

In the monotheistic religions, God is literally the king of the universe, has to be obeyed by its inventors and their laity via his self-nominated earthy representatives, and remains in his position for millennia (or until the worshippers perish). In science, theories and even worldviews, no matter how entrenched, can succumb to counter evidence in a historical jiffy.

I think that as long as we remember that our metaphors are own inventions and don’t use them as externally given evidence, we remain scientists. When we start sanctifying our metaphors as heteronomous, we move over to the domain of organized religion.

- This reply was modified 5 years, 5 months ago by Jonathan Nitzan.

-

AuthorReplies