Forum Replies Created

-

AuthorReplies

-

February 6, 2022 at 8:50 pm in reply to: Capitalists: Incapacitating Industry or Allocating Resources? #247737

rk374:

It depends on what we mean by ‘industry’.

1. If we understand industry in the spirit of Veblen — say, as denoting the ‘reasoned application of knowledge, human effort and material resources for the betterment of human and planetary life’ — then industry cannot systematically undermine these goals while retaining a definition that says the very opposite…. In this sense, industry cannot be ‘unbridled’.

2. This claim, though, applies only at a very abstract level. In practice, humans disagree on (1) what constitutes the betterment of human and planetary life, and (2) how the application of knowledge, effort and resources affects human and planetary life. So at this practical level, industry can become ‘unbridled’ to a greater or lesser extent, even in a society committed to these goals.

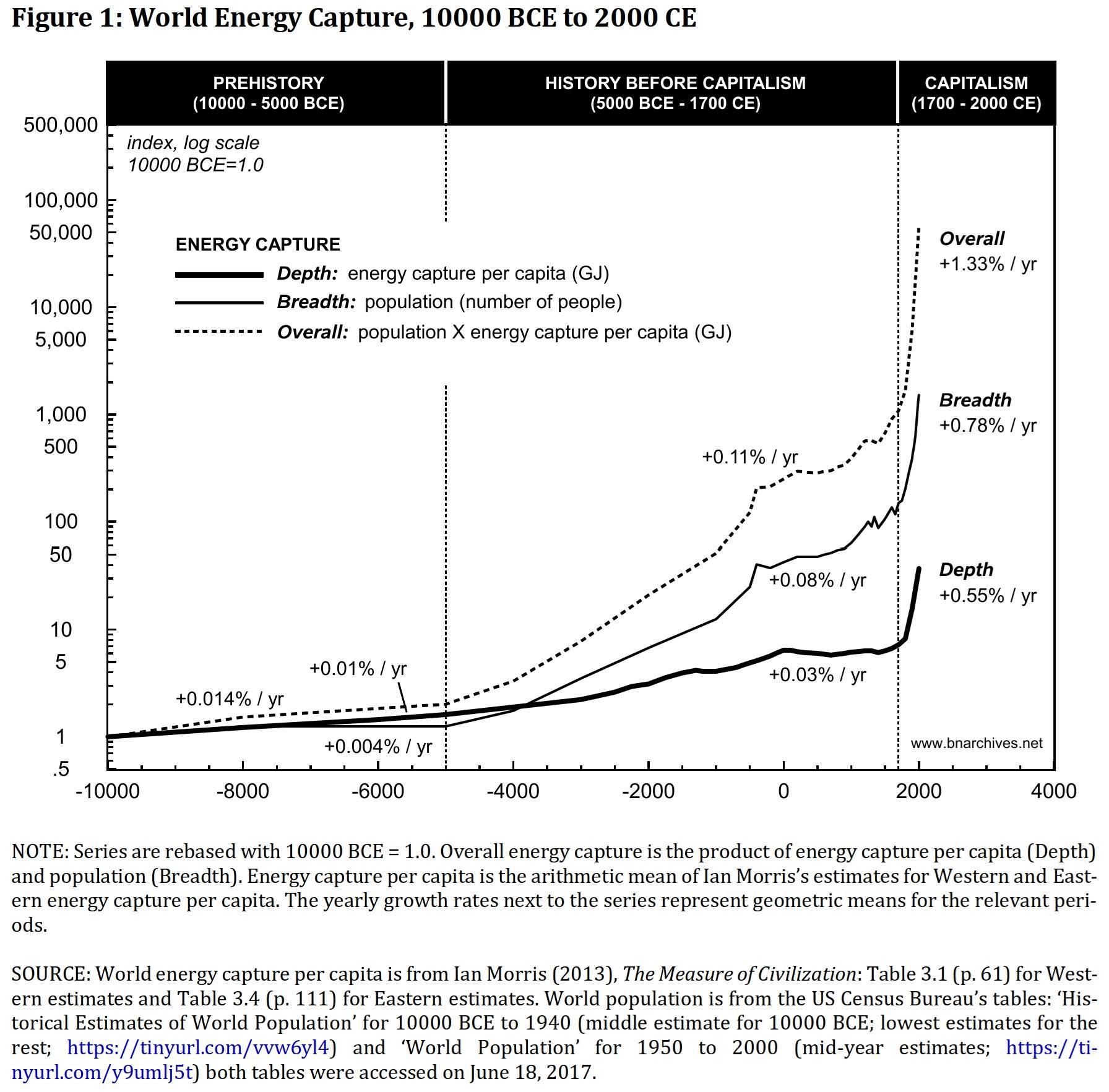

3. But we live in capitalism, and capitalism is driven by business not industry. Following Veblen and Mumford, our CasP theory argues that business undermines industry — i.e., it undermines the ‘reasoned application of knowledge, effort and resources for the betterment of human and planetary life’. But it does not undermine the use of knowledge, effort and resources as such. In fact, as the energy chart below shows, it augments it a great deal. The thing is that, in our view, this augmentation is not directed — at least not in the main — to the betterment of human and planetary life, but to the increase of hierarchical power which sabotages human and planetary life as most people now realize (though often without understanding why).

4. In this context, where a great chunk of our social and physical resources are used and abused for power ends, it follows that their prices don’t represent the ‘right’ or ‘proper’ allocation of resources for the good life of people and the planet (don’t know about ‘utility’, since nobody has ever observed and measured it).

February 1, 2022 at 2:58 pm in reply to: Does CasP Really Have a Theory of Value? Does It Need One? #247697Things became more regularized after 1623 and the rate of useful inventions creating new economic activities accelerated: eyeballing a list in wikipedia and counting what seem to be commercial (as opposed to scientific) inventions I see 1 invention in 16th cent 2nd half 2 inventions in 17th C 1st half 3 inventions in 17th C 2nd half 5 inventions in 18th C 1st half 11 inventions in 18th C 2nd half … and so on. This quickening of invention/entrepreneurship is the beginning of capitalism.

I’m not sure I understand you correctly, but you seem to equate capitalism with a positive rate of growth of invention / enterprise. I wonder how one actually determines such things. For example, should we include language, mathematics, the alphabet, ownership, writing, the wheel, medicine, kingship, marriage, etc. as “inventions” and “enterprise”? If we do include them as such, then we should say that capitalism existed whenever these entities emerged and changed — i.e. from the very beginning of humanity. And if don’t include them, then your definition of capitalism must be made more restrictive.

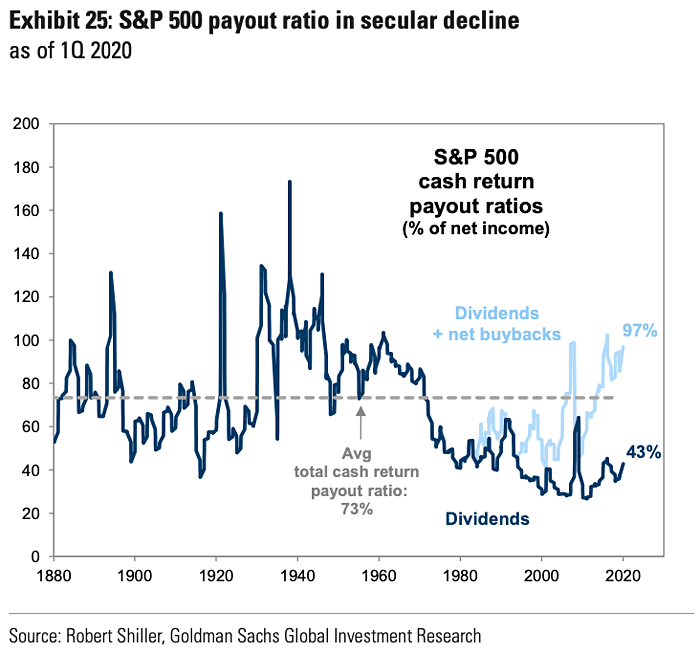

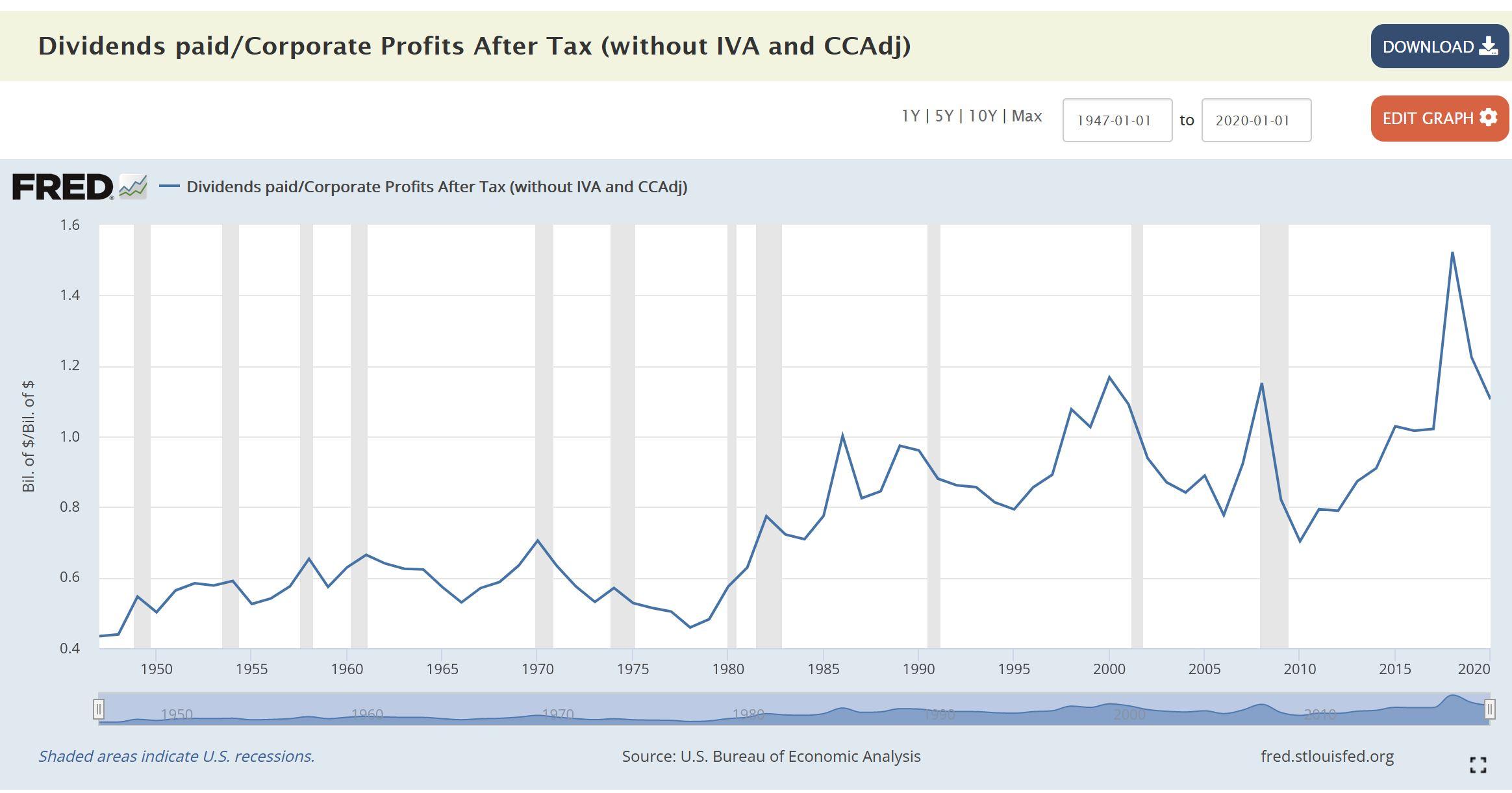

The ratio exceeds one because many corporations aren’t profitable.

Since the 1980s, the share of net profit in national income has trended upward, and a growing share of these profits has gone to dividends. Currently, dominant capital pays over 40% of its net profit in dividends (and another half in buybacks). It is true that a smaller number of firms pay dividends, but those who do seem to compensate for the shortfall.

But there are plenty of low-grade capitalists (individuals and firms) for whom differential accumulation (as compared to other capitalists) is neither a goal nor a concern, for example.

I’m not sure. I think all capitalists are gripped by benchmarks — the main difference is that most small capitalists are obsessed with meeting the average, whereas larger ones try to and sometimes can beat it.

Is this always the case? One of the reasons I believe Apple, Amazon, Google, and Microsoft have such large market caps is because they’ve managed to capitalize the future earnings of those outside of their corporate hierarchies.

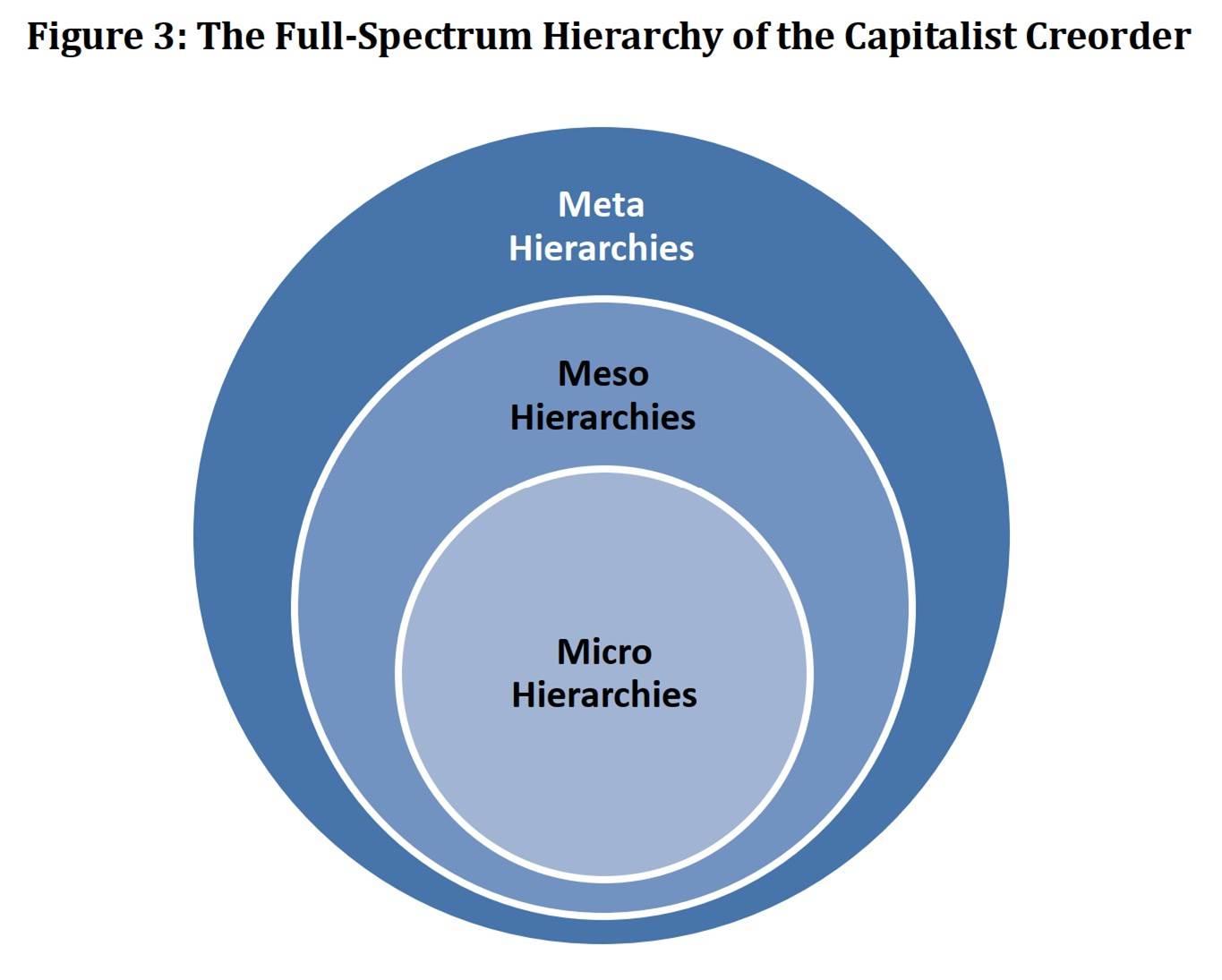

The inner hierarchies of the corporations themselves are only one aspect of hierarchical power, and not necessarily the most important one. In Section 3.3 of ‘Growing through Sabotage’ (2020), we classified corporations as micro hierarchies, nested in meso-hierarchies and further in meta-hierarchies. If we consider the full spectrum of social hierarchy, we might find that today’s capitalism is the most hierarchical society ever.

Most companies no longer pay dividends.

The data below are only marginally germane to the broader argument, but they are interesting nonetheless.

This chart is from Blair Fix: https://capitalaspower.com/2015/07/some-important-limitations-of-income-inequality-data/

Here is the U.S. dividend payout ratio. It has risen significantly since the 1980s, and at times it even exceeds 1!

Debate on the separation of ownership from control started in the 1930s with Berle and Means’ book on The Modern Corporation and Private Property, and it continues for two obvious reasons.

First, corporations are legally bounded, which means that even sole owners cannot do whatever they like with them. Second, the principal/agent structure of corporations inserts a layer of separation that further limits the flexibility of their formal owners, particularly if they don’t have a majority stake.

But this debate often misses the point, namely, that the overarching subject here is not the owners/executives/policymakers, but Capital itself.

In the final analysis, capitalism is not governed by individual capitalists, even though it often seems that way. It is not the Rockefellers, Carnegies, Morgans, Soroses, Zuckerbers and Musks of the world that run the show. And it is not even the corporations that they own that stir capitalism. Instead, it is the inner logic of capital that subjugates them all.

So why does CasP put so much emphasis on corporations — particularly the large ones — and on the dominant capitalists and executives that own and manage them?

The answer is that, according to CasP, the inner logic of capitalism is about differential power, and the imperative of differential power drives and creates taller and taller hierarchical structures headed by state-supported large corporations, their top executives and key owners.

By analyzing the various processes of sabotage that leading corporations/government officials/owners/executives engage in and the resistance they face on the one hand, and by contrasting these processes with their differential income, risk and assets on the other, we can draw meanigful conclusions on the changing nature of capital as power.

- This reply was modified 4 years, 5 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 5 months ago by Jonathan Nitzan.

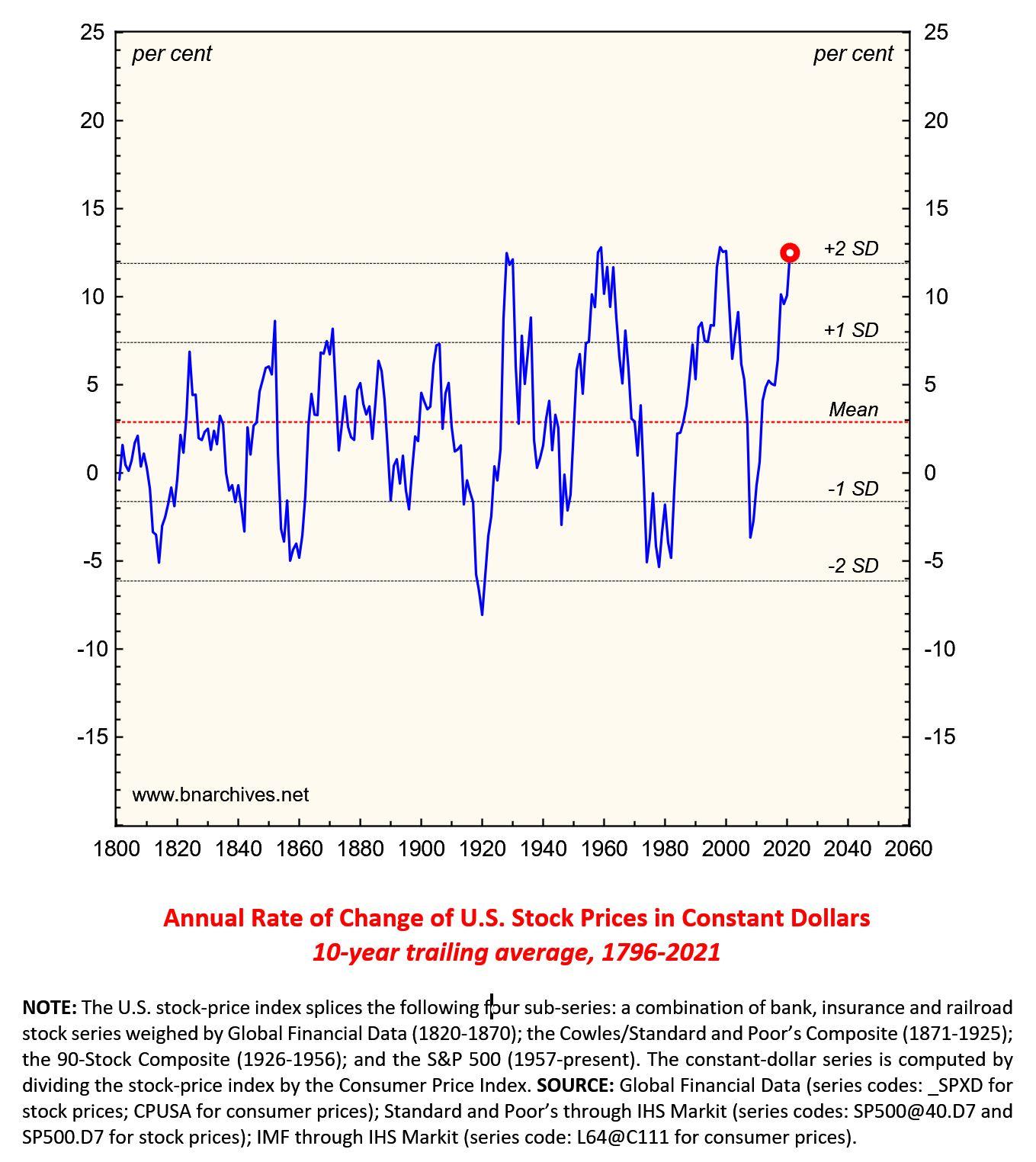

1. The series in this figure shows the annual rate of change of the CPI-deflated U.S. stock market index, expressed as a 10-year trailing average. These transformations mean that every annual observation in the series measures the average annual rate of change of the CPI-deflated index over the past 10 years.

2. The chart also marks one and two standard deviations above and below the historical mean of the series.

3. The current level of the series is more than two standard deviations above its historical mean.

4. If I were a betting man, I’d say that the U.S. is about to enter a major capitalist crisis sometime during the next decade.

- This reply was modified 4 years, 5 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 5 months ago by Jonathan Nitzan.

That’s impressive growth! I’m glad these ideas are circulating.

Yes, assuming that ‘downloads’ don’t mean ‘hits’ and that the items are read….

Thank you Scot.

First, I had always understood that the Fed’s love affair with monetarism died with Volcker’s failed monetarist experiment in the 1980s, that the Fed thereafter returned to targeting the Fed Funds Rate instead of trying to actively manage debt and monetary aggregates.

I think it is useful to distinguish monetarism from its policy instruments. Interest rates and the so-called money supply (an umbrella term that can mean many different things) are often used as policy instruments. They are also related, insofar as changing one alters the other, and vice versa. Central bankers and economists bicker constantly on the proper way to calibrate these slippery variables.

That being said, theoretically, most central bankers and mainstream economists agree that inflation is a monetary phenomenon in the sense that P = M * V / Q, and then argue endlessly on the meaning of each variable and how they lag each other in time. (When I came to work at the Bank Credit Analyst Research Group in the 1990s, I presented some of my PhD work on ‘Inflation as Restructuring’. One of the lead editors told me that although he found my argument fascinating, in the final analysis in didn’t matter: when all was said and done, inflation was all about the growth of money.)

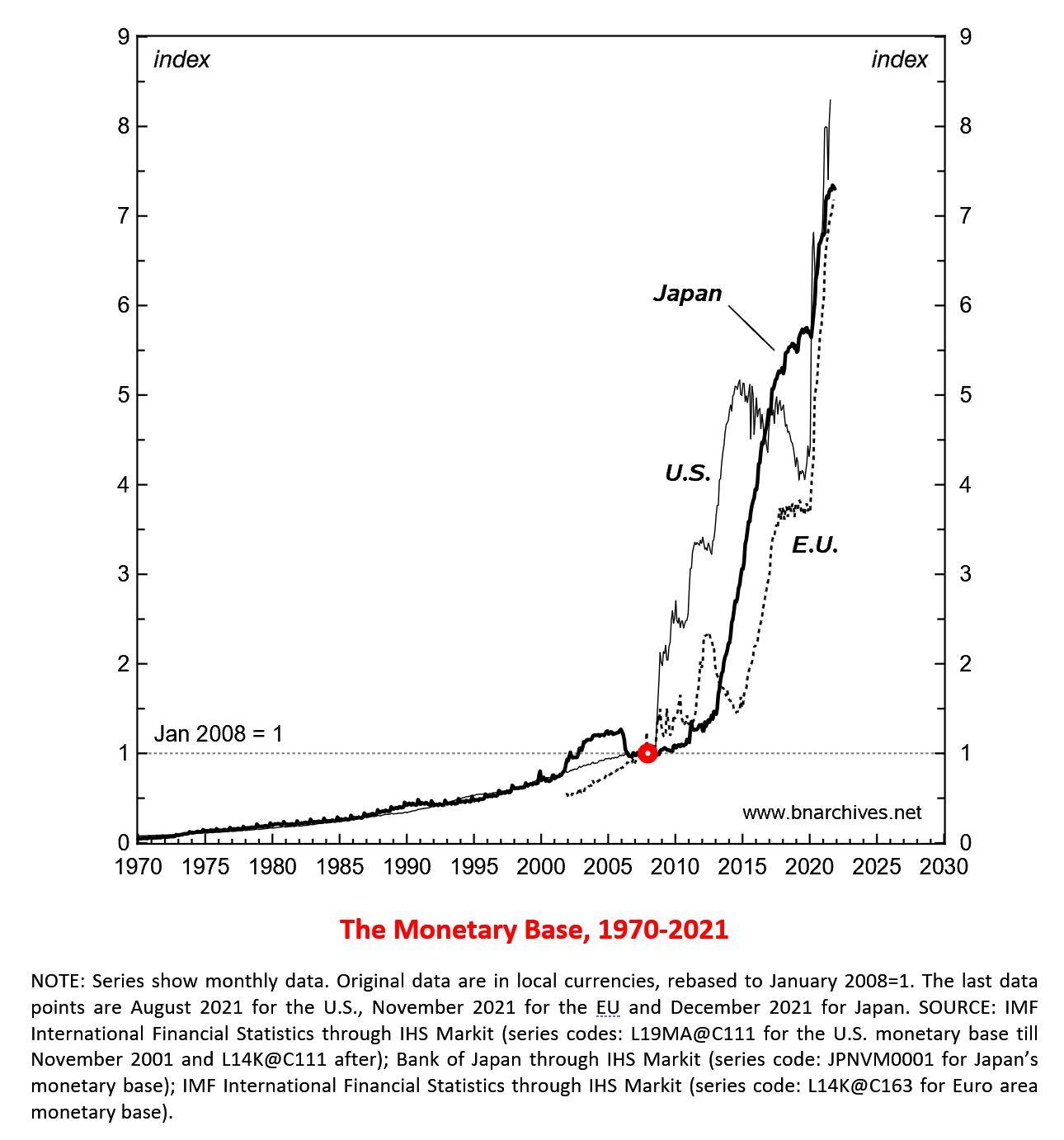

what the Fed publishes (and the IMF appears to use) as the US monetary base (the series BOGMBASE) is not “the overall value of notes and coins circulating in each country/area” but rather the “currency in circulation” plus “reserve balances,” which by definition do not circulate.

Yes, you are correct; my definition was inaccurate. But the distinction between currency in circulation and reserve balances is mostly a technical feature that facilitates settlements among private banks and between private banks and the central bank. The key thing is that the monetary base is the only money aggregate that central banks control directly. The other aggregates (M1, M2, etc.) are determined jointly with the private sector.

The end of monetarism

A note by Shimshon Bichler & Jonathan Nitzan

According to Milton Friedman, inflation is always and everywhere a monetary phenomenon of too much money chasing too few commodities. Following this logic, the Holy Grail of neoliberal policy is to have the so-called money supply expand just a bit faster than the long-term growth trend of the ‘real economy’. This way, the economy is given some flexibility — but not enough to stoke the monetarist fire of inflation.

And sure enough, as our chart shows, central bankers in the advanced capitalist economies — the U.S., Europe and Japan — adhered to the spirit of this policy up until the early 2000.

The chart plots the size of the ‘monetary base’ — namely, the overall value of notes and coins circulating in each country/area. This value is expressed in local currency and is rebased with January 2008 = 1 to enable temporal comparisons between the different series.

Until the beginning of the new millennium, the monetary base grew gradually and predictably, just as monetarism demanded. But in the early 2000s, the orthodoxy started to rattle. The first deviant was the Bank of Japan, whose ‘quantitative easing’ aimed — or so we were told — to fight the country’s persistent deflation. And then came the 2008 global financial crisis and all hell broke loose.

Having panicked, ‘policymakers’ started issuing high-power money as if there was no tomorrow. Initially, they justified their heresy by end-of-the-world scenarios of financial collapse. But while the danger came and went, their quantitative easing stayed. Since 2008, the monetary base of the EU rose 7.2 times, Japan’s 7.3 times, and the U.S.’s 8.3 times.

Adding insult to injury, this historically unprecedented breakdown of monetarist policy was accompanied by an equally radical refutation of monetarist theory. Recall that monetarism claims that money growth fuels inflation — yet despite the monetary explosion, inflation refused to cooperate. From 2008 to 2020, consumer prices rose by only 29% in the U.S, 17% in the EU and a mere 3% in Japan.

For more: see ‘Can Capitalists Afford Recovery? Three Views on Economic Policy in Times of Crisis’.

… is there a specific event that we should consider as the key trigger? Doesn’t this all coincide with the end of Bretton Woods?

I don’t know about triggers, events and Bretton Woods.

From a CasP viewpoint, the reason seems straightforward.

Neoliberalism is the rule of dominant capital; this rule is based on the hierarchical growth of dominant capital; this hierarchical growth amplifies the extent and intensity of strategic sabotage; and in order to avoid systemic implosion, this sabotage must be offset to some extent. That is why neoliberal governments become bigger, the deficits get amplified and their debts soar.

For a recent account of this process, see Dominant Capital and the Government.

Is the small “dead cat bounce” of 2021 (if I’m not mistaken) due to the general Covid-related recovery plans issued in OECD countries?

Could be.

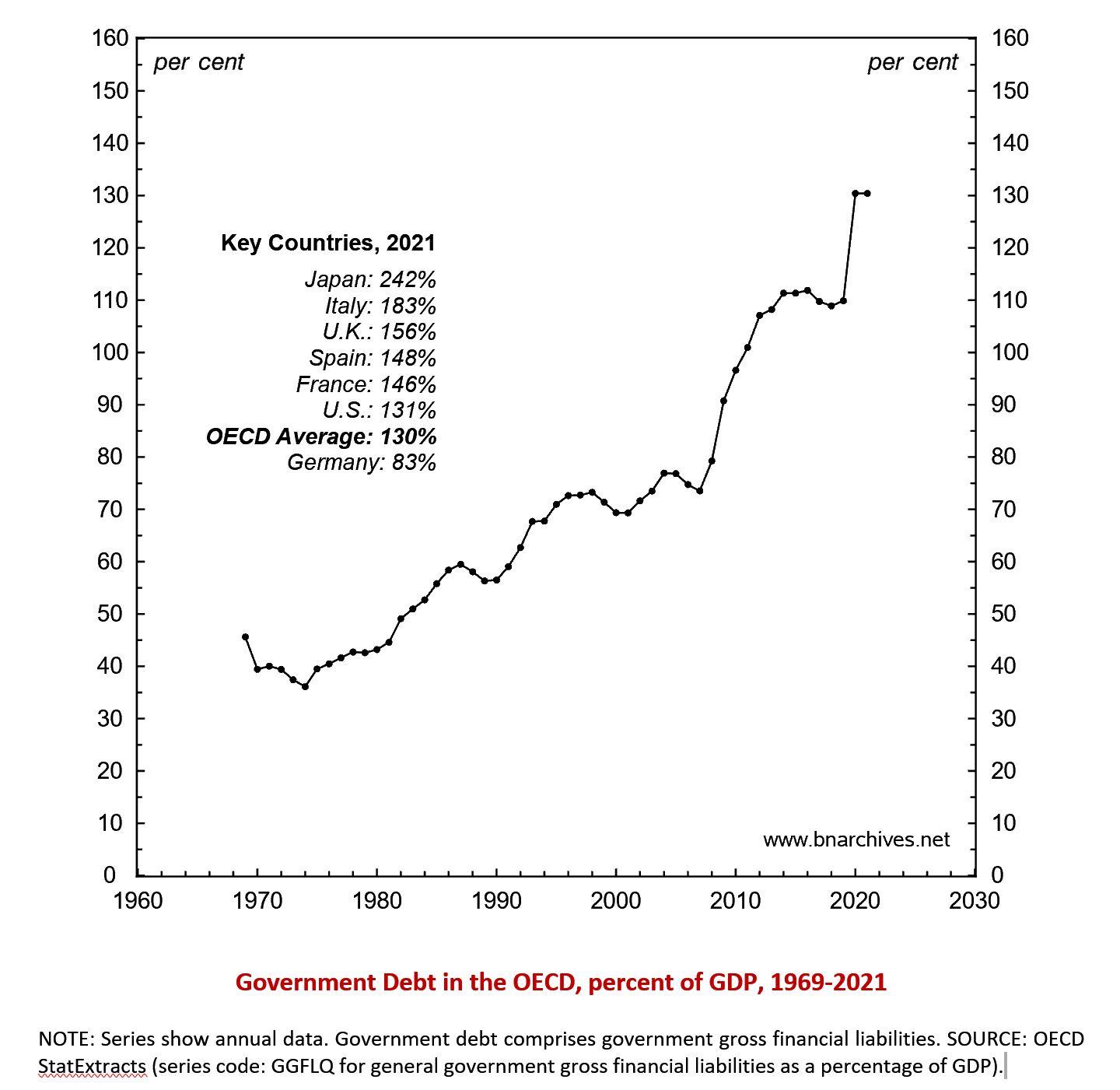

The neoliberal debt balloon: since 1980, the economy grew freer and freer while the OECD government debt/GDP ratio inflated. By 2021, this ratio was three times larger than it was in 1980.

- This reply was modified 4 years, 5 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 5 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 5 months ago by Jonathan Nitzan.

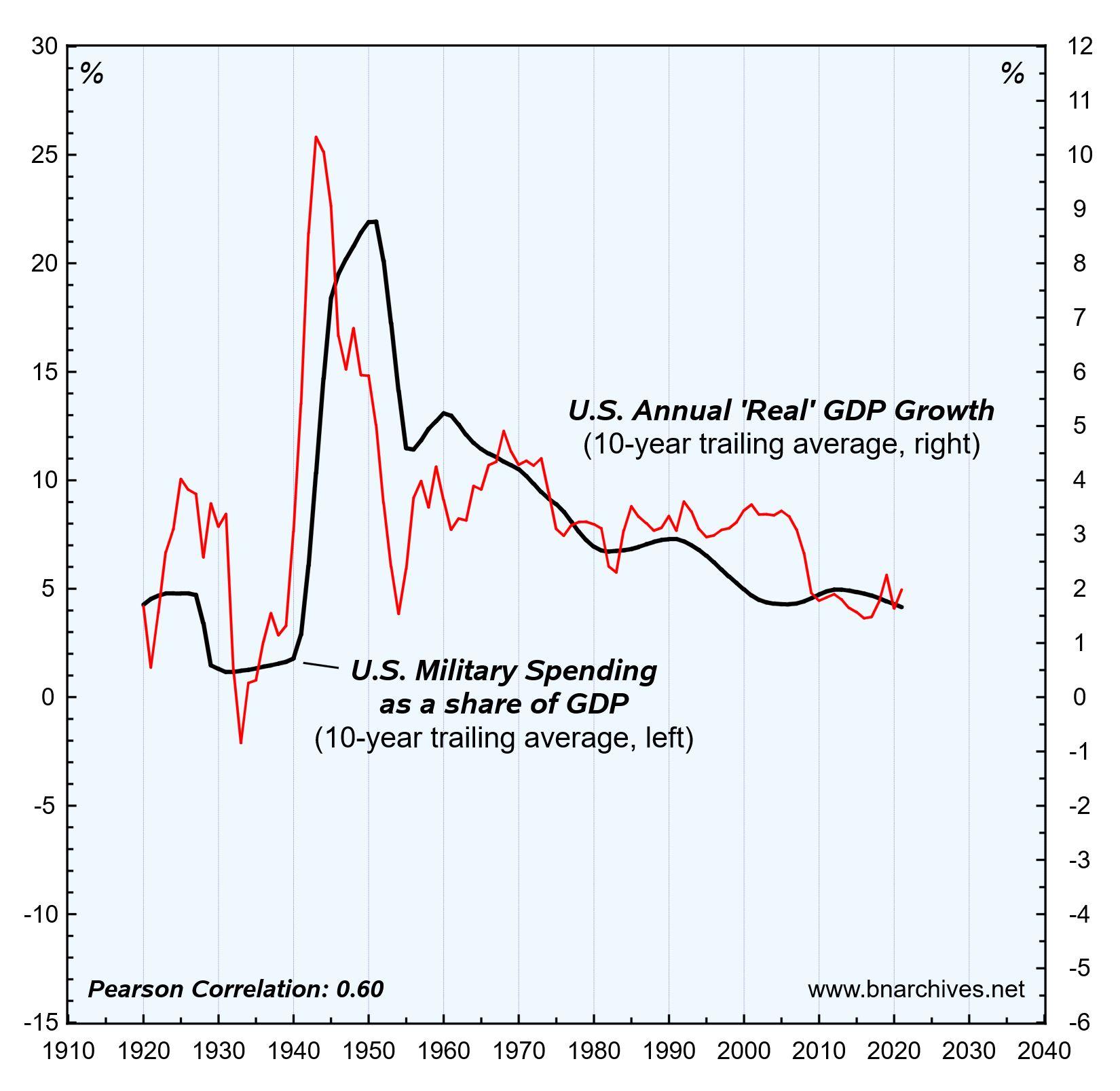

January 25, 2022 at 12:28 pm in reply to: Military Spending and Economic Growth in the United States #247621The reason for displaying the military spending series on a log scale is that it makes correlation visually clearer. Here is what the series look like on regular scales.

- This reply was modified 4 years, 5 months ago by Jonathan Nitzan.

January 25, 2022 at 12:20 pm in reply to: Military Spending and Economic Growth in the United States #247620The correlation is between the 10-year trailing average series.

-

AuthorReplies