Forum Replies Created

-

AuthorReplies

-

Thank you, Michael, for introducing your work and the useful dialogue.

We learn from disagreement.

Thank you Alexander.

Regarding goodwill.

1. When company A acquires or merges with company B, the owners of company A pay for the assets of company B. The price they pay can be high or low, but the result is merely the transfer of the assets previously held by the owners of B to the owners of A. In this specific sense, mergers and acquisitions merely redistribute the ownership of existing assets.

2. The question you raise concerns the fact that acquired assets often rise in price relative to their per-acquisition stock market valuation (an increase that accountants usually attribute to the emergence of ‘goodwill’). This is a very real process, of course, but I’m not sure why it is an issue for your measure of R. As far as I understand it, R aggregates ‘real’ retained earnings, so when retained earnings are used to acquire ‘overpriced’ assets, the extra price due to goodwill — which is merely a polite way of saying greater power — should be eliminated when these retained earnings are deflated back to ‘real terms’.

Personally, I don’t think that ‘real-term’ measures have anything ‘real’ about them; I think that, conceptually, they are totally bogus. But you cannot hold both ends of the stick: if you measure retained earnings in ‘real terms’, then pure price changes should be eliminated. And if your price deflator cannot achieve this conversion, then the deflation process is invalid.

Regarding the aggregation of ‘real’ retained earnings over time.

I’m not sure what this measure tells us. If the Standard Oil of New Jersey retained $20 million of net earnings in 1890, and if this $20 million was used to pay for drilling equipment, train companies, bribed politicians and what not, how much of this equipment, material or immaterial as the case may be, is still a “resource” in 2022? Your method suggests that all of it is, and you argue further that you know its quantity in ‘real terms’. My opinion is that you cannot know either.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

Thank you Alexander.

I have been thinking about the problem of what is capital and capitalism. A problem I have with capitalism as power and capital as sabotage of industry is the startup problem. How can capitalist power be exerted when it is weak compared to other powers? And how can sabotaged industry come to dominate over non-sabotaged industry?

Some ideas about how capital as power was born out of feudalism can be found in Capital as Power, Ch. 13: ‘The Capitalist Mode of Power’.

So what is capital? Capital is what capitalists buy with their profits.

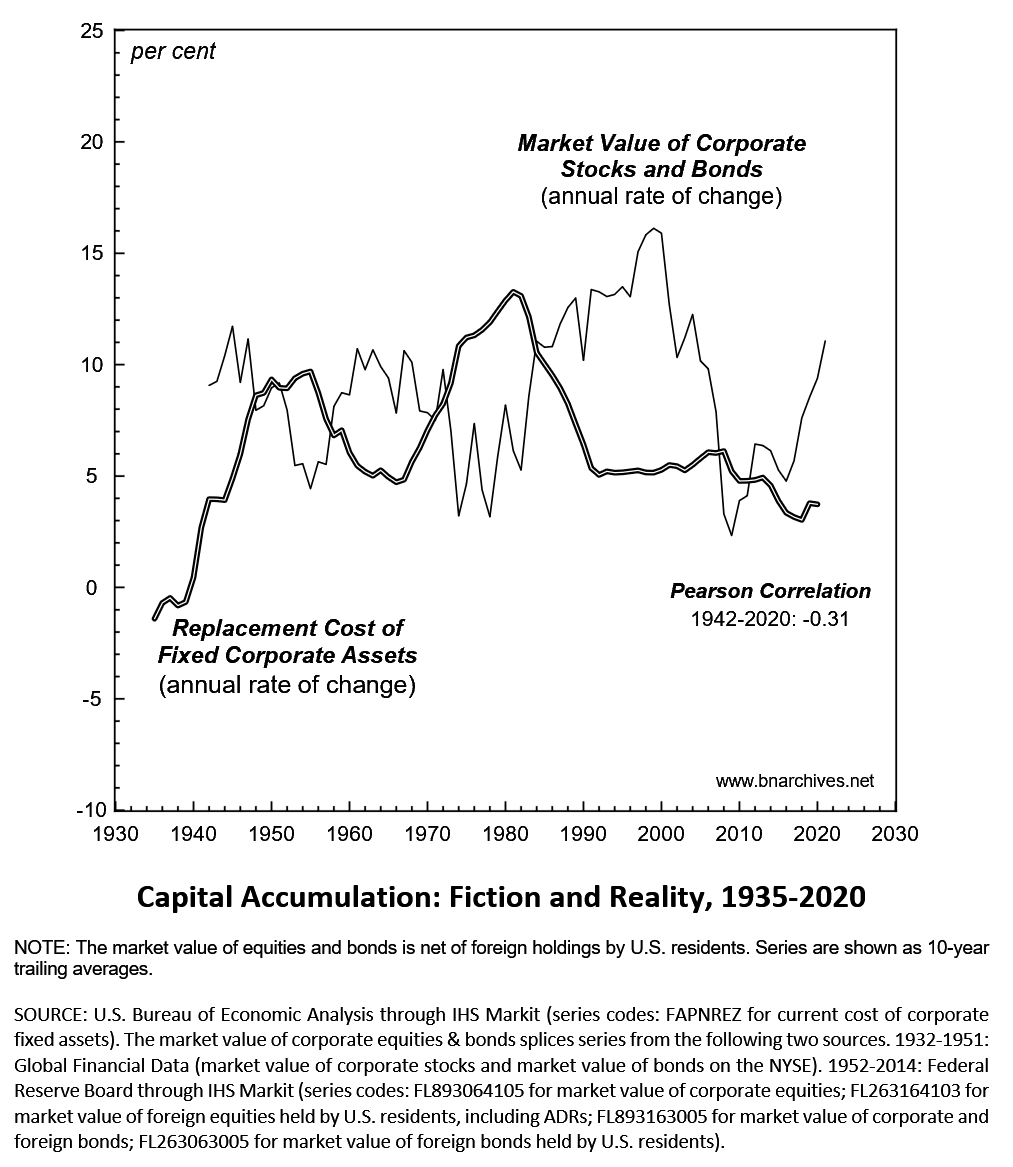

On an aggregate level, what capitalists buy with their profit is plant & equipment, or what economists call ‘real capital’ (buying other companies through mergers or acquisitions doesn’t alter the aggregate of what capitalists own, only redistributes it among them). The problem is that, over the longer haul, the growth rate of the replacement dollar value of ‘real capital’ (economic accumulation) moves inversely with the dollar value of stocks and bonds (financial accumulation). And since for capitalists the key is the latter process rather than the former, economists end up barking up the wrong tree. Here is a graph updated from ‘Capital Accumulation: Fiction and Reality’:

Your aggregation of past retained earnings expressed in ‘real terms’ (R) is backward-looking, so regardless of its theoretical meaning, it’s unclear how it affects forward-looking capitalization.

On ‘real’ measures in economics, see for instance:

- ‘Price and Quantity Measurements: Theoretical Biases in Empirical Procedures’ (1989)

- Capital as Power (2009): Chs. 5 and 8

- ‘The Aggregation Problem: Implications for Ecological and Biophysical Economics’ (2019)

- ‘Real GDP: The Flawed Metric at the Heart of Macroeconomics’ (2019)

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

Thank you Alexander for this interesting view.

You might find CasP analyses of the stock market useful, even if you disagree with them:

- A CasP Model of the Stock Market (2016) https://bnarchives.yorku.ca/494/

- Financial Crisis, Inequality, and Capitalist Diversity: A Critique of the Capital as Power Model of the Stock Market (2020) https://bnarchives.yorku.ca/599/

- How the History of Class Struggle is Written on the Stock Market (2020) https://bnarchives.yorku.ca/658/

- Reconsidering Systemic Fear and the Stock Market: A Reply to Baines and Hager (2021) https://bnarchives.yorku.ca/696/

- The Ritual of Capitalization (2021) https://bnarchives.yorku.ca/707/

Thank you for the clear explanation, Alexander.

Here you say:

R is not cumulative retained earnings divided by a price index.

But here you seem to say the opposite:

For a broad-based index, the value of R can be estimated as the sum of retained earnings in constant dollars

Reading your explanations, it seems to me that you express the common backward-looking notion of ‘real capital’ — namely, that this ‘stock’ is made of past earnings invested in plant, equipment, raw material, knowledge, etc. If I understand you correctly, the difference is that you don’t call this magnitude ‘real capital’ but ‘resources’.

I’m not sure how your view relates to Capital as Power, particularly given (1) that CasP rejects the notion that ‘real capital’ has an objective magnitude, and (2) that capitalization, being the discounted value of risk-adjusted future earning, is theoretically independent of past profit, aggregated or otherwise.

R is not cumulative retained earnings divided by a price index.

P/R is not a ratio of three indices. It is market price of a share divided by the equity value per share with equity calculated on a constant-dollar basis.

I must admit being confused. Forgive me if you have already done so, but could you provide a simple definition + a clear example for both R and P/R?

At the very least, though, the concept of a “market” should require the voluntary exchange of commodities, shouldn’t it?

I don’t think so. All monetary exchange involves aspects of power, so in that sense, it is never entirely or even mostly voluntary. But it is never only about power either. In a company town, the power of the company is significant, but not absolute. If it were absolute — like in a slave plantation or a concentration camp — there would be no need for monetary exchange.

The capitalist mode of power is mediated through monetary exchange. And if exchange is a vehicle of power, you cannot assume it away. In this sense, capitalism sans markets is an oxymoron.

But I could be wrong.

Scot,

Your notion of a “market” refers to the neoclassical setting of perfect competition. But this is only one possible setting, even in neoclassical theory. In capitalism, a market is a setting where commodities are exchanged (usually) for money. This is a very general definition that can accommodate any commodity/ies, participants, institutions and patterns of activity.

If you get rid of this concept, how would you describe the reality it refers to?

Thank you Michael Alexander for the interesting note. Three points.

1.

You define:

R = ‘real’ cumulative retained earnings = cumulative (retained earnings / price index).

According to this definition, R is an aggregation of the ratio between two nominal series. I don’t know how this aggregation is a proxy of ‘real’ capital — first, because retained earnings are at best the consequence of ‘real’ capital; and second, because ‘real’ capital, understood as a material/productive entity, is unknowable to anyone and everyone, including economists. Yes, Marxists claim that the ‘capital stock’ is ploughed-back surplus value (incarnated as ‘real’ retained earnings), though you cannot operationalize this claim with historical summation when prices deviate from values (whatever they might be) and when technical change makes existing plant and equipment useless/worthless to an unknowable degree.

2.

You define:

P/R = S&P 500 price index / R = S&P 500 price index / cumulative (retained earnings / price index).

This is a relationship between three nominal indices. It is bounded because the denominator R is a rising series with the same slope as the stock market trend. Take any other rising series with a similar slope — or the stock market trend for that matter — and you get the same result.

3.

I’m not sure I understand your last chart and associated explanation.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

Sundry thoughts on the state of capital:

1. What makes the capitalist mode of power unique, is that it offers a universal measure of power relations in the form of differential capitalization (and its underlying elementary particles – differential future earnings, differential hype and differential risk).

2. Differential capitalization is not only universal, but also increasingly encompassing. It penetrates and creorders more and more power relations in society, minute and grand. And this penetration and creordering makes the mode of power – or the state of capital, as we call it – appear in constant flux.

3. This flux is deeply dialectical in that it interrelates the imposition of power and resistance to this imposition in what Ulf Martin (2019) calls an ‘autocatalytic sprawl’: the imposition of so-called rational power elicits ‘irrational’ resistance, which in turn calls for further impositions, further resistance, and so on.

4. In this context, the key question concerns the limits, or asymptotes, of this process. The capitalist incarnation of Lewish Mumford’s megamachine is probably the tallest, strongest and most encompassing the world has ever known. But these superlatives also indicate that it might be pushing against some limits beyond which its autocatalytic sprawl might implode. For more on these limits and their implications, see ‘The Asymptotes of Power’ (2012), ‘A CasP Model of the Stock Market’ (2016), and ‘Growing through Sabotage’ (2020).

5. The conventional conception of the modern state as a distinct entity, related to but conceptually separate from capital, is ill-equipped to deal with these integrated processes. James C. Scott’s notion of ‘legibility’ is theoretically trivial (and ‘not particularly original’, in his own words). Relations of power, by their very nature, creorder the universe on which they are imposed. And the process by which rulers make the terrain legible to them is by no means new. It’s written all over the history of the earliest states (just read Frankfort et al., Kramer and Mumford).

6. What is novel is that the logic of capital creordered a new state of capital out feudalism (see Ch. 13 in Capital as Power) . In this sense, the modern state is a creature of capitalism, just like capitalism is inconceivable without a state. They are two sides of the same thing: the state of capital.

7. Bottom line. Power relations, including those created by states (conventionally understood), can be and often are quantified. But they are quantified in different ways with different principles and distinct units. It is only when these relations are subjected and translated to the universal logic of capital (as power), that they too become universal….

***

Frankfort, Henri, H. A. Groenewegen-Frankfort, John Albert Wilson, Thorkild Jacobsen, and William Andrew Irwin. 1946. The Intellectual Adventure of Ancient Man. An Essay on Speculative Thought in the Ancient Near East. Chicago: The University of Chicago press.

Kramer, Samuel Noah. 1956. [1981]. History Begins at Sumer. Thirty-Nine Firsts in Man’s Recorded History. 3rd rev. ed. Philadelphia: University of Pennsylvania Press.

Mumford, Lewis. 1967. The Myth of the Machine. Technics and Human Development. New York: Harcourt, Brace & World, Inc.

Mumford, Lewis. 1970. The Myth of the Machine. The Pentagon of Power. New York: Harcourt, Brace Jovanovich, Inc.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

January 6, 2022 at 5:17 pm in reply to: Inflation is always and everywhere a redistributional phenomenon #247475Here is Joseph Baines’ 2013 figure updated till 2021, showing how differential inflation continues to redistribute profit well into the present.

Inflation is always and everywhere a process of redistribution.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

January 4, 2022 at 11:34 am in reply to: Inflation is always and everywhere a redistributional phenomenon #247474For those interested in reading more on the subject, here is a list of some of our CasP analyses of oil:

- The Political Economy of Armament and Oil – A Series of Four Articles (1989) https://bnarchives.yorku.ca/136/

- Bringing Capital Accumulation Back In: The Weapondollar-Petrodollar Coalition – Military Contractors, Oil Companies and Middle-East “Energy Conflicts” (1995) https://bnarchives.yorku.ca/13/

- Putting the State In Its Place: US Foreign Policy and Differential Accumulation in Middle-East “Energy Conflicts” (1996) https://bnarchives.yorku.ca/11/

- The Global Political Economy of Israel (2002) https://bnarchives.yorku.ca/8/

- It’s All About Oil (2003) https://bnarchives.yorku.ca/38/

- Dominant Capital and the New Wars (2004) https://bnarchives.yorku.ca/1/

- New Imperialism or New Capitalism? (2006) https://bnarchives.yorku.ca/203/

- Still About Oil? (2015) https://bnarchives.yorku.ca/432/

- Profit Warning: There Will Be Blood (2017) https://bnarchives.yorku.ca/432/

- Still in the Danger Zone (2020) https://bnarchives.yorku.ca/634

January 1, 2022 at 7:17 pm in reply to: Costly Efficiencies Working Paper – Critical feedback #247460Hi Chris:

I have a technical point to make.

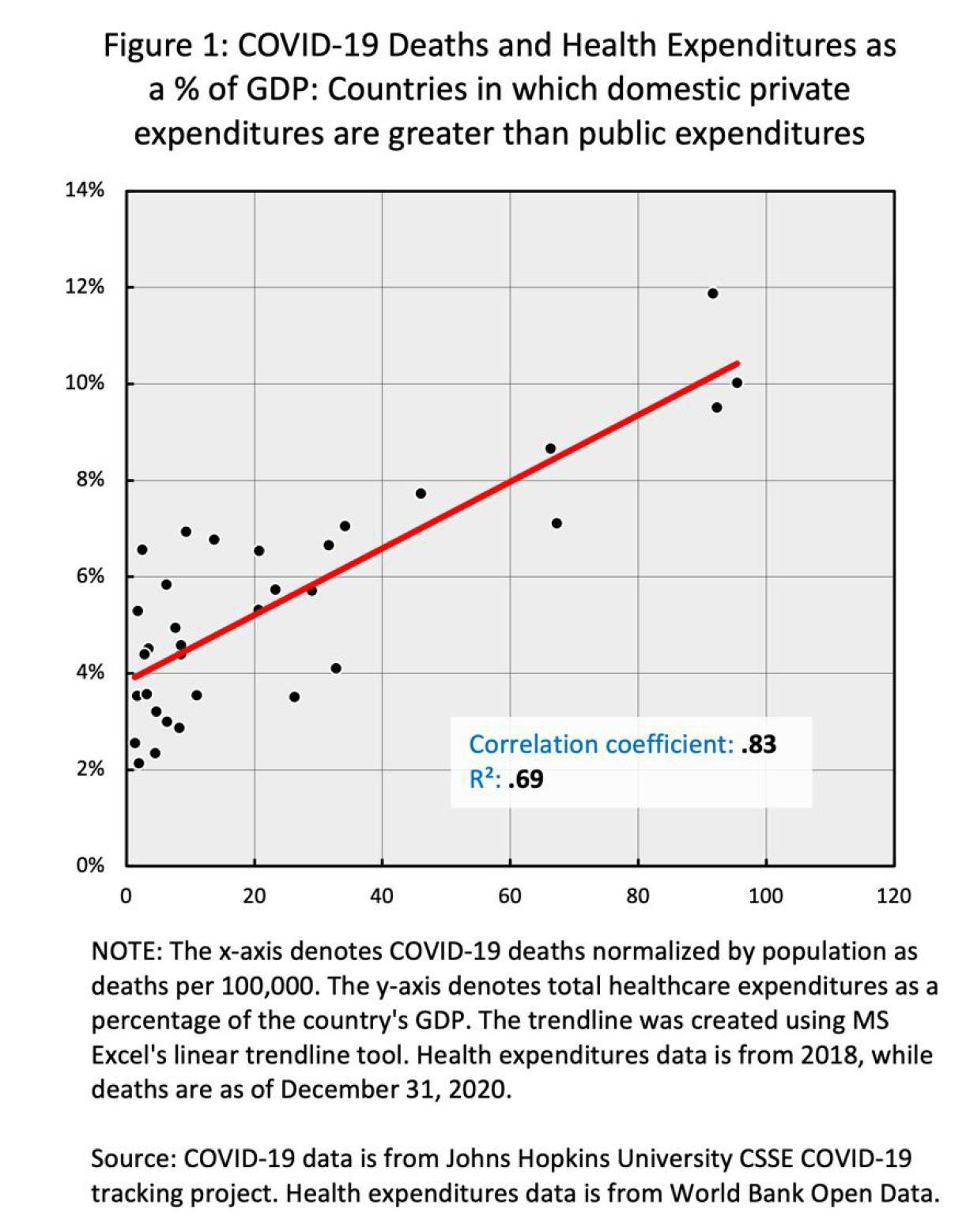

Your paper looks at the relationship between health expenditures and Covid19 deaths, implying that the former has a varying effect on the latter, depending on the public/private expenditure mix.

Your chars make this implied causality potentially difficult to follow. In the sciences, it is conventional to plot the implied cause on the horizontal axis and the effect on the vertical one. Your figures — such as the one reproduced below — invert this convention. They put the effect on the horizontal axis and the cause on the vertical one. Changing the axes will make your results easier to read.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

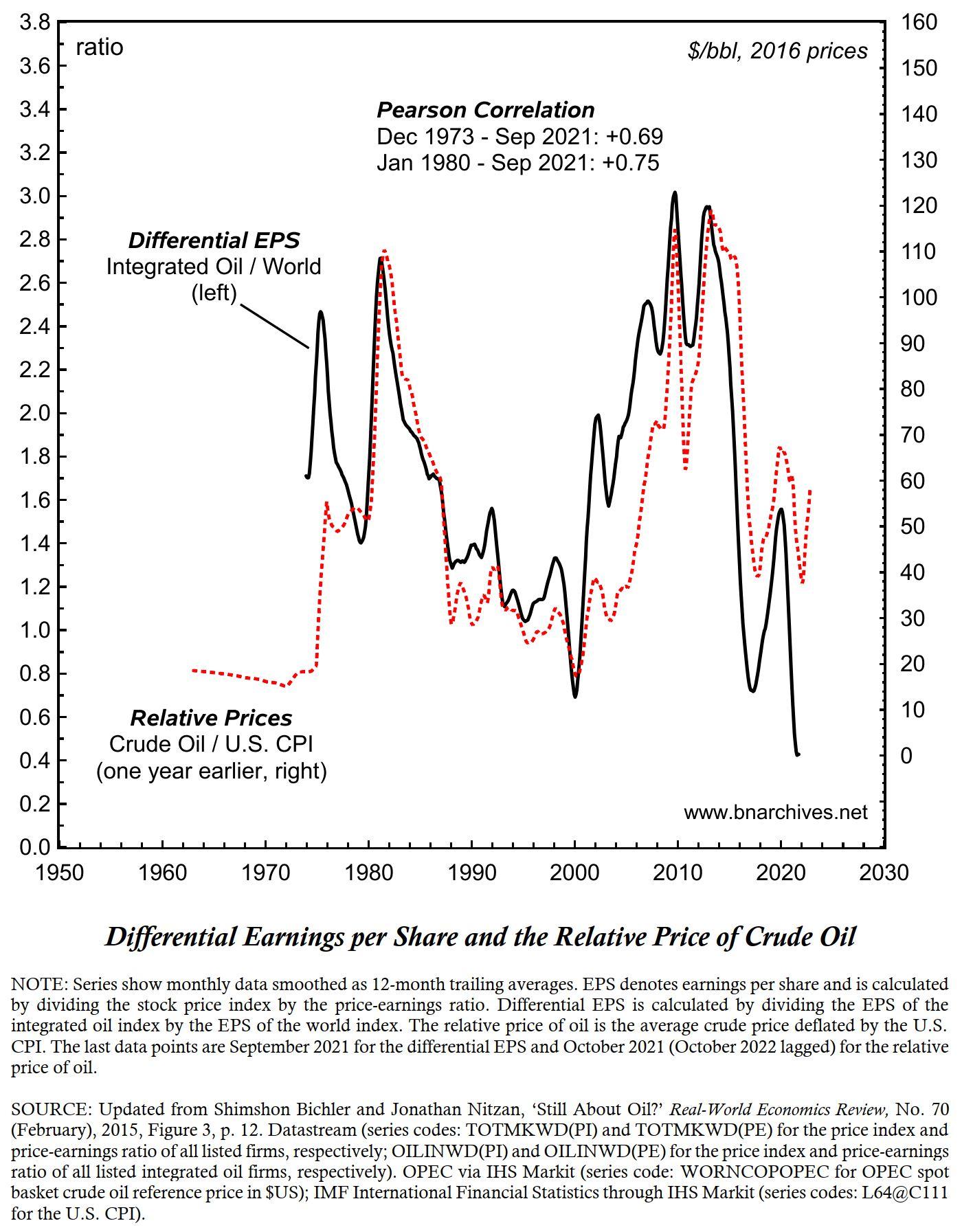

December 29, 2021 at 4:34 pm in reply to: Inflation is always and everywhere a redistributional phenomenon #247445Relative oil prices and differential oil profits

By Shimshon Bichler & Jonathan Nitzan

***

If you thought that oil profits are about producing oil, think again.

The enclosed chart, updated from our 2015 Real-World Economics Review paper, ‘Still About Oil?’, shows that the main determinant of oil profit — and specifically of differential oil profit — is not output, but prices.

The figure shows the correlation between two series: (1) the differential oil profits of the world’s integrated oil companies, computed as the ratio between their earnings per share and the earnings per share of all listed firms; and (2) the relative price of oil one year earlier, measured by the $ price of crude oil relative to the U.S. consumer price index. (The reason for the annual lag is that ‘current’ profits represent a trailing average of earnings recorded over the past 12 months.)

When we wrote the article in 2015, differential oil profits and the relative price of oil were both at record highs; nowadays, they brush against record lows. And that pattern is to be expected. As the chart shows, the correlation between these two measures remains positive and tight, with a Pearson coefficient of +0.69 for the entire period since Dec 1973, and +0.75 since January 1980.

Inflation is always and everywhere a re-distributional phenomenon.

(And expect differential oil profits to rise next year.)

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 4 months ago by Jonathan Nitzan.

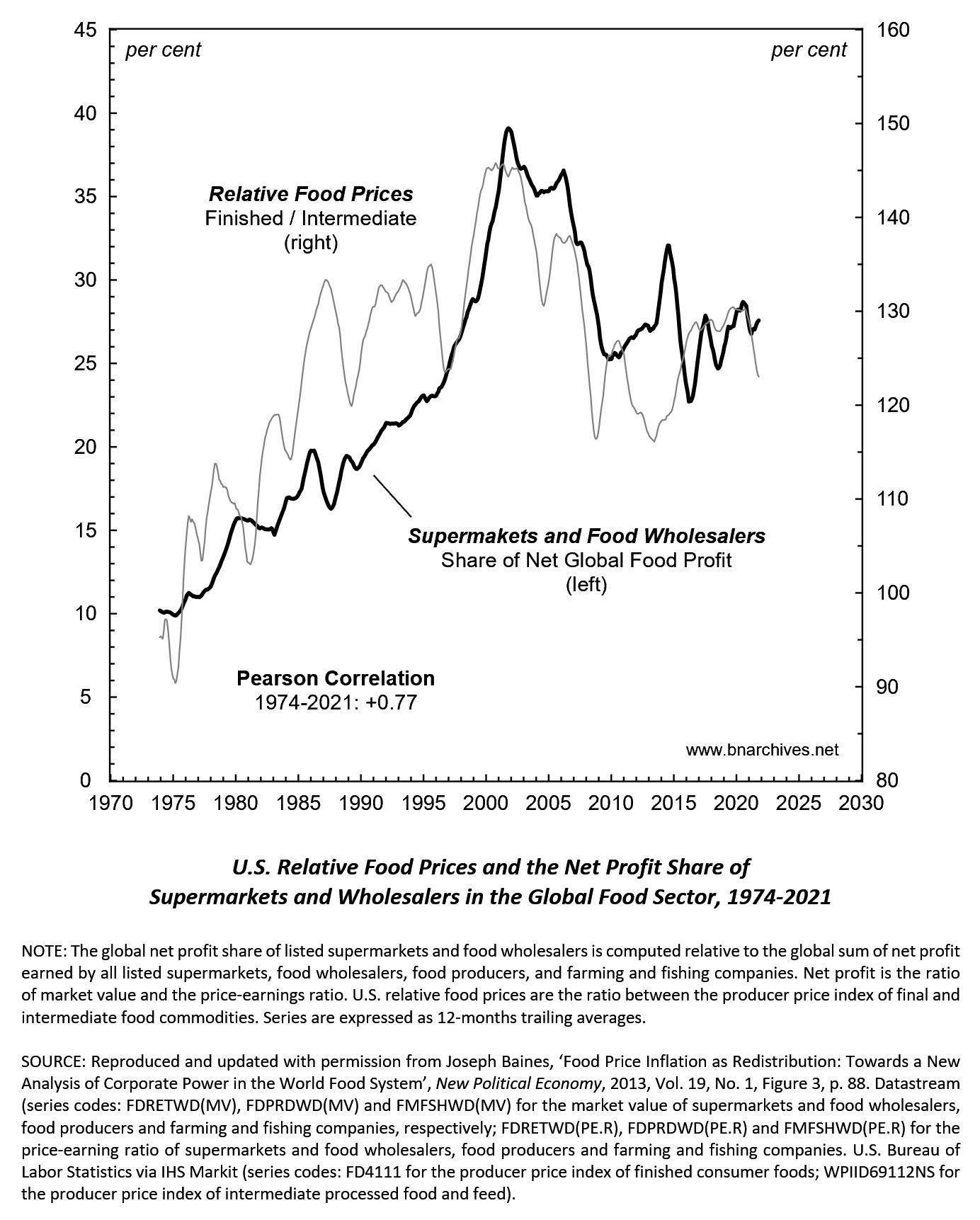

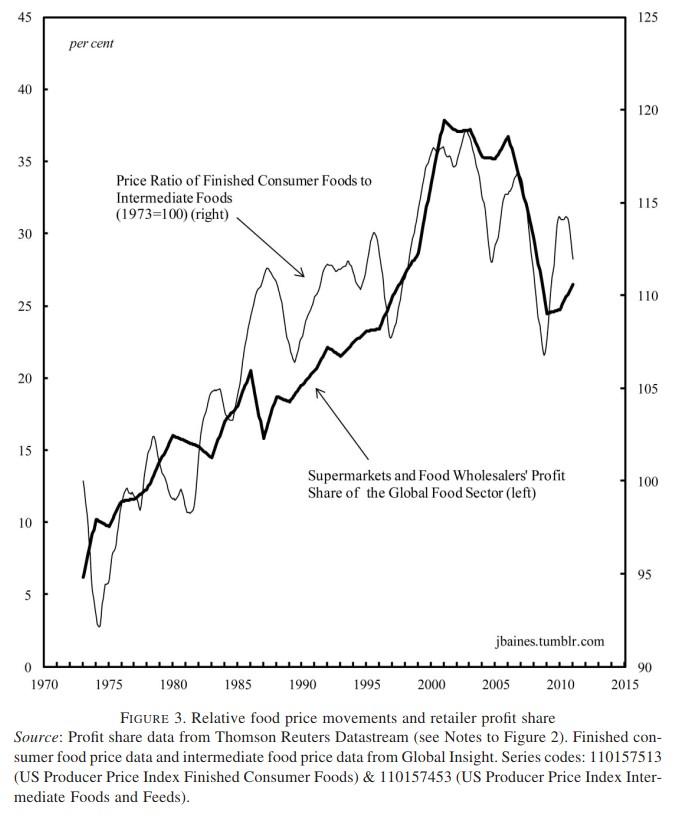

December 27, 2021 at 8:12 pm in reply to: Inflation is always and everywhere a redistributional phenomenon #247441This figure is from Joseph Baines’ 2013 New Political Economy paper ‘Food Price Inflation as Redistribution: Towards a New Analysis of Corporate Power in the World Food System’, p. 88.

The chart shows how differential inflation, shown here by changes in the price ratio between finished consumer foods and intermediate goods, altered the profit share of supermarkets and wholesalers in the global food sector.

Inflation redistributes income, practically always, and often systematically.

-

AuthorReplies