Forum Replies Created

-

AuthorReplies

-

Which brings me to a question. Differential accumulation is central to CasP, but how do we compare the relative power of states using fundamentally different modes of power? North Korea seems to have gained a position of relative stasis of power through it’s isolationism, and while other states gain and lose power relative to each other, North Korea seems to plod along without significant change.

Good question.

All capital is power, but not all power is capital. The capitalist mode of power is fundamentally different from other modes of power in that it offers a universal measure of capitalized power. As the ritual of differential capitalization spreads, influences, absorbs and incorporates more and more aspects of power, the measurements of capitalized power become more meaningful, encompassing and easier to assess.

This encompassing process started in the bourgs of the late middle ages and continues today. The capitalized aspects of social power within capitalists societies expand, while capitalism itself expands and gradually takes over previously non-capitalist societies (see our 2010 ‘Notes on the State of Capital’).

However, relations of power that do not get capitalized — for instance, the North Korea regime — lack universal quantities and therefore remain difficult to ‘compare’ to other relations of power, including capitalized ones. Moreover, the ‘autocatalytic sprawl’ of capitalized power analyzed by Ulf Martin suggests that the very process of capitalizing power generates its own negation in the form of new uncapitalized power/counter-power, and since this sprawl is self-generating, it implies that capitalized power can never become fully encompassing.

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

November 22, 2021 at 4:30 pm in reply to: Inflation is always and everywhere a redistributional phenomenon #247207I wonder if you would be able to share the underlying data.

Enclosed is our Excel data file for active corporations reported by the U.S. IRS. The file includes the number of corporations and their business receipts.

Could you clarify how you calculate the markup of the Compustat 500?

Regarding the profit markup for the Compustat 500 and the U.S. business sector: both are computed by dividing aggregate net profit for all firms in the group by aggregate sales for all firms in the group.

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

Attachments:

You must be logged in to view attached files.November 15, 2021 at 6:19 pm in reply to: Modelling the State of Capital (or At Least Trying to Do So) #247182Looking forward to seeing your ideas enable new research.

November 14, 2021 at 10:02 am in reply to: Modelling the State of Capital (or At Least Trying to Do So) #247180The existence of two different mediums of exchange (money and capital), two different types of objects of exchange (commodities and financial assets), and the two different approaches to pricing them (cost-plus v. present valuation of future income), suggest two distinct economies (even two distinct poleis), which are shown here in Figure 3 as the “Political Economy” and the “Financial Economy.” I considered labeling each domain a “market,” but the market metaphor suggest freedom that does not exist in the state of capital. The key concept is that there are two distinct domains that are inter-dependent, but the domain of Finance/capital dominates.

I think your grappling with these issues is interesting an potentially fruitful for research. But until we see how it is fruitful, a few more observations/questions.

(1) Two distinct economies? Yes and no. On the face of it, money is not the same as capital (although you can argue that, in the capitalist mode of power, money is capital with zero expected profit); commodities are different than financial assets (though you can argue that, in the capitalist mode of power, commodities are financial assets with a zero expected profit); and the pricing of commodities is different from the pricing of future income (although, in the capitalist mode of power, this difference disappears when commodities are sold to be delivered in the future, which suggests that the difference has to do with temporarily).

(2) Regardless of my reservations in (1) , there is the issue of parsimony. I’m just wondering which of your claims requires tucking the finance/political economy duality on top of CasP. At this point, it seems to me that all your claims here can be examined without this extra duality — though, I’d be happy to see your future research prove me wrong!

(3) FIRE. You argue that real-estate and insurance were crucial in the emergence of capitalism, which is true — but how is this relevant to Finance as an analytical category?

November 11, 2021 at 5:21 pm in reply to: Modelling the State of Capital (or At Least Trying to Do So) #247166Thanks, Scot. Here are a few questions/comments.

1.

In your outline, FINANCE = FIRE = Banks, insurance, real-estate. I understand why you think of banks as ‘Finance’: allegedly, they are the ones who create money. But why do you lump insurance and real estate together with them?

2.

You distinguish between the ‘financial economy’ and the ‘political economy’, but you recognize that capitalists, governments and the underlying population exist in both, and that each of their actions has simultaneous financial and political-economy ramifications. With this in mind, how is this bifurcation useful?

3.

CasP researchers have discussed prices (especially the pricing of financial assets) at length, but something that I have not seen discussed before in CasP is the importance of the cost of capital (Financial Economy) and the cost of credit (Political Economy) to differential accumulation. For example, larger companies, whether size is measured by market cap or annual revenues, generally have lower costs of capital, i.e., it costs larger companies less to increase their power.

Baines and Hager researched this process in their 2021 paper ‘The Great Debt Divergence and its Implications for the Covid-19 Crisis: Mapping Corporate Leverage as Power’.

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

Cinema

Shimshon Bichler and Jonathan Nitzan

Jerusalem and Montreal, November 2021First posted on The Bichler and Nitzan Archives.

Unlike books, cinema directs and controls our attention and leaves less to the imagination. But that’s why we love it: it grabs us. And even if it isn’t always as deep as books, it can still teach us plenty. Here is a list of movies and series we liked, along with their directors/creators and the year/s in which they first screened.

1. 8½ (Federico Fellini, 1963)

2. 12 (Nikita Mikhalkov, 2007)

3. 12 Angry Men (Sidney Lumet, 1957)

4. 1900 (Bernardo Bertolucci, 1976)

5. 2001: A Space Odyssey (Stanley Kubrick, 1968)

6. ’71 (Yann Demange, 2014)

7. A Clockwork Orange (Stanley Kubrick, 1971)

8. Across the Universe (Julie Taymor, 2007)

9. All About My Mother (Pedro Almodóvar, 1999)

10. Amadeus (Miloš Forman, 1984)

11. Amarcord (Federico Fellini, 1973)

12. American Beauty (Sam Mendes, 1999)

13. Amores Perros [Love is a Bitch] (Alejandro González Iñárritu, 2000)

14. Angel Heart (Alan Parker, 1987)

15. Apocalypse Now (Francis Ford Coppola, 1979)

16. Arabian Nights (Pier Paolo Pasolini, 1974)

17. Bagdad Café (Percy Adlon, 1987)

18. Ballad on Naryama (Shôhei Imamura, 1983)

19. Barry Lyndon (Stanley Kubrick, 1975)

20. Bedrag [Follow the Money] (Series, Jeppe Gjervig Gram, Jannik Tai Mosholt, Anders Frithiof August, 2016-)

21. Being There (Al Ashby, 1979)

22. Betrayed (Costa-Gavras, 1988)

23. Black Cat, White Cat (Emir Kusturica, 1998)

24. Blood Simple (Joel and Ethan Coen, 1985)

25. Brazil (Terry Gilliam, 1985)

26. Breaking the Waves (Lars von Trier, 1996)

27. Breathless (Jean-Luc Godard, 1960)

28. Brother (Aleksey Balabanov, 1997)

29. Burn! (Gillo Pontecorvo, 1969)

30. Céline (Jean-Claude Brisseau, 1992)

31. Chernobyl (Series, Craig Mazin, 2019)

32. Chocolate (Claire Denis, 1988)

33. Cinema Paradiso (Giuseppe Tornatore, 1988)

34. City Lights (Charles Chaplin, 1931)

35. Cyrano de Bergerac (Jean-Paul Rappeneau, 1990)

36. Dances with Wolves (Kevin Costner, 1990)

37. Danton (Andrzej Wajda, 1983)

38. Darwin’s Nightmare (Hubert Sauper, 2004)

39. Das Boot (Wolfgang Petersen, 1981)

40. Das Experiment (Oliver Hirschbiegel, 2001)

41. De Bruit et de Fureur [Sound and Fury] (Jean-Claude Brisseau, 1988)

42. Defiance (Edward Zwick, 2008)

43. Deliverance (John Boorman, 1972)

44. Departed (Yôjirô Takita, 2008)

45. Devs (Series, Alex Garland, 2020)

46. Diva (Jean-Jacques Beineix, 1981)

47. Dog Day Afternoon (Sidney Lumet, 1975)

48. Dogville (Lars Von Trier, 2003)

49. D.O.A. (Annabel Jankel & Rocky Morton, 1988)

50. Donna Flor and her Two Husbands (Bruno Barreto, 1976)

51. Down by Law (Jim Jarmusch, 1986)

52. Dr. Strangelove (Stanley Kubrick, 1964)

53. Eastern Promises (David Cronenberg, 2007)

54. El Norte (Gregory Nava, 1983)

55. Europa Europa (Agnieszka Holland, 1990)

56. Eyes Wide Shut (Stanley Kubrick, 1999)

57. Falling Down (Joel Schumacher, 1993)

58. Fahrenheit 11/9 (Michael Moore, 2018)

59. Fargo (Joel and Ethan Coen, 1996)

60. Fauda, (Series, Lior Raz and Avi Issacharoff, 2015-2018)

61. Fellini’s Casanova (Federico Fellini, 1976)

62. Fight Club (David Fincher, 1999)

63. Fog of War (Errol Morris, 2003)

64. Forrest Gump (Robert Zemeckis, 1994)

65. Full Metal Jacket (Stanley Kubrick, 1987)

66. Gadjo Dilo [The Crazy Stranger] (Tony Gatlif, 1997)

67. Gangs of New York (Martin Scorsese, 2002)

68. Goodfellas (Martin Scorsese, 1990)

69. Gran Torino (Clint Eastwood, 2008)

70. Homeland (Series, Howard Gordon and Alex Gansa, 2011-2020)

71. House of Sand and Fog (Vadim Perelman, 2003)

72. Icarus (Bryan Fogel, 2017)

73. In Darkness (Agnieszka Holland, 2011)

74. In the Mood for Love (Kar Wai Wong, 2000)

75. Inception (Christopher Nolan, 2010)

76. IP5 (Jean-Jacques Beineix, 1992)

77. Jackie Brown (Quentin Tarantino, 1997)

78. JFK (Oliver Stone, 1991)

79. Jules and Jim (François Truffaut, 1962)

80. King of Devil’s Island (Marius Holst, 2010)

81. La Battaglia di Algeri [The Battle of Algiers] (Gillo Pontecorvo, 1966)

82. La Dolce Vita (Federico Fellini, 1960)

83. La Notte di San Lorenzo [The Night of the Shooting Stars] (Paolo & Vittorio Taviani, 1982)

84. Lady Vengeance (Chan-wook Park, 2005)

85. Land of Mine (Martin Zandvliet, 2015)

86. Le Bal (Ettore Scola, 1983)

87. Le Couperet (Costa-Gavras, 2005)

88. Le Dernier Combat [The Last Battle] (Luc Besson, 1983)

89. Le Dernier Métro [The Last Metro] (François Truffaut, 1980)

90. Le Retour de Martin Guerre (Daniel Vigne, 1982)

91. Le Roi et L’oiseau [The King and the Mockingbird] (Paul Grimault, 1980)

92. Le Souffle au Cœur [Murmur of the Heart] (Luis Malle, 1971)

93. Le Temps des Gitans [Time of the Gypsies] (Emir Kusturica, 1998)

94. Les Misérables du XXeme siecle (Claude Lelouch, 1995)

95. Les Plouffe (Gilles Carle, 1981)

96. Les Valseuses [Going Places] (Bertrand Blier, 1974)

97. Letters from Iwo Jima (Clint Eastwood, 2006)

98. Leviathan (Andrey Zvyagintsev, 2014)

99. Life is Beautiful (Roberto Benigni, 1997)

100. Lili Marlene (Rainer Werner Fassbinder, 1981)

101. Little Big Man (Arthur Penn, 1970)

102. Locke (Steven Knight, 2013)

103. Mad Max (George Miller, 1979)

104. Man of Iron (Andrzej Wajda, 1981)

105. Man of Marble (Andrzej Wajda, 1977)

106. Man on Wire (James Marsh, 2008)

107. Matewan (John Sayles, 1987)

108. Memento (Christopher Nolan, 2000)

109. Metropolis (Fritz Lang, 1927)

110. Midnight Cowboy (John Schlesinger, 1969)

111. Midnight Express (Alan Parker, 1978)

112. Mississippi Burning (Alan Parker, 1988)

113. Modern Times (Charles Chaplin, 1936)

114. Mon Oncle [My Uncle] (Jacques Tati, 1958)

115. Montenegro (Dusan Makavejev, 1981)

116. Moneyball (Bennett Miller, 2011)

117. My Left Foot (Jim Sheridan, 1989)

118. Mulholland Dr. (David Lynch, 2001)

119. Music Box (Costa Gavras, 1989)

120. Narcos (Series, Chris Brancato, Carlo Bernard, and Doug Miro, 2015-2017)

121. Network (Sidney Lumet, 1976)

122. Nikita (Luc Besson, 1990)

123. Nobody Speaks (Brian Knappenberger, 2017)

124. Noce Blanche [White Wedding] (Jean-Claude Brisseau, 1989)

125. Norma Rae (Martin Ritt, 1979)

126. No Country for Old Men (Joel and Ethan Coen, 2007)

127. No Direction Home: Bob Dylan (Martin Scorsese, 2005)

128. O Brother, Where Art Thou? (Joel and Ethan Coen, 2000)

129. Of Mice and Men (Lewis Milestone, 1939)

130. Oldboy (Chan-wook Park, 2003)

131. Once Were Warriors (Lee Tamahori, 1994)

132. One Flew Over the Cuckoo’s Nest (Miloš Forman, 1975)

133. Our Daily Bread (Nikolaus Geyrhalter, 2005)

134. Pan’s Labyrinth (Guillermo del Toro, 2006)

135. Paths of Glory (Stanley Kubrick, 1957)

136. Peaky Blinders (Series, Steven Knight, 2013-)

137. Platoon (Oliver Stone, 1986)

138. Pulp Fiction (Quentin Tarantino, 1994)

139. Ragtime (Miloš Forman, 1981)

140. Rashômon (Akira Kurosawa, 1950)

141. Reservoir Dogs (Quentin Tarantino, 1992)

142. Rivers and Tides (Thomas Riedelsheimer, 2001)

143. Robocop (Paul Verhoeven, 1987)

144. Roger & Me (Michael Moore, 1989)

145. Roma (Federico Fellini, 1972)

146. Room (Lenny Abrahamson, 2015)

147. Rosewood (John Singleton, 1997)

148. Run Lola, Run (Tom Tykwer, 1998)

149. Running on Empty (Sidney Lumet, 1988)

150. Satyricon (Federico Fellini, 1969)

151. Schindler’s List (Steven Spielberg, 1993)

152. Searching for Sugar Man (Malik Bendjelloul, 2012)

153. Secrets and Lies (Mike Leigh, 1996)

154. Serpico (Sidney Lumet, 1973)

155. Seven Beauties (Lina Wertmüller, 1975)

156. Seven Samurai (Akira Kurosawa, 1954)

157. Shine (Scott Hicks, 1996)

158. Sicario (Denis Villeneuve, 2015)

159. Sleeping with the Enemy (Joseph Ruben, 1991)

160. Starred Up (David Mackenzie, 2013)

161. Straw Dogs (Sam Peckinpah, 1971)

162. Such a Long Journey (Sturla Gunnarsson, 1998)

163. Sunshine (István Szabó, 1999)

164. Talk to Her (Pedro Almodóvar, 2002)

165. Taxi Driver (Martin Scorsese, 1976)

166. The Act of Killing (Joshua Lincoln Oppenheimer, 2012)

167. The Band’s Visit (Eran Kolirin, 2007)

168. The Big Kahuna (John Swanbeck, 1999)

169. The Bridges of Madison County (Clint Eastwood, 1995)

170. The Bureau (Series, Éric Rochant, 2015-2020)

171. The Celebration (Thomas Vinterberg, 1998)

172. The Century of the Self (Series, Adam Curtis, 2002)

173. The China Syndrome (James Bridges, 1979)

174. The Coca-Cola Kid (Dusan Makavejev, 1985)

175. The Commitments (Alan Parker, 1991)

176. The Cook, The Thief His Wife & Her Lover (Peter Greenaway, 1989)

177. The Crying Game (Neil Jordan, 1992)

178. The Dear Hunter (Michael Cimino, 1978)

179. The Emerald Forest (John Boorman, 1985)

180. The English Patient (Anthony Minghella, 1996)

181. The Full Monty (Peter Cattaneo, 1997)

182. The General (John Boorman, 1998)

183. The Godfather (I, II and III) (Francis Ford Coppola, 1972, 1974, 1990)

184. The Killing Fields (Roland Joffé, 1984)

185. The Last Emperor (Bernardo Bertolucci, 1987)

186. The Life of David Gale (Alan Parker, 2003)

187. The Lives of Others (Florian Hanckel von Donnersmarck, 2006)

188. The Man Who Planted Trees (Frédérick Back, 1988)

189. The Matrix (Lana Wachowsky,1999)

190. The Pianist (Roman Polanski, 2002)

191. The Piano (Jane Campion, 1993)

192. The Return (Andrei Zvyagintsev, 2003)

193. The Road Warrior (George Miller, 1981)

194. The Salt of the Earth (Wim Wenders and Juliano Ribeiro Salgado, 2014)

195. The Sheltering Sky (Bernardo Bertolucci, 1990)

196. The Shining (Stanley Kubrick, 1980)

197. The Silence of the Lambs (Jonathan Demme, 1991)

198. The Stoning of Soraya (Cyrus Nowrasteh, 2008)

199. The Syrian Bride (Eran Riklis, 2004)

200. The Tin Men (Barry Levinson, 1987)

201. The Truman Show (Peter Weir, 1998)

202. The Unbearable Lightness of Being (Philip Kaufman, 1988)

203. The Vanishing (George Sluizer, 1988)

204. The White Ribbon (Michael Haneke, 2009)

205. The Wire (HBO series, 2002-2008)

206. Thelma & Louise (Ridley Scott, 1991)

207. There Will Be Blood (Paul Thomas Anderson, 2007)

208. Titus (Julie Taymor, 1999)

209. Trafic (Jacques Tati, 1971)

210. Touch of Evil (Orson Welles, 1958)

211. Underground (Emir Kusturica, 1995)

212. Unforgiven (Clint Eastwood, 1992)

213. Up (Series, Paul Almond and Michael Apted, 1964-2019).

214. Vitus (Fredi M. Murer, 2007)

215. Waltz with Bashir (Ari Folman, 2008)

216. Waste Land (Lucy Walker, 2010)

217. Week-end (Jean-Luc Godard, 1967)

218. When Father was Away on Business (Emir Kusturica, 1985)

219. Who’s Afraid of Virginia Woolf? (Mike Nichols, 1966)

220. Z (Costa Gavras, 1969)

221. Zazie dans le Métro (Louis Malle, 1960)

222. Un Zoo la Nuit (Jean-Claude Lauzon, 1987)Scot,

You raise many questions, but I think that, at this point, engaging with them will be splitting hair. Perhaps when you write something concrete where these issues become paramount, we can revisit the various metaphors and categories and see whether our differences, if any, matter or not.

- This reply was modified 4 years, 9 months ago by Jonathan Nitzan.

Broad concepts/metaphors are always loose and contested.

What/who was the “operational symbol” of Mumford’s original Mega-Machine? Was it the king?

According to Ulf Martin’s The Autocatalytic Sprawl of Pseudorational Mastery, ‘operational symbolism’ appeared only in modernity. The kings in Egypt and Mesopotamia were still locked into ‘magical symbolism’.

Approaching these questions from an entirely different angle, have you considered (or do you assert) that the “state of capital” is logically distinct from the state within whose laws the state of capital operates?

The concept of the ‘state of capital’ begins by defining the ‘state’ as the overall power structure of society and then attributing to it a particular form – ancient kingship, feudal, capitalist, etc. For us, the ‘state of capital’ is a synonym for the ‘capitalist mode of power’. As we see it, the state of capital is the broadest definition of the regime and, in that sense, it contains – rather than being contained by – the normal conception of the state. Thus, in our view, what people normally refer to as the ‘U.S. state’ is part of the state of capital, not the other way around.

From this perspective, capitalism is not a mega-machine, it is a control system (mode of power) whose logic organizes and controls the mode of production for the purposes of perpetuating its control (power).

Isn’t a megamachine a control system? My impression is that this is exactly what Mumford had in mind. But then, metaphors are merely tools to contextualize/enrich/sharpen our understanding, so you can definitely change them to suit your purpose.

What about bank deposits, the value of which are always the par/nominal value of money deposited (assuming no accruing of interest)? Does CasP consider bank deposits as capital? Or does it view bank deposits as “money,” even if it is not in circulation (as the Federal Reserve does)?

We think of bank deposits that pay no interest as capital with zero expected profit. The same applies for any other ‘income-less’ asset.

Second, I agree that the “holder” of the record is immaterial, but is the counter-party to the underlying claim also immaterial? Being the aggregator of and counter-party to all capital imbues Finance with immense power, even though that capital is officially owned by and owed to others.

I’m not sure what you mean by ‘Finance’ with a capital F. We speak about finance with a lower-case f. For us, finance is an operational symbol (in Ulf Martin’s terminology), and that’s it. What most people think of when they speak about Finance is the FIRE sector (finance, insurance and real estate). In our view, this sector is not finance, but merely one institutional/organizational manifestation of finance. As we see it, the FIRE sector, however large, does not control money, credit and debt; the “state of capital” does. It is the ruling capitalist class, its key corporate and government organs and their many-faceted institutions that together dominant and steer the financial process. Banks, insurance and real-estate companies are merely part of that process.

Now, having said that, you are correct that FIRE can and does redistribute income, risks and assets — but so do other sectors, such as raw materials, pharmaceuticals and high-tech firms, sometimes at cross-purposes, sometimes in unison. These redistributional patterns are the details of the differential process of ‘credit at large’ — not the process as such.

- This reply was modified 4 years, 9 months ago by Jonathan Nitzan.

Personally, I also take the quote quite literally to mean that “capital” exists only as tallies in accounting records of financial institutions, and these tallies are indicia of wealth owed to the account holder by the institution that maintains the accounting records (e.g., banks and stock brokerages). Of course, all accounting records record capital transactions, even those of a non-financial business, but as a practical matter all “capital” in developed countries “accumulates” as tallies of accounts held in financial institutions.

Scot,

Our claim that “the quantum of capital exists as finance, and only as finance” can be clarified by breaking it into two parts.

(1) Capital is finance. For capitalists, “capital” are record of ownership (stocks, bonds, real-estate claims, etc.) whose quantity is their forward-looking pecuniary capitalization, and forward-looking capitalization is a financial quantum: its magnitude is risk-adjusted expected future earnings discounted by the normal rate of return.

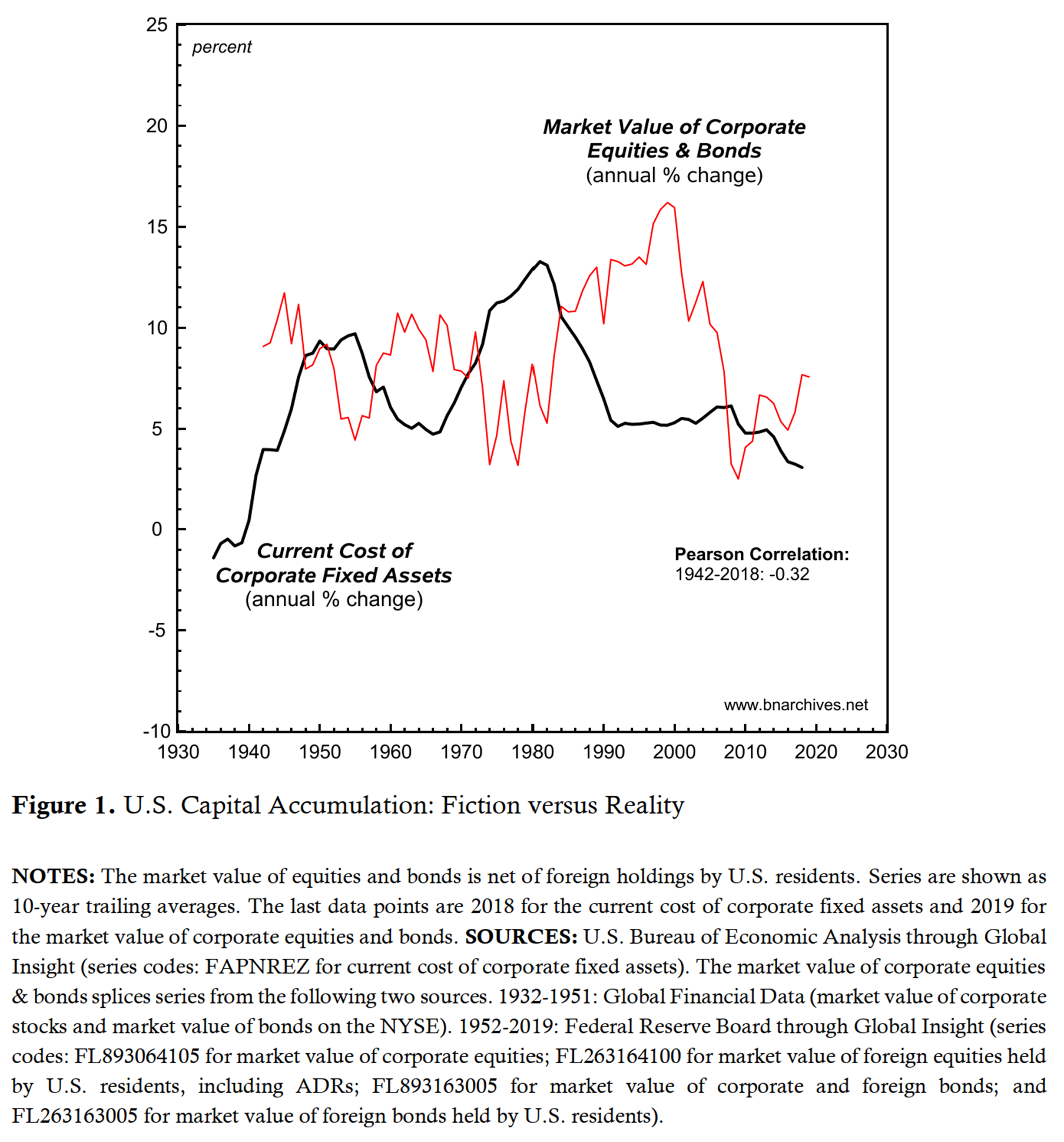

(2) Capital is only finance. The common view that capital=capital goods breaks down because amalgams of heterogeneous capital goods cannot be measured in meaningful ‘real’ units (physical volume, weight, embodied energy, etc., although universal, are not meaningful). Furthermore, even when we measure the money magnitude of capital goods rather than their so-called real magnitude, the movement of this magnitude has little or nothing to do with that of capitalization. In the U.S., the two magnitudes move in opposite directions.

The fact that records of ownership are held by financial institutions is immaterial for these arguments. You could hold them under the mattress and they would still be finance and only finance.

- This reply was modified 4 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 9 months ago by Jonathan Nitzan.

It’s easy to sense the solid foundation behind CasP and behind your answers but what should I read to get a proper handle on it? I guess I need to read some foundational texts and modern texts. Where do I start and where do I read up to? Can you recommend say five or six texts, any size, all original authors (in English, translations available if necessary) and not surveys unless you regard a given survey as belonging in such a small foundational group of texts.

This is not an easy question to answer, and I’m not even sure it is the right question to ask.

I’ve looked through my library for innovative books that influenced our thinking over the years – studies of society, science and history, as well as novels — and I counted about 100. There is no way for me to rank them by their importance. They all are. But reading alone won’t help anyone ‘find his/her way’, so to speak.

Our own experience taught us that to develop our opinion – rather than to adopt the opinion of others – we must do our own empirical/historical research. One reason is that research allows us to ask and perhaps answer questions that others haven’t. But the more important reason, I think, is that it sharpens our sense of judgment. Research allows us to better discern what question are important and what are secondary, or unimportant; which subjects are crucial and which less so, or not at all; which opinions are innovative, and which are silly; etc.

For this reason, I make my course work research dependent. My students, both undergraduate and graduate, are given two empirical assignments and a final theoretical-empirical term paper. The first assignment asks them to mimic my own empirical work; the second makes them answer a series of empirical questions; and the final one requires that they both invent and answer their own theoretically-inspired empirical questions (see https://bnarchives.yorku.ca/702/).

Not everyone is cut for this type of work. But in each class, there are some students who rise to the challenge, and in due course, some of those become first-class political economic researchers. I can also attest that many of these would-be experts started my class with no prior background in political economy, mathematics, and statistics.

So, I know that this method works – and, most importantly, that it is open to anyone. You don’t need to be a university professor, a PhD student, or a math wizard. You only need to be young, regardless of your age.

I hope these notes are useful.

However, when I encounter statements like “Science cannot tolerate logical contradictions,” I become concerned. I am not entirely sure what is meant. Does it mean CasP is pure science and cannot tolerate contradictions?

Let me try to explain.

When scientists encounter logical contradictions — namely, when their theories make contradictory propositions — they become restless and try to resolve these contradictions. Some of the greatest advances in the history of science relate to resolving logical contradictions, usually by proposing new concepts/theories (plus empirical research) that eliminate those contradictions.

The bifurcation of politics and economics tends to generate logical contradictions. When economics assumes self-equilibrating, atomistic markets, this assumption contradicts the recognition by other social scientists that there exist large corporations, governments, unions, NGO and crime syndicates, not to speak of larger networks/hierarchies of these entities. When economists assume that humans are driven by absolute utility maximization, this assumption contradicts the recognition by many other social scientists that humans seek relative power. When economists assume (usually unknowingly) that they can aggregate ‘real’ magnitudes based on individual utility, this assumption is contradicted by other social scientists who think that humans are different from each other and therefore that their utilities cannot be added, that people are often very irrational, that they are largely unaware of their preferences/utilities, and that most of their preferences/utilities are not their own in the first place. I can go on, but I think the point is clear.

Economists treat such contradictions by declaring that one element is a ‘distortion’ of the other, but this treatment leaves the contradictions intact.

How then does CasP deal with human and human system contradictions such as irrationality? Does it mean CasP limits its field of investigation and is not attempting to resolve such contradictions?

I don’t think irrationality per se is a logical contradiction. The logical contradiction arises when the theory assumes that human are always rational as well as that they are often irrational. CasP doesn’t assume that people are rational or irrational. It observes that the thoughts/actions of human beings are shaped, at least in part, by the hierarchical structure in which they exist, and that the result often seems irrational to us (though usually not so to the rulers). It also recognizes that humans are capable of autonomy, and that, under certain circumstances, they might create autonomous relations and perhaps even autonomous societies. Since the position of society on this spectrum is not a starting assumption, but something to be examined, it does not generate logical contradictions of the type I mentioned earlier.

More on these issues: The Capital As Power Approach. An Invited-then-Rejected Interview with Shimshon Bichler and Jonathan Nitzan

Analytically, ‘economics-politics dualists’ — namely all economists, Braudel’s included — begin by conceiving capitalism as a self-regulating atomistic economy, and then tuck on power as a ‘distortion’. This is akin to physicists assuming 4 elements and then adding everything else they know as a ‘distortion’.

Science cannot tolerate logical contradictions — and yet that is exactly what splitting politics from economics ends up doing.

US Lobbying numbers for 2021 (Jan-Sept). Pharmaceuticals industry spends twice the second highest industry (Electronics).

Interesting data, Chris.

(Parenthetically, I think you mean the ‘pharmaceutical business’, not the ‘pharmaceutical industry’.)

Has any progress been made in mapping out the COP-MOPs of capitalism and, especially, its predecessor modes of power?

It’s work in progress.

In the meantime, and if you haven’t already, you might want to have a look at Di Muzio’s The Tragedy of Human Development. A Genealogy of Capital as Power.

-

AuthorReplies