Forum Replies Created

-

AuthorReplies

-

August 29, 2021 at 10:51 am in reply to: Questions on the schism betwen monetary consumption and material consumption #245970

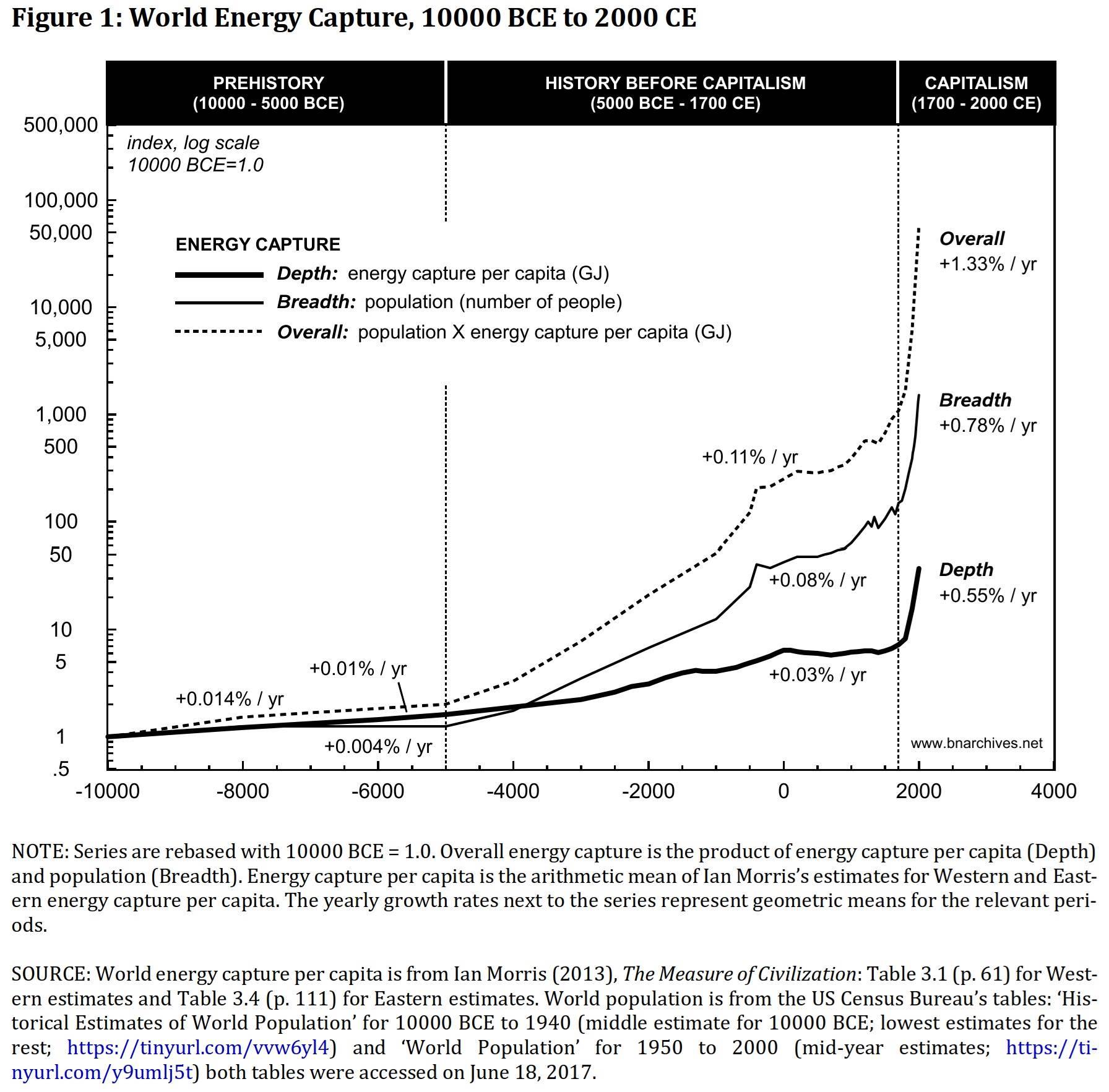

There is no question that, measured in absolute energy term, consumption and income are positively correlated. But in focusing on this correlation and the lavish lifestyle of the rich we might be missing a bigger point.

In our 2020 paper ‘Growing Through Sabotage’, we suggest that the more important question is what part of the energy captured by society goes to wellbeing and what part goes to sustaining and augmenting hierarchical power:

In the paper, we argue that, in the capitalist mode of power, ‘business as usual’ means that the hierarchical share tends rise, and that this relative increase becomes the main driver of energy capture.

If this view is correct, it means that as long as the current capitalist mode of power prevails and expands, the need for more and more hierarchical energy will continue to drive absolute energy capture higher and higher.

From this power viewpoint, the distribution of consumption between rich and poor is more a consequence than a cause.

- This reply was modified 4 years, 11 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 11 months ago by Jonathan Nitzan.

Brian, I think you are correct that ‘sabotage’ could and should be interpreted more generally than the economic restricting of productive capacity. Most broadly, we can conceive sabotage as the restriction of the autonomous, creative capacities of humanity to develop and augment the personal and common good, or something along those lines.

In our 2020 paper Growing Through Sabotage (p. 2, footnote 3), we write.

Note that our notion of strategic sabotage here is broader and somewhat different than Veblen’s (Bichler and Nitzan 2019). Writing at the turn of the twentieth century, Veblen’s main focus was the pecuniary institutions of ‘business’ and the ways in which these institutions undermined the universal efficiency of ‘industry’ for redistributional ends. In this sense, his conception of sabotage was largely confined to the ‘economic’ sphere of production and consumption, investment and waste, credit and finance. The CasP approach, although partly influenced by Veblen, transcends the politics-economics duality from the very beginning and is therefore able to conceive of sabotage not as an economic tool, but as a lever of power more generally.

This broader viewpoint reveals significant historical changes in the nature and application of strategic sabotage. In the ancient states (as well as in prehistoric societies), power was usually exerted openly, directly and violently, and often in ways that seemed arbitrary and random. In later, more complex polities, though – and particularly in modern capitalism – this exertion became much more opaque and roundabout, far less violent and significantly more systematic. In this latter constellation, sabotage is less open and more stealthy: instead of acting positively to affirm and assert the will of the powerful, it operates mostly negatively, by preventing, restricting and undermining the actions of those polities’ subjects. It also grows less violent: instead of using brute force, it often resorts to temptation, manipulation, mental pressure and inbuilt guilt. Finally and crucially, it becomes more methodical: instead of yielding to whim and caprice, it progresses deliberately and calculatedly.

In our 2009 Capital as Power, we discussed sabotage in relation not only to the pace of industry but also — and perhaps more importantly — its very direction (p. 235)

[Examples of] broad industrial diversions include the development by pharmaceutical companies of expensive remedies for invented ‘medical conditions’ instead of drugs to cure real disease for which the afflicted are too poor to pay; the development by high-tech companies of weapon technologies instead of alternative clean energies; the development by chemical and bio-technology corporations of one-size-fits-all genetically modified vegetation and animals instead of bio-diversified ones; the forced expansion by governments and realtors of socially fractured suburban sprawl instead of participatory and sustainable urbanization; the development by television networks of lowest-denominator programming that washes the brain instead of promoting its critical faculties; and so on.

Of course, as we repeatedly noted the line separating the socially desirable and productive from the undesirable and counterproductive is inter-subjective and contestable. But taken together, these examples nonetheless suggest that a significant proportion of business-driven ‘growth’ is wasteful if not destructive, and that the sabotage underlying these socially negative trajectories is exactly what makes them so profitable.

- This reply was modified 4 years, 11 months ago by Jonathan Nitzan.

A few worthwhile novels about Japan, its culture and power structure, by non-Japanese authors:

1. First on the list is James Clavell’s 1975 Shogun. The story takes place in the early 17th century, but you’ll learn from it more than from any other novel. Also, you won’t be able to put it down.

2. The sensational success of ‘Shogun’ lured tens of thousands of university undergraduates to Japanese studies programs. Academic experts on the subject, envious of Clavell’s success, dissected his work but failed to find meaningful inaccuracies.

3. Peter Tasker, a top financial analyst based in Japan, fast-forwards Clavell to the 21st century. His detective novels, like Samurai Boogie and Buddha Kiss, expose the underbelly of modern-day Japan.

4. Jake Adelstein’s 2009 novel Tokyo Vice is the true story of an American crime reporter who got entangled with the Yakuza. Hold on to your seat.

5. Michael Crichton’s novels are almost always sharp and riveting. His 1992 Rising Sun, written when Japan was still seen as a ‘threat’ to American supremacy, is no exception.

- This reply was modified 5 years ago by Jonathan Nitzan.

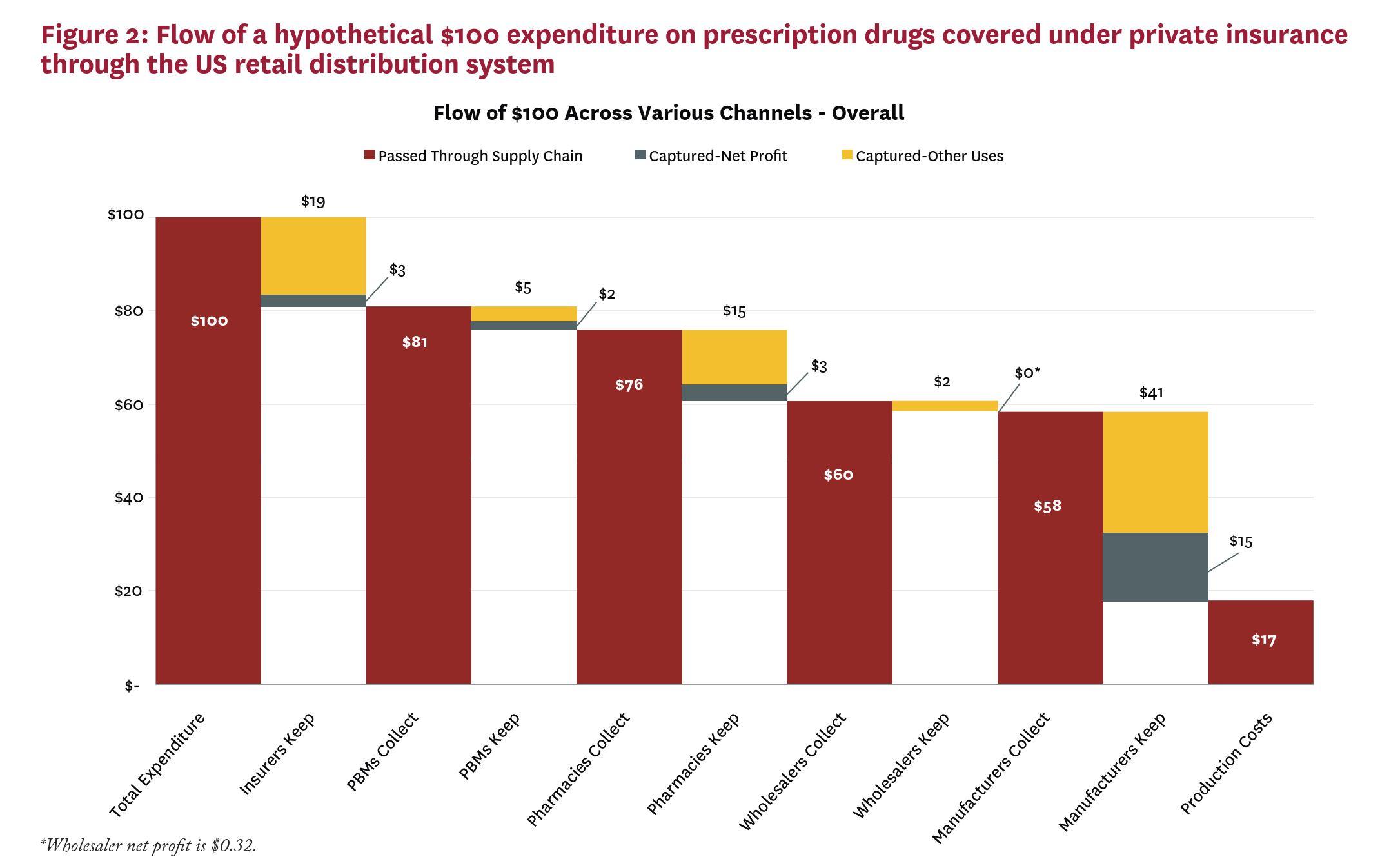

Some breakdown of U.S. drug cost, based on:

Sood, Jeeraj, Tiffany Shih, Karen Van Nuys, and Dana Goldman. 2017. The Flow of Money Through the Pharmaceutical Distribution System. Los Angeles, CA: USCSchaeffer Leonard D. Schaeffer Center for Health Policy Economics.

According to Sood et. al., a $100 drug in the U.S. costs only $17 to produce. The rest goes to the pharmaceutical firms and various intermediaries. A full $23 of the $100 is earned as profit — $15 by the pharmaceutical firms and $8 by the intermediaries.

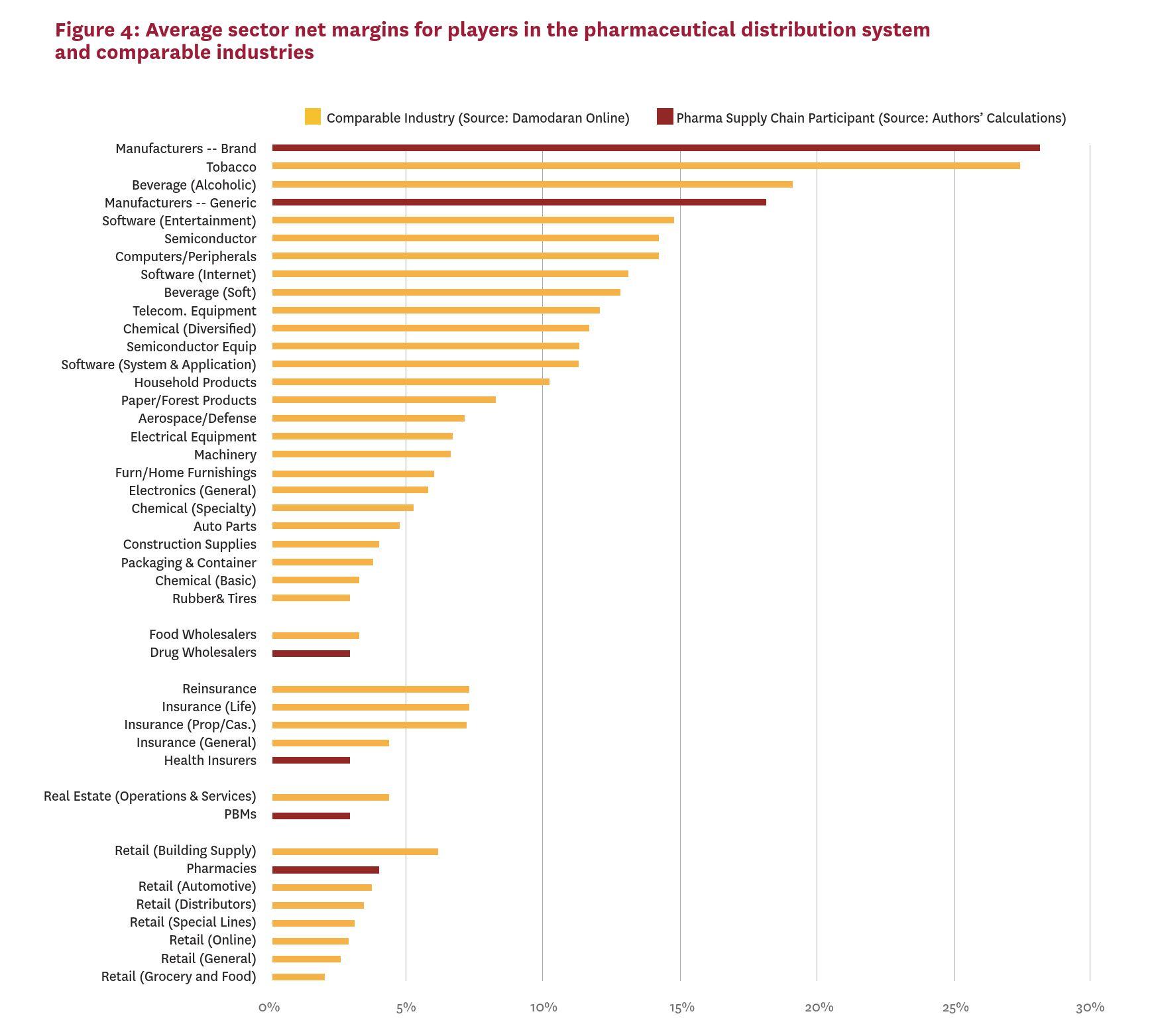

This figure, also from Sood et. al., shows the 2015 net profit margins — i.e., net profit as a % of sales — in various U.S. sectors. Brand pharmaceuticals lead the pack, with generic firms following not far behind.

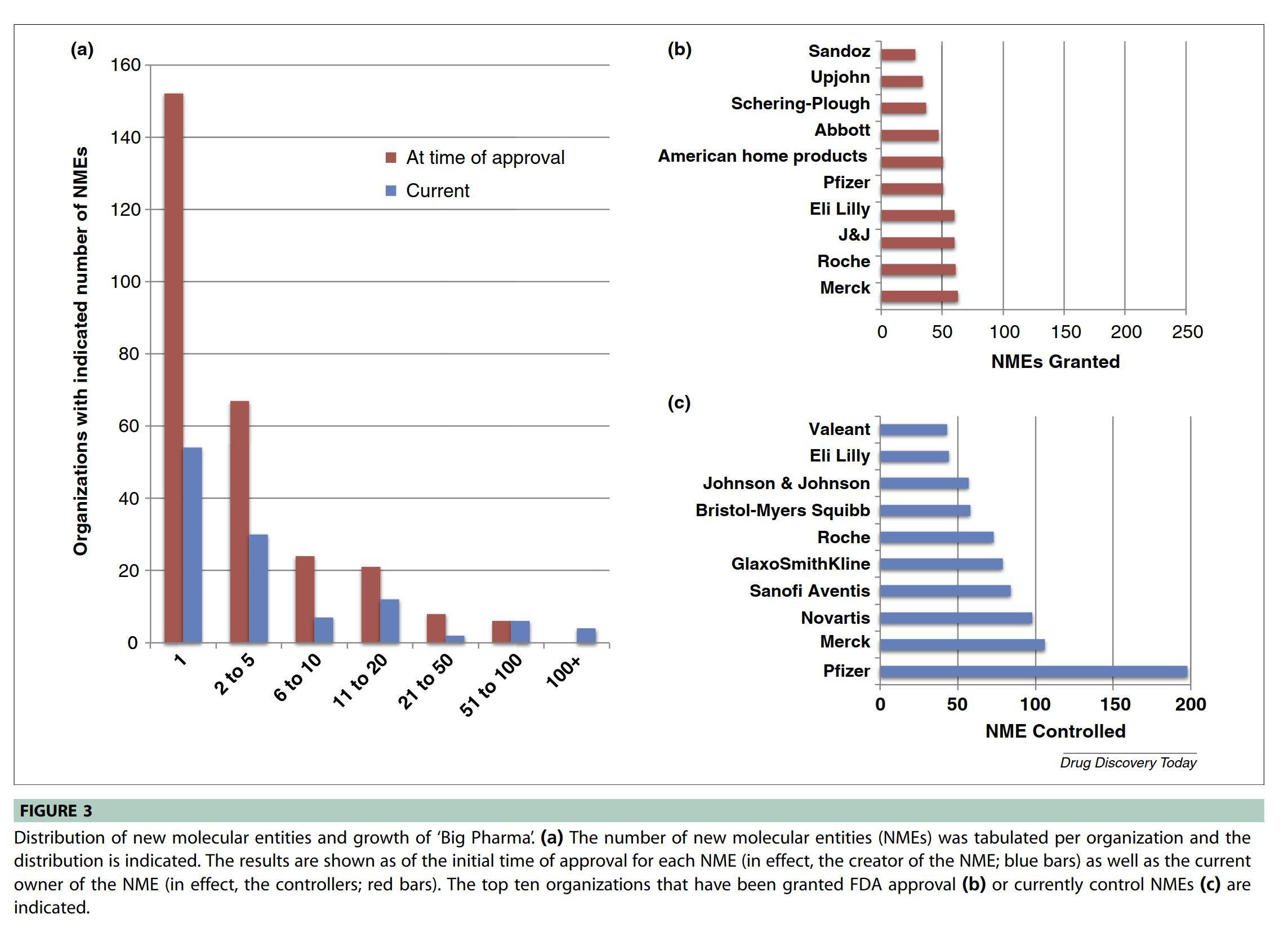

According to Kinch et. al., ownership of new molecular entities (NMEs) has grown highly concentrated – in 2013, the top 10 pharmaceutical firms owned more than 2/3rds of all NMEs, while the top 5 pharmaceutical firms owns over 40%.

Kinch, Michael S., Austin Haynesworth, Sarah L. Kinch, and Denton Hoyer. 2014. An Overview of FDA-Approved New Molecular Entities: 1827-2013. Drug Discovery Today 19 (8, August): 1033-1039.

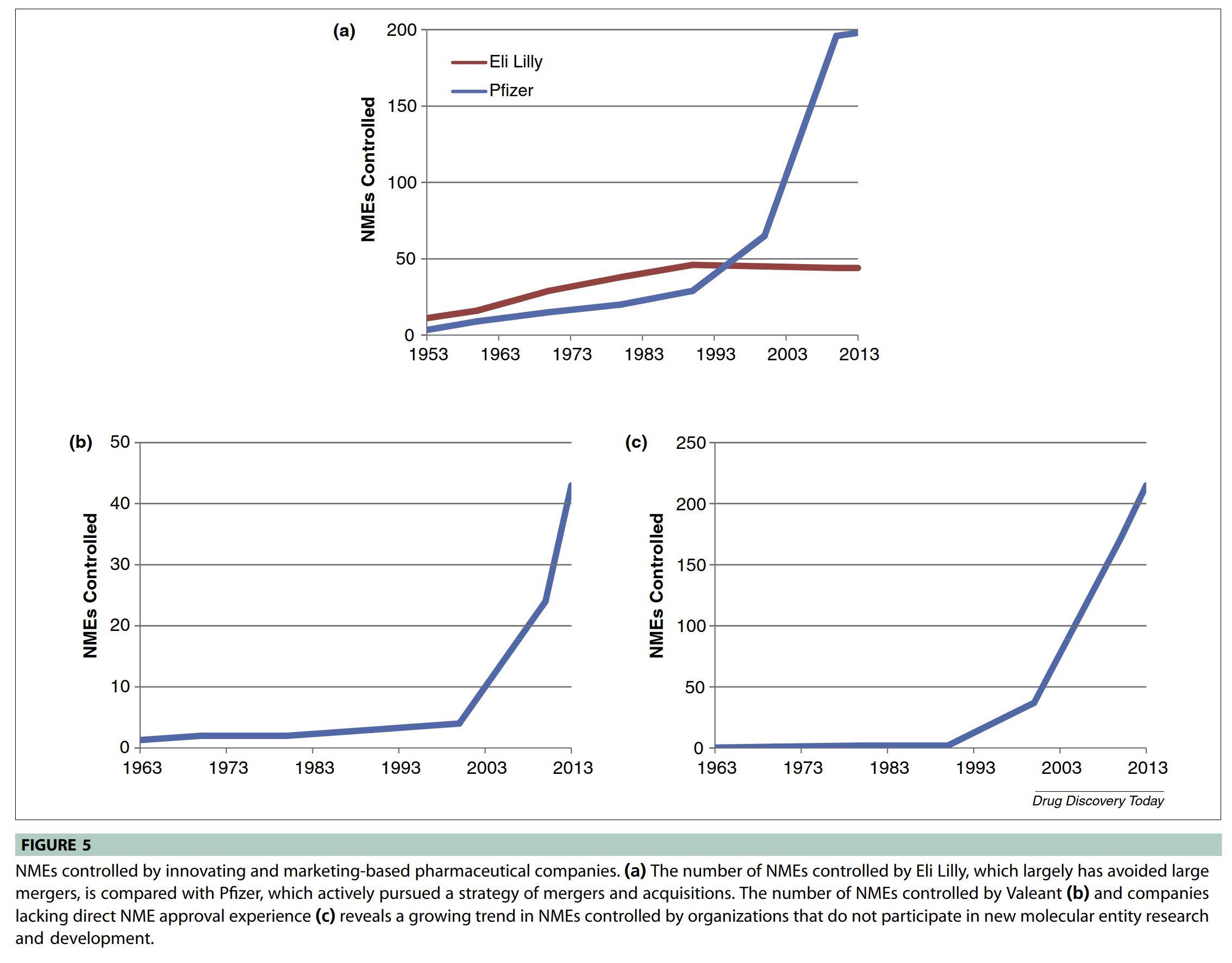

Much of this concentration is due to mergers & acquisitions. Panel 1 shows the rise of company-gobbler Pfizer versus internal developer Eli Lilly. Panels 2 and 3 show NMEs owned by firms that develop none!

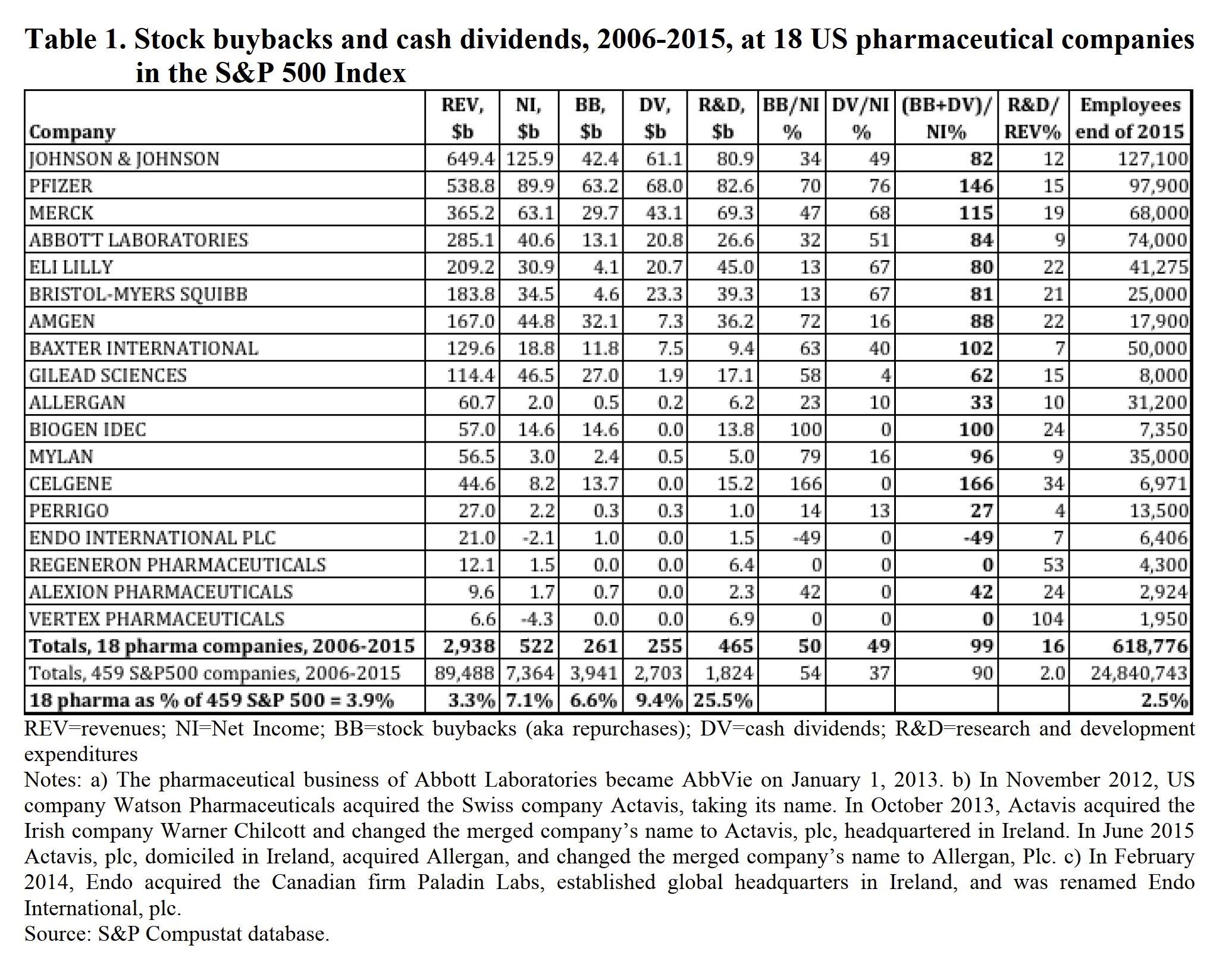

Ever wondered what profit is good for?

Lazonick et. al. show that, in 2006-2015, the 18 U.S. pharmaceutical firms in the S&P500 used 99% of their net income to buy back their own stocks and pay dividends. The number for the rest of the S&P500 was 90%.

Lazonick, William, Matt Hopkins, Ken Jacobson, Mustafa Erdem Sakinç, and Öner Tulum. 2017. US Pharma’s Financialized Business Model. Institute for New Economic Thinking Working Papers (July 13): 1-28.

- This reply was modified 5 years, 1 month ago by Jonathan Nitzan.

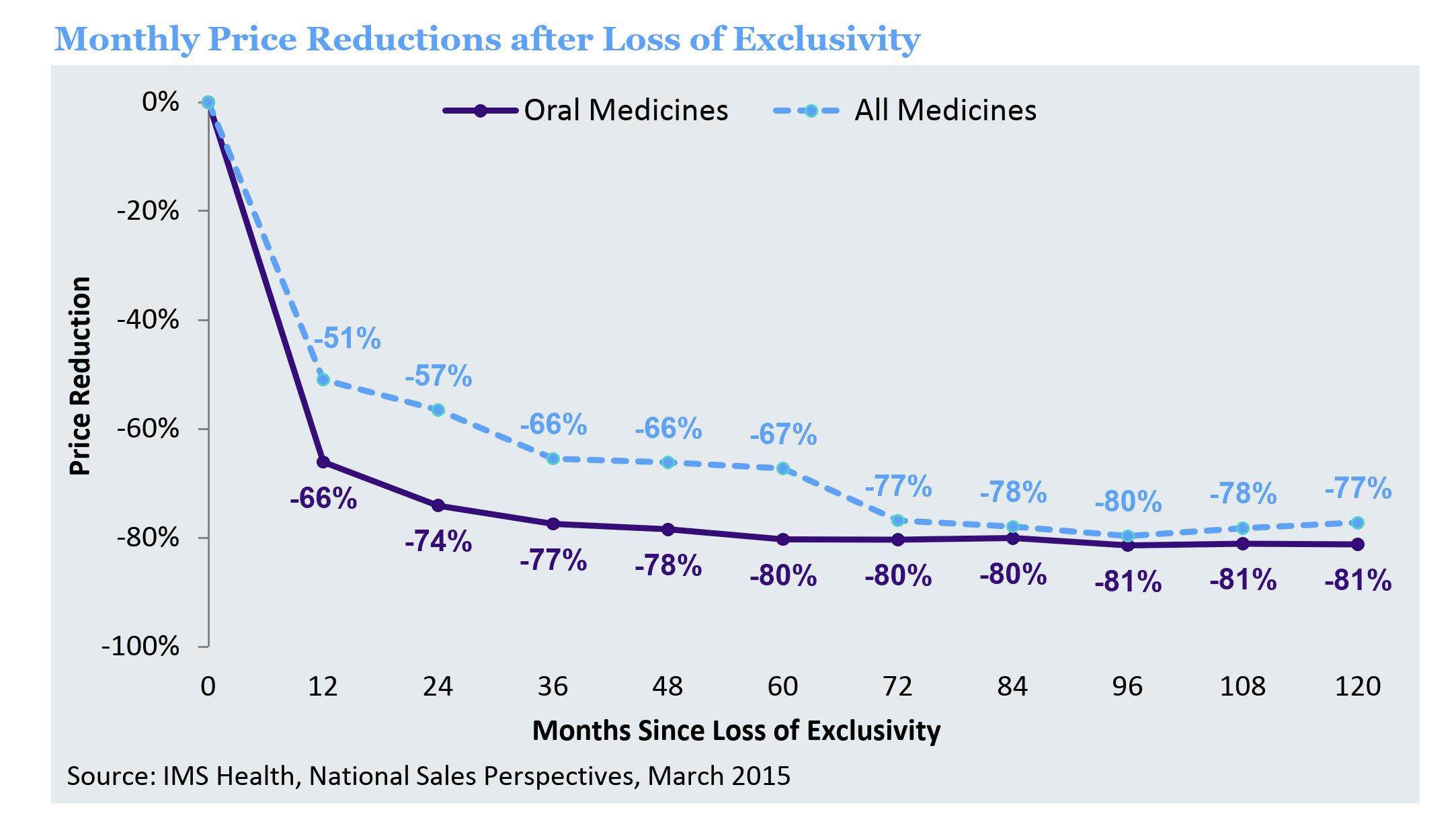

Power? What Power. Pharmaceutical company defenders claim that patent protection helps companies finance their R&D — and, moreover, that protection is temporary: once removed, generic prices drop precipitately.

IMS Institute for Healthcare Informatics. 2016. Price Declines after Branded Medicines Lose Exclusivity in the U.S. January. Parsippany, NJ.

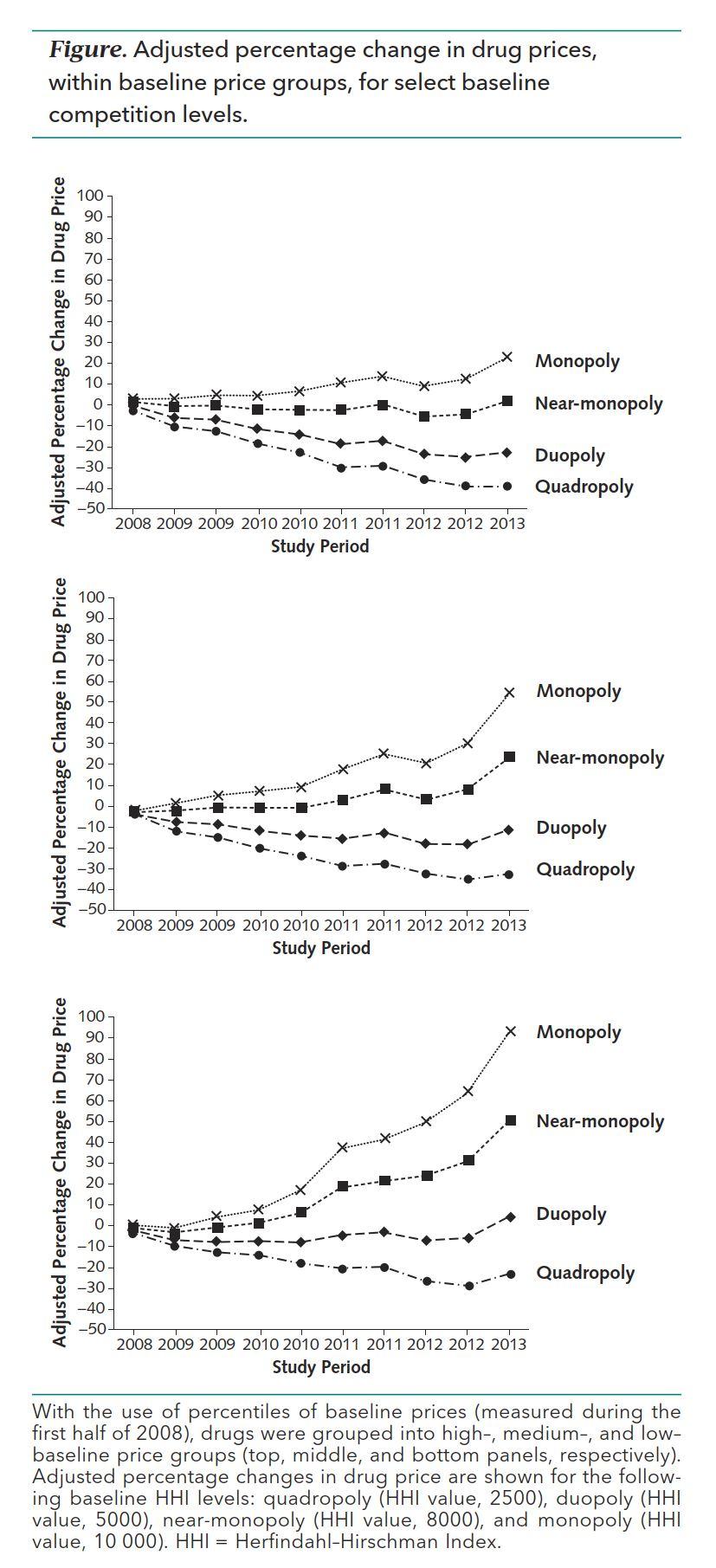

But wait. Generic pharmaceuticals have grown so concentrated, that generic drug prices are rising! In 2008-13, they increased by 30%. In this chart, we see generic price increases for expensive drugs (top panel), medium priced (middle) and cheap (bottom).

Dave, Chintan V., Aaron S. Kesselheim, Erin R. Fox, Peihua Qiu, and Abraham Hatzema. 2017. High Generic Drug Prices and Market Competition. A Retrospective Cohort Study. Annals of Internal Medicine 167 (3): 1-8.

Some thoughts:

1. Can it be said that the deposit/loan creation process or Minsky’s “acceptance” also involve the logic of capitalism – deriving the “present value” of future earnings with a “discount rate” – that capitalization of other assets has (in a sense that, for instance, bankers calculate the profitability of projects or debtors when that make loans?)

The extension of credit is intimately tied with rising capitalization: borrowers (and the lending banks) expect future earnings in excess of the interest and fees they have to repay. If they didn’t, they would not borrow and the bank would not lend.

2. How would or does exactly endogenous money participate in the process of capitalization? We know, as I wrote above, liquidity of capital markets too depends on bank liquidity, but does it just have some indirect effects or does it have some direct involvement in capitalization of assets?

Credit cycles tend to correlate with capitalization cycles (primarily of the stock market). Usually, when market capitalization cycles upward, so does hype, generating more profit expectations and inviting more credit/borrowing to take advantage of these rising expectations. Of course, banks can help fuel/hinder hype, so causality is intertwined.

3. As CasP explains, earnings are a matter of exercising power – “creorder” – across society. How do banks do it exactly?

Banks can and do influence monetary policy, they can raise/reduce their lending rates, toughen/lax lending conditions, advertise/encourage/temp borrowers to take more loans or do the opposite. These are all forms of power.

***

When it comes to the broad trends of credit and capitalization, the conventional separation between banks and and rest of the business sector in not always useful. They are governed by the same power logic.

- This reply was modified 5 years, 1 month ago by Jonathan Nitzan.

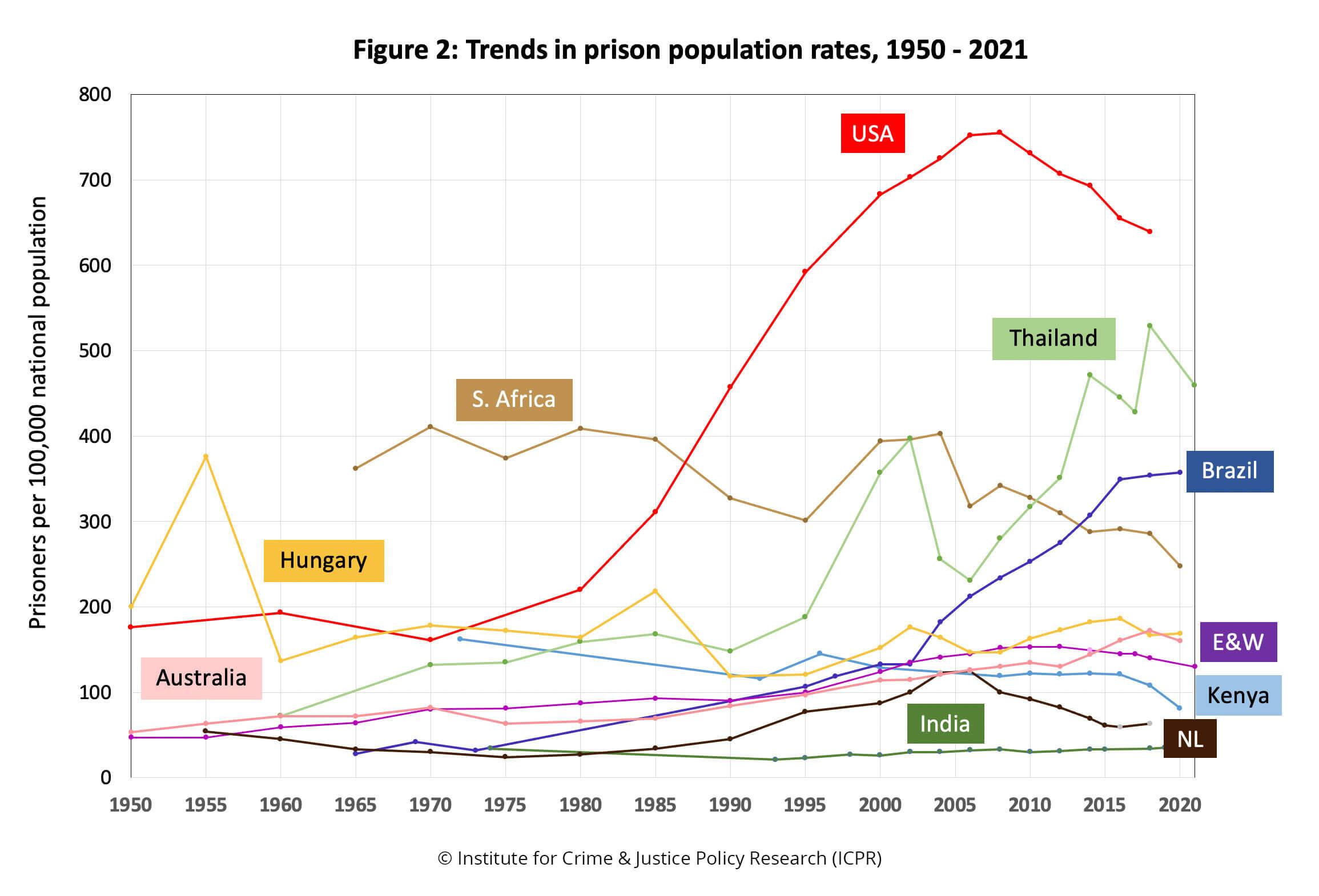

Data waiting for a researcher:

This chart from the WPB shows individual time series for prison population by country. Dividing each series by the the country’s population from the World Development Indicators database gives the incarceration rate. And the incarceration rate can be correlated with income inequality draw from the World Inequality Database.

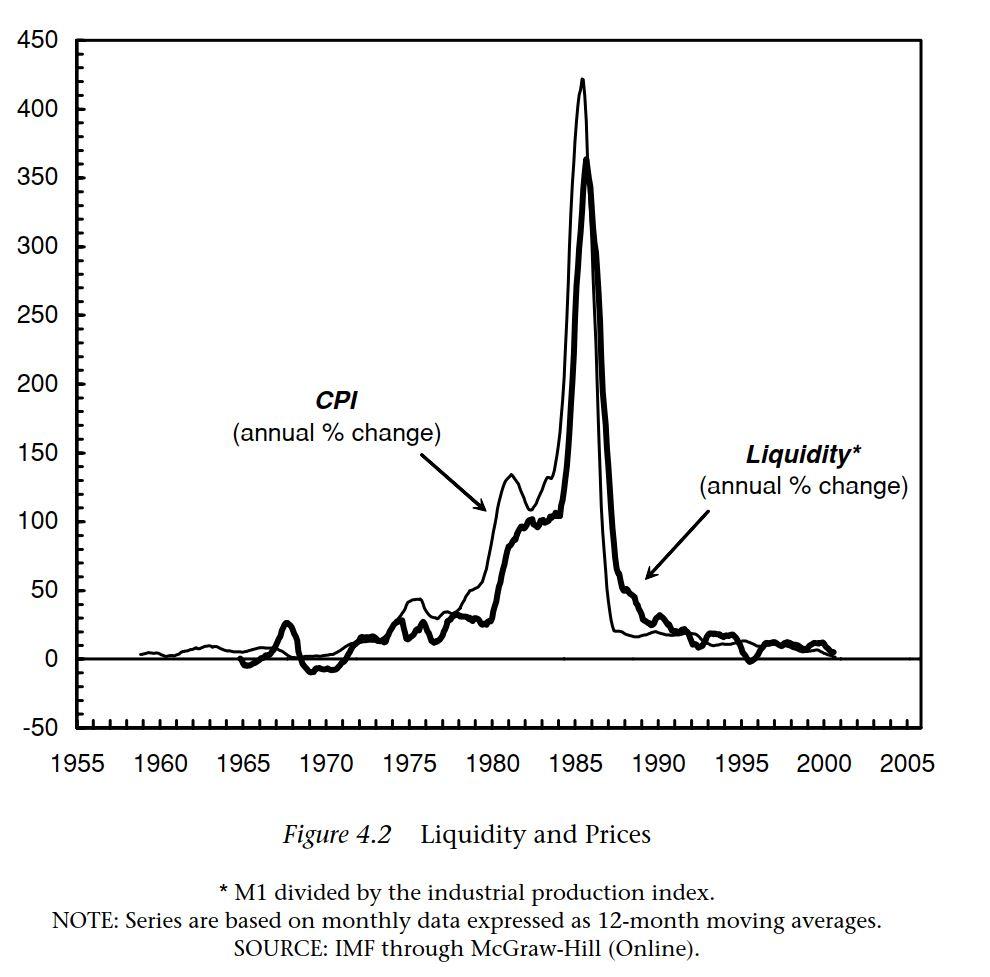

The standard monetarist argument, put in its most simplistic form, is that inflation is driven by rising liquidity (liquidity=money stock/production). But for that argument to hold, the rise in liquidity must come before the increase in inflation.

This graph, taken from our 2002 book The Global Political Economy of Israel, shows it is the other way around: Israeli inflation has led the rise of liquidity!

- This reply was modified 5 years, 1 month ago by Jonathan Nitzan.

- This reply was modified 5 years, 1 month ago by Jonathan Nitzan.

Hi Chris:

1. From power to inflation, or from inflation to power?

In my view, the interesting question is not the effect of power on inflation, but rather what inflation can tell us about power.

From our CasP perspective, modern power is observed as a quantitative relationship between entities. In capitalism, the ultimate manifestation of this relationship is differential capitalization. You can also examine the components of this power, one of which is differential prices (and their rate of change — namely, differential inflation).

From this viewpoint, it makes little sense to say that ‘a lack of workers’ power prevents a rise in future inflation’, simply because nobody knows the future pricing power of workers. Instead, I think it makes more sense to say that the fact that there is currently only limited inflation suggests that workers have limited power and therefore are unable to help fuel it here and now.

2. Absolute versus differential inflation

From our CasP viepoint, inflation is always and everywhere a redistributional process. This means that what matters is not the absolute but relative rates at which prices change. Furthermore, the redistributional patterns of inflation may or may not correlate with its absolute levels. This is something that can be deciphered only through empirical research. (For more, see Inflation as Restructuring.)

3. Do asset prices fuel inflation?

Over the longer haul, higher asset prices need to be ‘validated’ by higher profit (and/or lower risk and normal rates of return), and profit can indeed be increased by inflation. But for that to happen, capitalists must be able to raise their differential prices, and I doubt that this ability is connected to asset prices as such.

4. Does low inflation means more M&A?

In our opinion, the answer is no. In our work, we argued that differential accumulation depends mainly on M&A and stagflation, and that the conditions underlying these two processes are contradictory, so they tend to move counter-cyclically to each other. However, these tentative observations do not mean that there must be either M&A or stagflation. Instead, we simply suggest that at least one of these processes is required for differential accumulation, and that if dominant capital is unable to achieve either, it will end up with no differential accumulation or might suffer differential decumulation.

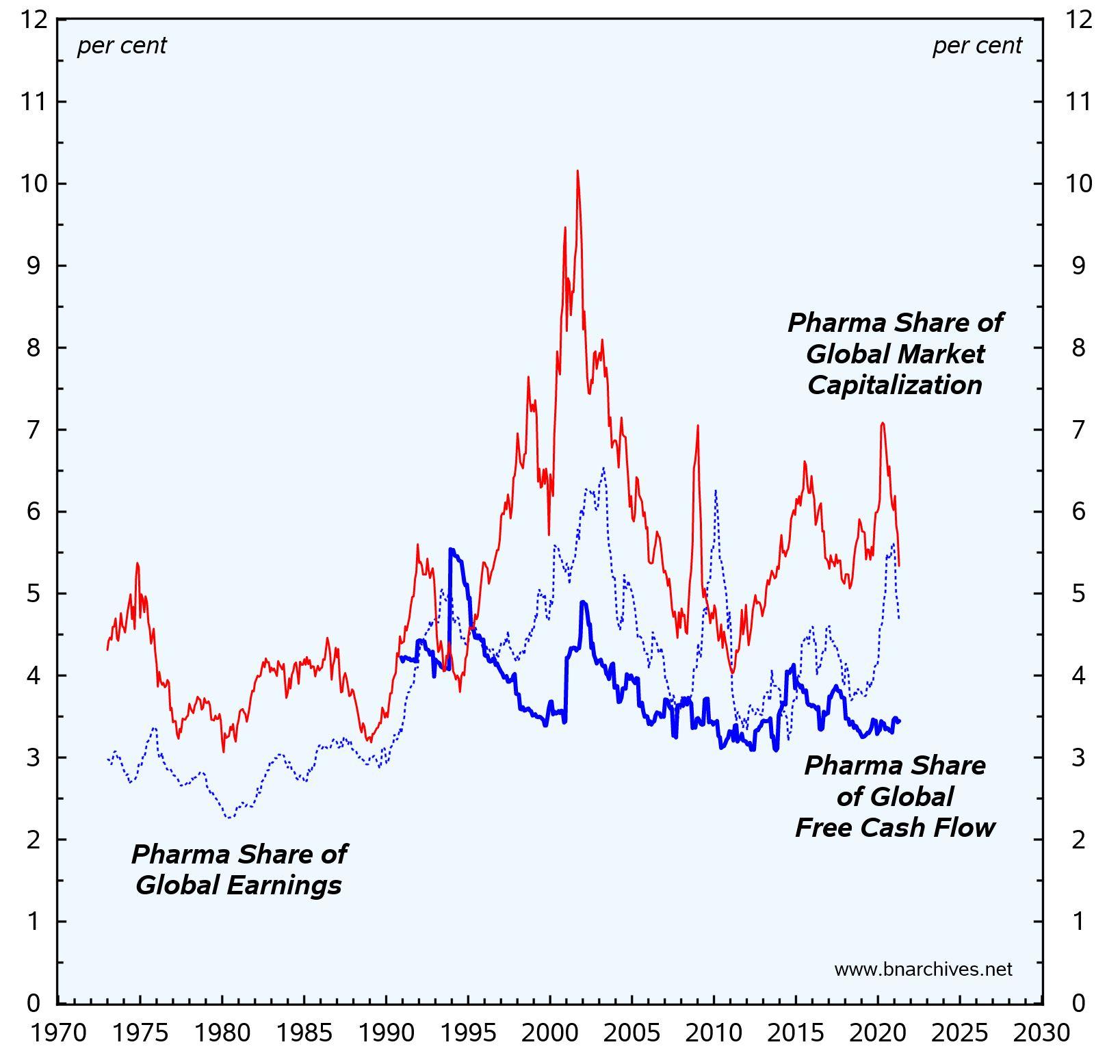

Regarding the ‘free-cash-flow’ argument made in the third footnote of our piece.

To reiterate, the claim against Figure 2 in our research note is that (1) capitalists discount not net earnings, but the free cash flow; and (2) that, in the case of pharmaceutical firms, the relative magnitude of the free cash flow (compared to the average) is higher than the relative magnitude of net earnings (compared to the average).

If the relative magnitudes of the free cash flow and of market capitalization are the same, it follows that capitalists see the future growth of pharmaceutical free cash flow and/or risk as being the same as the average.

But that is not what the data indicate.

Instead, they show that:

1. In terms of magnitudes, the relative shares of market capitalization > net earnings > free cash flow.

2. In terms of trends, the slopes of market capitalization > net earnings > free cash flow.

- This reply was modified 5 years, 1 month ago by Jonathan Nitzan.

From an accounting perspective, there is no way around the fact that capitalists consume their capital goods, they do not accumulate them.

I don’t mean to begin a debate on this issue, just a couple of notes:

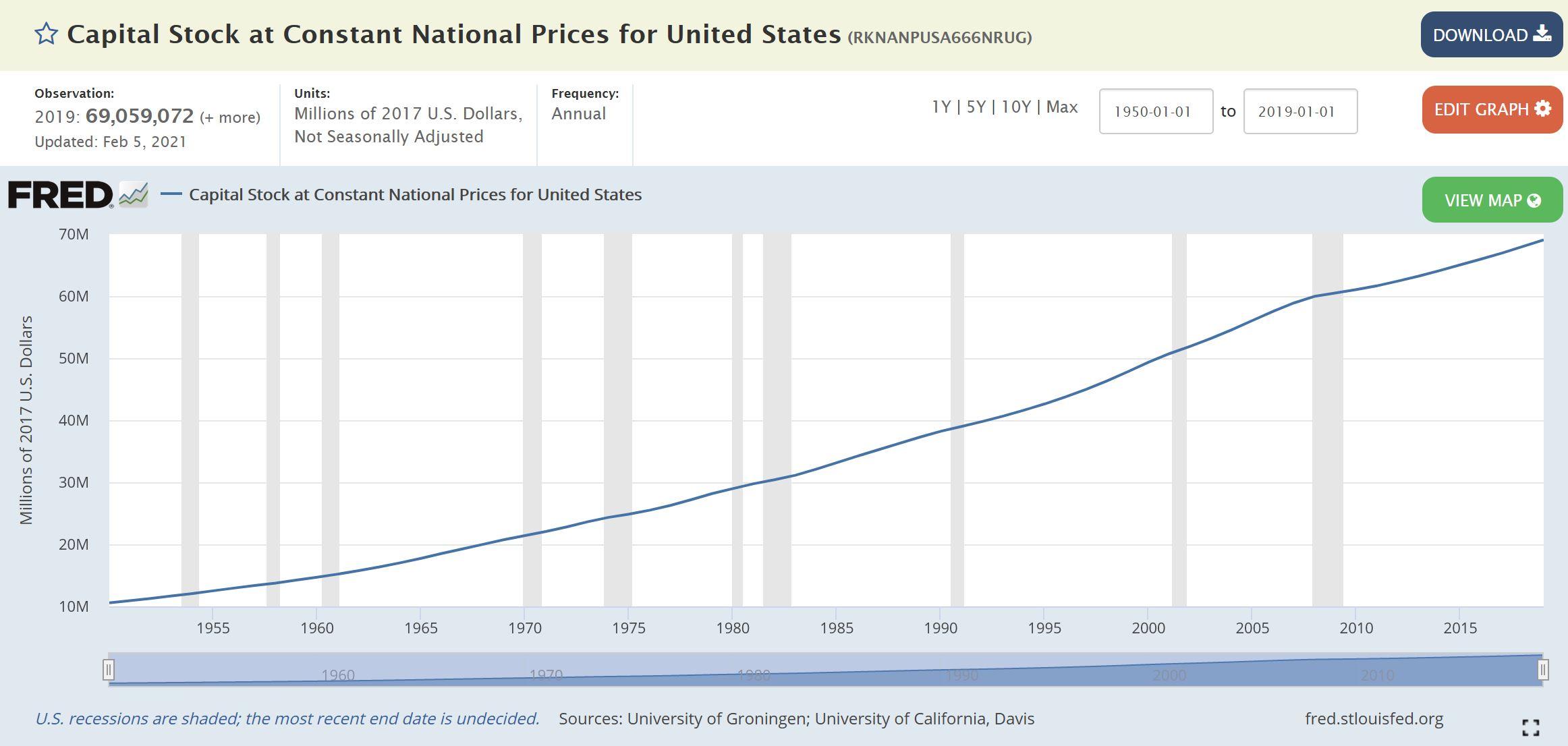

1. I don’t think economists think capitalists accumulate any given capital good. Obviously, individual capital goods depreciate. But in the view of economists, capitalists not only replenish the overall capital stock, they also cause it to grow. For them, one of the key hallmarks of capitalism is a growing physical capital stock, made of an-ever shifting array of capital goods and measured in value-read-money-in-‘constant-prices’ (figure below).

2. One has to distinguish accounting from so-called economic depreciation. Accounting depreciation is determined by accounting rules. So-called economic depreciation is determined, supposedly, by the (productive) value of the capital good. In practice, national accounting statistics measure depreciation differently that company accountants.

- This reply was modified 5 years, 1 month ago by Jonathan Nitzan.

- This reply was modified 5 years, 1 month ago by Jonathan Nitzan.

Capital goods supposedly transfer their value (in utils or SNALT) to the products they create, and, according to the neoclassical view, they even have an additional productivity to boot, so they create more value than their own.

According to economic theory, both Marxists and NC, capitalists do not accumulate this or that item; they accumulate the value embedded in items. The items may change, but value doesn’t. It transmutes itself as it jumps from item to item….

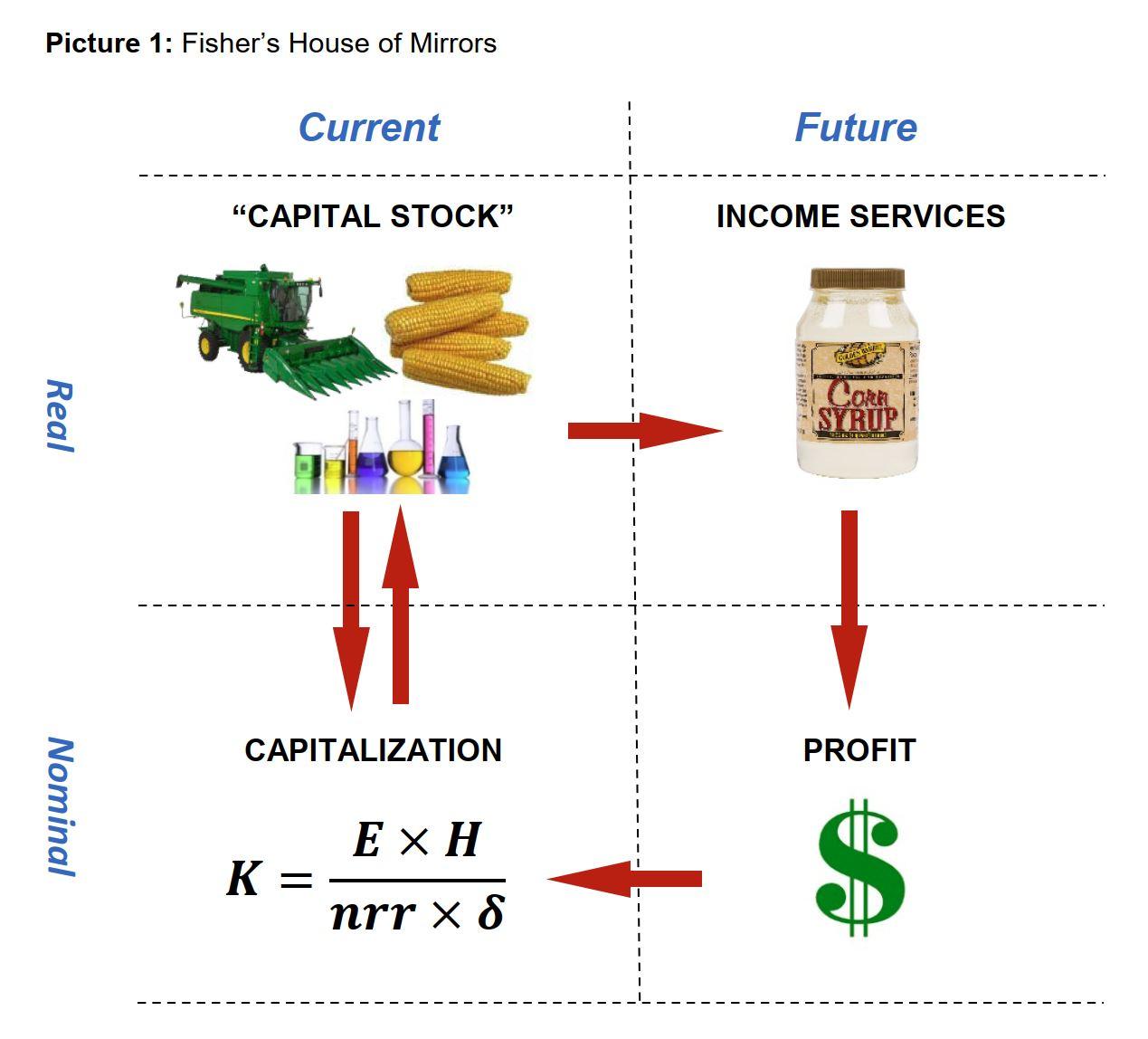

Moreover, according to Irvin Fisher, this view is intimately connected with capitalization:

Fisher, Irving. 1896. What is Capital? The Economic Journal 6 (24, December): 509-534.

Here is a schematic description of his argument:

- This reply was modified 5 years, 2 months ago by Jonathan Nitzan.

Here is a brief research note summarizing our argument on the capitalist outlook:

Bichler, Shimshon, and Jonathan Nitzan. 2021. Pharmaceuticals: Beating the Hell Out of the Average. Research Note (June): 1-5.

More to come.

-

AuthorReplies