Forum Replies Created

-

AuthorReplies

-

Thank you Rowan and Pieter for your interesting interventions.

I believe that the notion that power is both the means and end of accumulation was central to CasP from early on. In fact, it was the motivating force for formulating CasP in the first place.

For a recent articulation, see our 2019 piece, ‘CasP’s “Differential Accumulation” versus Veblen’s “Differential Advantage” (Revised and Expanded).

Scot,

If I understand you correctly, you use r to denote the discount rate, which is distinct from the markup, representing the ratio of profits/revenues.

To me, the discount rate r denotes the rate of return (i.e., the rate at which the entity’s assets grow).

- Do you share this view? If you do, why is your following expression valid: revenues = Cost (1 + r)

- If you don’t share this view, what do you mean by the discount rate?

Scot,

Apologies if I misinterpreted your intention. The truth is that I read your long reply to my 8 points, but found myself lost in its details. I also didn’t see an explicit retraction of you original argument that capitalists determine their profit — but, again, there are many moving parts in your reply, so maybe I didn’t understand it properly.

Instead of answering each of your individual points, let me try to digress our view and suggest how it might differ from yours (as I understand it).

Capitalization is given by:

1. K = expected future earnings / discount rate

The right-hand side of this expression can be decomposed into to 4 elementary particles

2. K = (future earnings * hype) / (normal rate of return * risk)

Power-driven capitalists try to augment their differential capitalization (marked by the .d extension) (Note that, because the normal rate is common, its differential value normalizes to 1 and drops from the equation.):

3. K.d = (future earnings.d * hype.d) / risk.d

***

POINT 1. When Eq. 3 is applied to a capitalized entity or group of entities, every element in it represents a distinct aspect of the power of that entity: the future earnings it will receive relative to those of the benchmark, the hype it can create relative to the benchmark, and the risk it can keep low relative to the benchmark, all contribute to its overall capitalized power relative to the benchmark.

From this viewpoint, the differential discount rate (which reduces to differential risk in this formulation) is distinct from differential future earnings and differential hype and therefore has to be treated as only one aspect of power. This conclusion differs from your notion, as I understand it, that, because pricing supposedly relies on discounting, all power can be reduced to the discount rate.

POINT 2. In our view, none of these elementary particles is set exclusively by the entity owners themselves. Instead, these particles are determined by the power conflicts in which the entity is embedded and on which it acts. Thus, differential future earnings, even if greatly influenced by the differential power of the entity, are meaningful only as a conflictual relation with the power of other entities and processes who boost/reduce it (including workers, governments, customers, criminals, culture, wars, etc.). Similarly with differential hype and differential risk, which the entity can alter in one direction but others can change in another.

The result is that capitalized power — which we understand as the quantitative differential representation of many qualitatively different conflicts — is not a top-down dictate of the powerful, but an ever-changing culmination of an ongoing conflict that spans society at large. Capitalists and the entities they own are at the top of the capitalized hierarchy, but their position in that hierarchy as well as the very structure of that hierarchy are constantly changing because power always invites and is exercised against opposition (Ulf Martin’s autocatalytic sprwal).

POINT 3. These considerations might serve to explain why CasP puts so much emphasis on theoretically informed empirical research. Without such research, we cannot decipher — and simplify — the complex trajectories of differential capitalization nor understand the underlying qualitatively different processes that drive those trajectories. Without this deciphering and understanding, our equations and theories remain empty shells at best and misleading corps at worst.

Scot,

I think the issue here is not only whether we can write the equations correctly (which often we don’t), but also – and perhaps more so — whether the equations justify our conclusions.

You write that:

In a world where the capitalist uses the capitalization equation to set what it will pay for input costs such as wages by discounting its expected profits from future sales, the discount rate used by the capitalist determines (and ensures) the capitalist’s profits.

I think this interpretation is fundamentally wrong.

In and of themselves, capitalist expectations of profit, the ex-ante discount rate used to concoct these expectations, and the impact these expectations have on how much they spend on inputs, do not and cannot determine, let alone ensure, actual profits.

It seems to me that your claim here is not only unrealistic, but also self-contradictory.

Imagine every potential capitalist expecting his/her own profit into existence. This mana-from-heaven magic will make everyone an instant, insatiated capitalist, bring their individual expectations into conflict with each other, and pretty much ascertain that their actual profits will differ from what they expect.

In my view, discounted values do not generate power. Instead, it is power that generates discounted values.

But we can agree to disagree.

In a world where the capitalist uses the capitalization equation to set what it will pay for input costs such as wages by discounting its expected profits from future sales, the discount rate used by the capitalist determines (and ensures) the capitalist’s profits. See equation 6, below.

Scot,

That’s a clever way of presenting your point, but I don’t think the point itself is correct.

1. What capitalists agree to pay workers certainly depends on their profit expectations, but this dependency is not what your equations express.

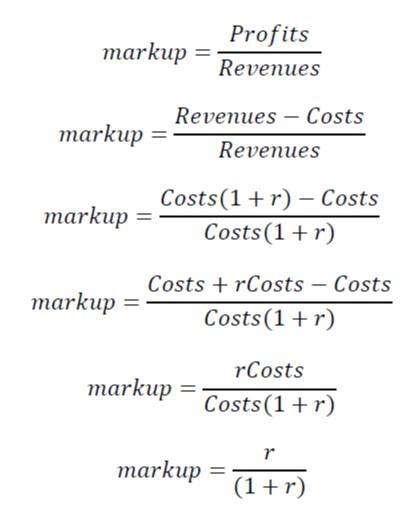

2. The discount rate is what investors use to capitalize expected future profits. In your equations, though, r is not the discount rate (the rate of growth of capitalization), but the profit markup over costs (assuming all costs can be expressed as wages).

3. Moreover, the way you express it, r reflects not the intended markup, but the realized one.

4. The realized markup – and therefore actual future profit — is neither at the capitalist’s discretion nor knowable beforehand. It depends on how much capitalists will be able to sell in the future, which is anybody’s guess (and the reason why profit forecasters are almost always wrong).

5. Since capitalists don’t know their actual future profit, they cannot set current wages as a function of that profit.

6. By definition, the wage bill is the product of the wage rate and the level of employment. In general, capitalists control the level of employment — but, in my view, they don’t set the wage rate, which is the result of historical conditions and an ongoing, complex power conflict within the firm and across society. Expected (though not actual) future profit is merely one element of this conflict.

7. For Kalecki, the markup reflects capitalist power. But this reflection is ex post, not ex ante. The discount rate, by contrast, is set ex ante, not ex post. I think it is erroneous to treat them as if they were the same.

8. Perhaps it will be useful to try to express your equations in ex-ante terms (rather than ex post), using the discount rate (rather than the markup).

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

“power is confidence in setting the discount rate,” or, more simply “power is the ability to set the discount rate.”

1. I think we need to distinguish between individuals and groups who determine the discount rates they apply when trying to price expected future earnings (me, Elon Musk, JPMorgan Chase) and the average discount rate prevailing in society. If we take the individual perspective, my power is the same as Musk’s and JPMC, since all of us are free to set our own discount rates as we see fit. If we take the average perspective, then there is no singular entity or group to associate this power with, since the average discount rate is determined by the shifting structures of capitalism.

2. By saying that power is simply ‘the ability to set the discount rate’, you seem to imply that the power of any given entity — me, Musk, JPMorgan Chase — is independent of its (expected) profit. Do you really mean that?

Thank you, James. The 602-page doorstopper is on its way to the bookstores, though, for some reason, the publisher’s book page isn’t up yet.

The book presents and situates CasP theory and research — our own as well as that of others — within the broader evolution of political economy. Some of this material has already appeared in English, but much of it hasn’t, so a translation would be nice. Whether we will do it is another matter….

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

In his interesting 2010 book, Misplaced Generosity. Extraordinary Profits in Alberta’s Oil and Gas Industry (Edmonton, Alberta: Parkland Institute, University of Alberta), Reagan Boychuk offers an account of Alberta’s oil and gas revenues, costs and profit, plus imputations of ‘normal’ and ‘excess profit’. (Twitter thread)

The computations/imputations are built from the bottom up – i.e., they are based on estimates of the industry’s output, average oil/gas selling prices and investment and production cost, so, on the face of it, they reflect the business performance of Alberta’s oil and gas industry — and nothing else.

But here is a question: output levels are collected at the provincial levels, as are selling prices (I assume). But capital and operating costs probably come from the companies themselves, and since these companies are often large transnationals rather than Albertan only, it is hard to know the extent to which their data reflect local operations ‘uncontaminated’ by transfer pricing.

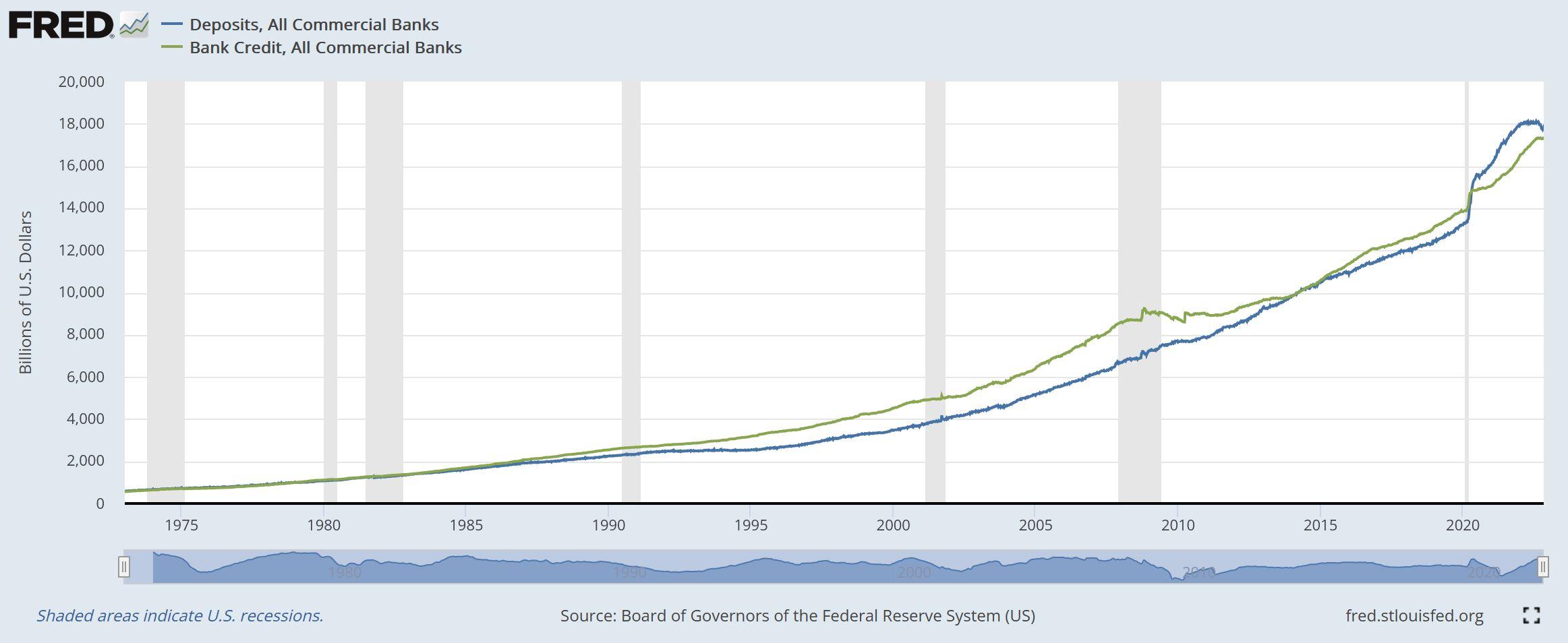

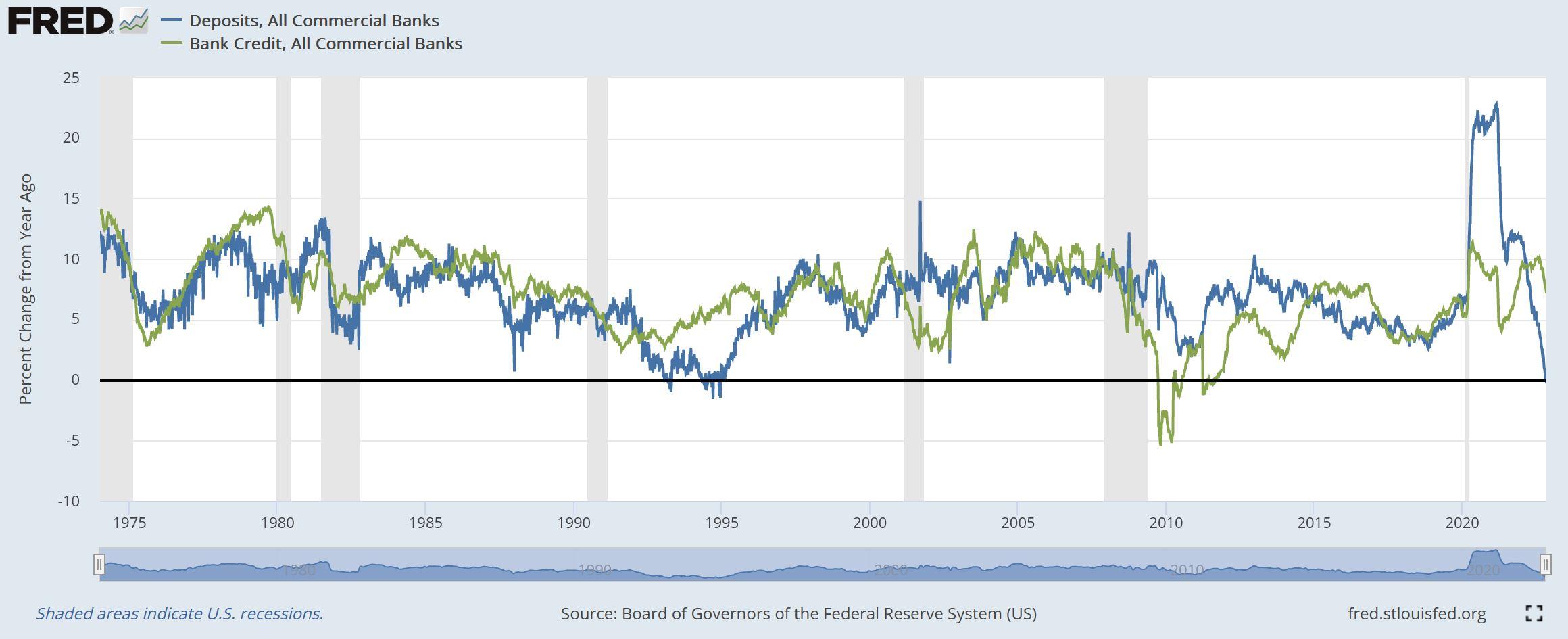

Regarding my point (2) above, here are the weekly data for deposits and credit in the U.S. banking system — first in levels ($bn) and then in annual rates of change (%).

Loans and deposits do move in tandem.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

Conceputally, NIPA profits are attributed to ‘industries’, so ostensibly you can select the sectors that produce ‘capital goods’ and aggregate their profits.

Practically, though, NIPA profits are derived from corporate reports, and since many corporations today operate in more than one sector (and often in many), it is difficult if not impossible to know what profits come from what sector.

As far as I know, the national accounting rule of thumb is to attribute the company’s entire profit to the sector that generates most of its sales, but if this largest sector accounts for only 20% or 30% of the corporation’s operations, the results can be very misleading.

November 10, 2022 at 7:48 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #248575November 10, 2022 at 1:01 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #248571Thank you for both posts, Scot.

In our book Capital as Power, we describe the ever-growing terrain of capitalization:

Nowadays, every expected income stream is a fair candidate for capitalization. And since income streams are generated by social entities, processes, organizations and institutions, we end up with the ‘capitalization of every thing’. Capitalists routinely discount human life, including its genetic code and social habits; they discount organized institutions from education and entertainment to religion and the law; they discount voluntary social networks; they discount urban violence, civil war and international conflict; they even discount the environmental future of humanity. Nothing seems to escape the piercing eye of capitalization: if it generates earning expectations it must have a price, and the algorithm that gives future earnings a price is capitalization. (158)

Extrapolating the foregoing illustrations, we can say that in capitalism most social processes are capitalized, directly or indirectly. Every process – whether focused on the individual, societal or ecological levels – impacts the level and pattern of capitalist earnings. And when earnings get capitalized, the processes that underlie them get integrated into the numerical architecture of capital. Moreover, no matter how varied the underlying processes, their integration is always uniform: capitalization, by its very nature, converts and reduces qualitatively different aspects of social life into universal quantities of money prices. In this way, individual ‘preferences’ and the human genome, the structure of persuasion and the use of force, the legal structure and the social impact of the environment – are qualitatively incomparable yet quantitatively comparable. The capitalist nomos gives every one of them a present value denominated in dollars and cents, and prices are always commensurate. (166)

With this being said, I think we need to distinguish ‘actual capitalization’ from ‘as-if capitalization’.

As Ulf Martin explains, capitalization is an ‘operational symbol’ – namely, a symbol that does not simply represent the reality, but explicitly defines and creates it in the first place. And, to me, this feature suggests that for something to be labeled capitalization, it needs to be consciously articulated as such.

In this context, we can think of ‘actual capitalization’ as one that the capitalizer explicitly spells out; as-if capitalization as one that the outside observer-theorist imposes; and in-between cases as weighed by their proximity to either pole.

A wage payment in this scheme is actual capitalization if the capitalists and workers involved calculate it as such, but it is only as-if capitalization if the idea is merely imposed by the outside observer-theorist.

And in my opinion, the same goes for discoveries of ‘ancient capitalization’: unless we can demonstrate that the price was consciously or at least explicitly articulated by the price setter as the discounting of expected further earnings, it remains a retrospective, as-if imposition.

***

Martin, Ulf. 2019. The Autocatalytic Sprawl of Pseudorational Mastery. Review of Capital as Power 1 (4, May): 1-30.

What does the harnessing of matter and energy tell us about the history of humanity?

1. Consider the following chart, taken for our paper ‘Growing Through Sabotage’, and assume that the numbers it shows are correct. Do these numbers tell us anything about the social formations of families, tribes, chieftainships and states? About slavery, feudalism, capitalism, socialism and fascism? About where society is likely to be on the spectrum between direct democracy and tyranny? Energy and matter create an ‘envelope of the possible’: the more energy and matter being converted, the more energy and matter are available for use. But the quantities that end up being used and the purpose for which they are used remain open-ended.

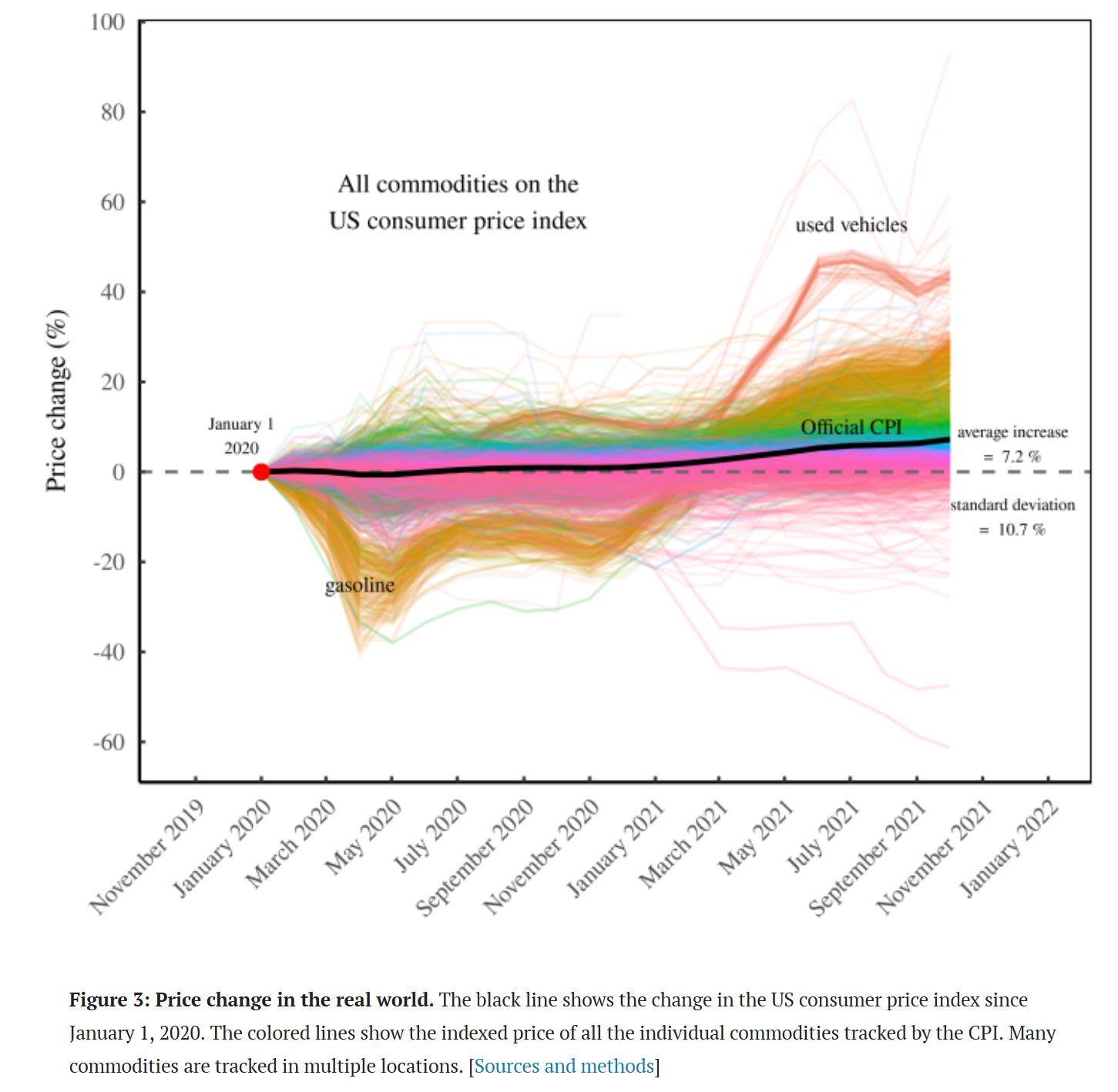

2. In capitalism, the important quantities are not material/energetic, but pecuniary, and pecuniary magnitudes are the product of both quantities and price. This fact means that, with different prices, the same material/energetic quantity can give rise to different pecuniary magnitudes (see the enclosed chart from Blair Fix’s paper, ‘The Truth About Inflation’, showing the range of price changes associated with a given rate of inflation). And since relative prices are a matter of power, so are the pecuniary magnitudes they give rise to.

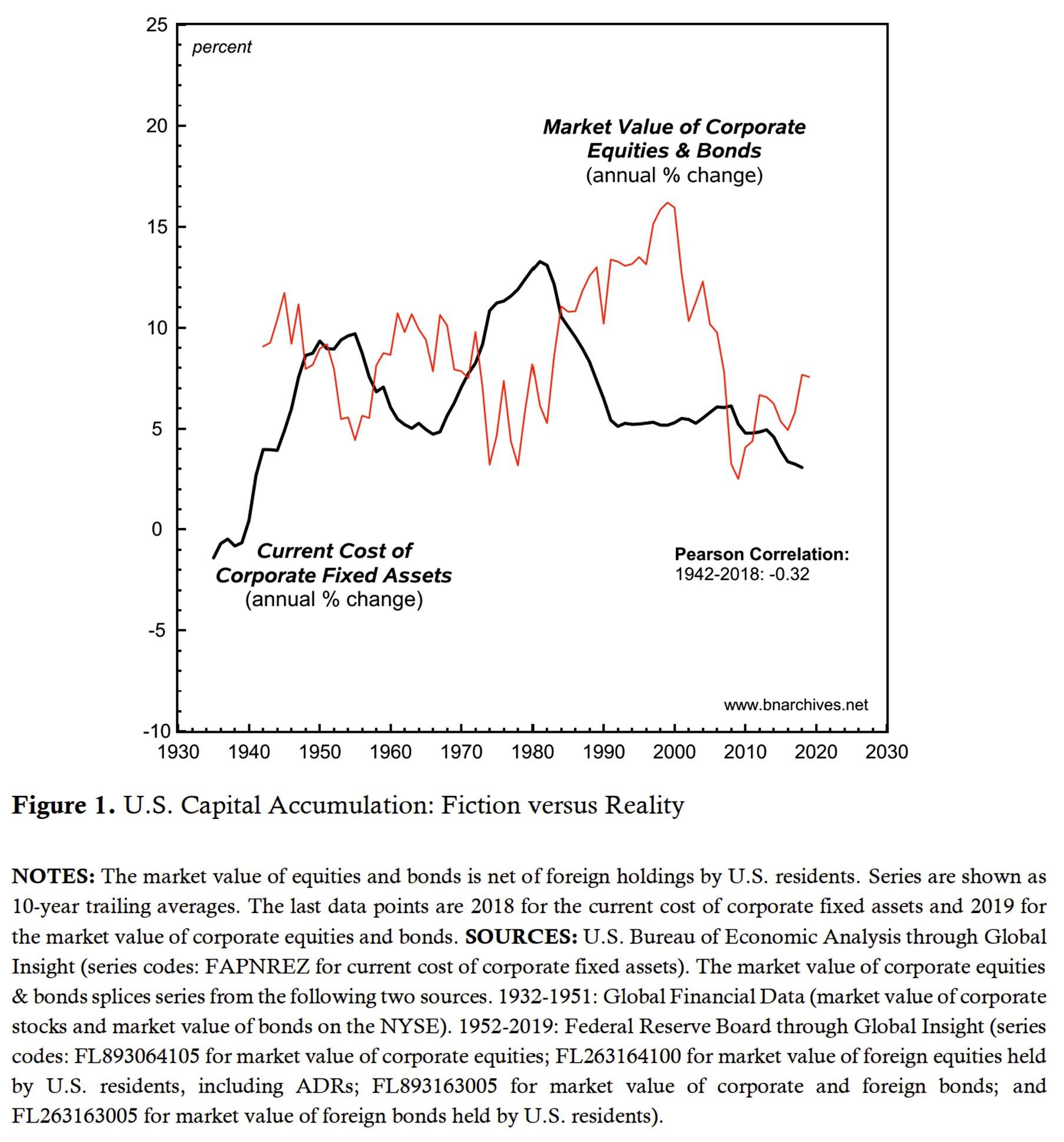

3. On its own, the fact that capitalism creates more backward-looking ‘capital goods’ counted in terms of energy/matter/labour time tells us little about the forward-looking accumulation of ‘capital’ which discounts risk adjusted expected future earnings (not to speak about their differential magnitudes). The chart below, taken from our rejected interview, ‘The Capital as Power Approach’, shows that, in the United States, the growth of these two magnitudes are inversely correlated. In other words, the two ‘accumulations’ — the one dear to economists and the other that matters to capitalists — are opposite in their direction, and labelling the former ‘real’ and the latter ‘fictitious’ does nothing to make this problem go away.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

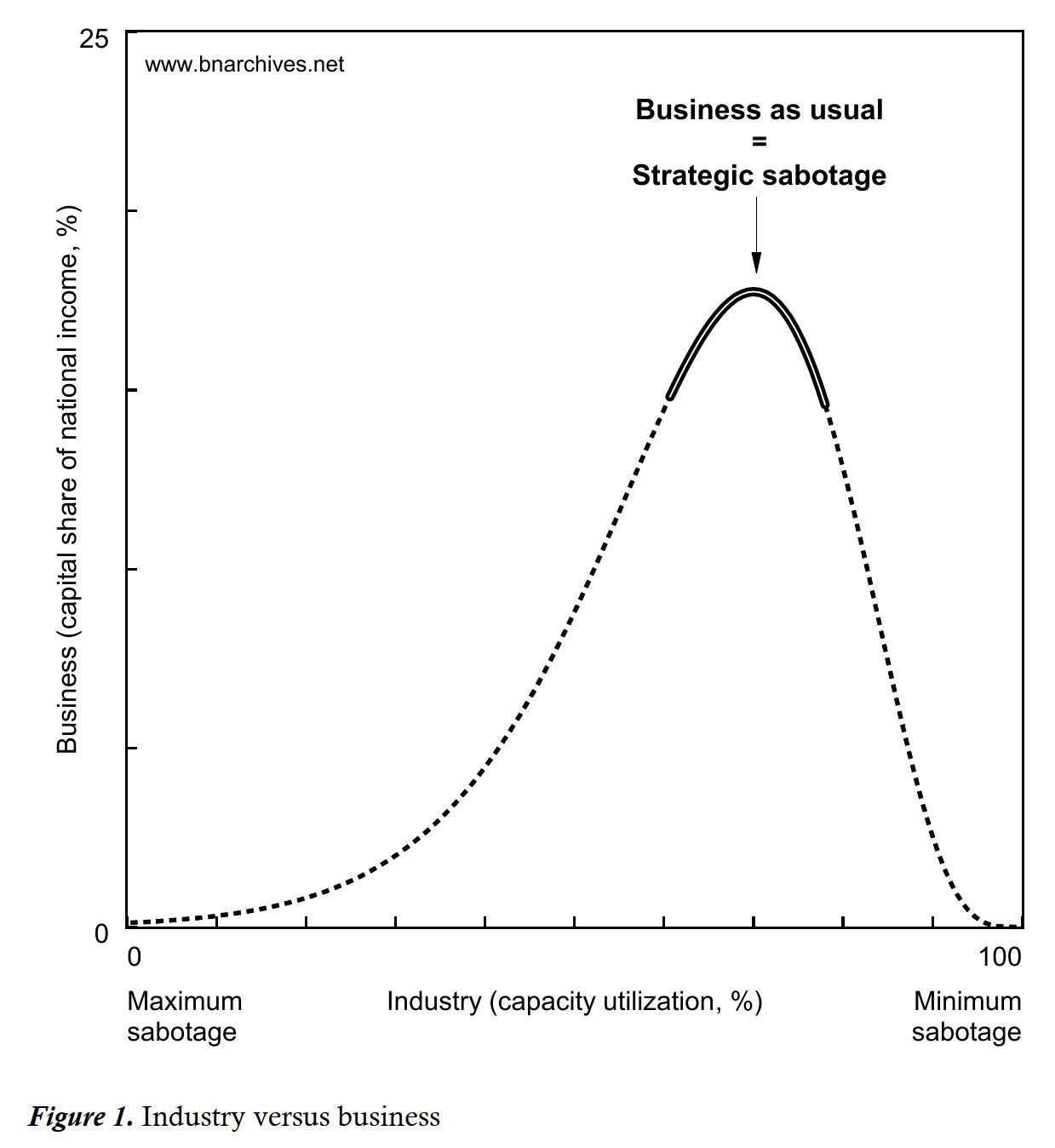

(1) Let’s tell a simple parable. In this parable there are two separate groups of 100 people each, called ‘industry’ and ‘business’.

(2) Industry is characterized by two features: (1) its members deliberate/cooperate/act autonomously and democratically to determine both their goals and the most effective ways and means of achieving those goals; and (2) their goals concern not only their output, but also — if not more so — the very processes of producing this output and developing themselves and the institutions that participate in this production.

(3) The purpose of the business group is to control industry and use this control to extract income from it. The effect of business on industry can be positive, nil or negative. However, if the impact is positive, and if industry endorses and applies it, then business is no longer separate from industry, but part and parcel of it. And since business becomes part of industry and no longer controls it, it cannot extract any income from it. By contrast, if the effect of business on industry is nil or negative, industry — assuming it is autonomous – is likely to reject it. In this case, the only way for business to have the last say, is by enforcing this impact – i.e., by ‘sabotaging’ industry.

(4) If we accept this parable as a way of thinking about actual capitalism, it follows that the industry-business distinction holds only when business sabotages industry. And this condition means that the only thing that business can do is calibrate the nature and intensity of industrial activity by setting sabotage somewhere between none (full industrial capacity shown the rightmost point on Figure 1) and total (zero industrial capacity shown by the leftmost point in Figure 1). According to our parable, though, this calibration contributes nothing to industry; it merely allows it greater or lesser freedom to act in the best the interest of humanity.

(5) And now to your question, Corentin:

[W]hat are advertisements, fashion, sales representatives, etc. for if not to forge new needs and stimulate consumption, hence industry?

Our answer: advertisement, fashion, sales representatives, etc. contribute not to industry, but to the business control of industry. An autonomous society decides for itself, democratically, what to do and how. It has no need for business stimulation, advertisement and the creation of ‘new needs’. If we are ever to see such society emerging, it will likely move away from the sabotage that business relentlessly imposes and glorifies (private transportation, urban sprawl, fast food, conspicuous consumption, brainwashing, poisonous production, etc.), as well as scale back the enormous waste of sustaining and fortifying the power hierarchies that business uses to control us all.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

November 2, 2022 at 8:06 am in reply to: Is Exchange Value Really Just Capitalized Use Value? #248518Bagnall’s text is intended for the specialist, and I find it really hard to follow. I do understand, though, that:

1. The discussion involves fragmented ancient evidence that the experts piece together, fill the in-between blanks and then interpret the results as if they were modern financial transactions.

2. The transactions involved aren’t purely monetary, but hybrids of money and ‘in-kind’ flows. This mix means that even when the transactions are clearly stated — and most aren’t — their underlying magnitudes are only partly specified:

We can now summarize the types of transactions involved in the Tetoueis documents and the new Berlin text: (1) loans in kind to be repaid in kind with interest of 50 per cent ;20 (2) loans in money to be repaid in kind, with both amounts specified but not the interest; (3) loans in money, amount specified, to be repaid in kind at a price not specified but reduced by a third; (4) loans in money, with amount not specified, to be repaid with a fixed amount of produce. (Bagnall: 93)

With this in mind, interpreting the ‘pricing’ of these contracts as if they were acts of capitalization, however embryonic, seems to me far fetched.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

-

AuthorReplies