Forum Replies Created

-

AuthorReplies

-

This is the reason I wonder if there are some key texts you could name as central in building your understanding to the point that CasP became conceivable, derivable to yourself and Shimshon Bichler?

The books that have influenced us are referred to in our works, but I don’t think the ‘secret’ is in what you read: from our experience, the pivot is actual research. It is research that raises the simple questions that nobody seemed to have raised before, that leads you to question what the experts believe, that opens your horizons to totally new spaces, entities and processes. And it is research that directs you to search for forgotten writings and helps you weave them into a new understanding of the world.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

Thank you Rowan.

“… a notion of capital as capitalization & capitalization the product of a power relations makes it by definition nondeterministic & contingent, I think, in ways old capital theories wouldn’t have been. Which is to B&N’s credit, but to the detriment of “capital theory” as a project.”

Neoclassical theory and its economic offshoots are ‘deterministic’ only on paper. In practice, their inner arguments cannot be operationalized (utility and util-denominated productivity are mirages) and their indirect ‘testing’ almost always fails (generating a multiples ‘measures of ignorance’ compensated for by an even greater number of ‘distortions’).

CasP’s argues that the trajectory of capitalist societies reflects the capitalist creordering of power against opposition. The capitalist attempt to creorder society, being subjugated to the ritual of differential capitalization, is relatively simple to articulate and often possible to predict. Resistance to this creordering, however, can be open-ended, which makes it difficult to map and anticipate. One way or the other, the resulting clash between these two moments is complex and non-linear, which means that we can only say so much about its immediate results and even less about its future outcomes.

With this limitations in mind, CasP research has managed to map a growing number of historical power patterns related to stagflation, M&As, energy use and hierarchy, wars, societal U-turns, military spending, risk reduction, popular culture, sabotage, consumption, debt, high-technology, etc. And what’s more, it demonstrated that some of these patterns continue to hold beyond the time period for which they were originally mapped and theorized. Not bad for a non-deterministic science of society.

My feeling about CasP is that it remains on-track but an incomplete project.

The idea that capital is power and that capitalism is a mode of power is just a theoretical shell. It has to be concretized, and this process has barely begun.

[CasP] theory is difficult. When empirically supported theory is complex and difficult the public prefer a simple lie. This is one reason why capitalism works so well. “Supply and demand” is repeated like a catechism: a self-evident truth to everyone.

The theory of demand and supply may be based on a lie, but it’s anything but simple. Most economics students don’t really understand it, and most non-economists cannot decipher a single paragraph of a neoclassical paper. By comparison, CasP is readily accessible and can be understood by any intelligent person who puts her/his mind to it.

The reason why neoclassicism reigns and CasP ignored has to do with the monopoly economists hold over all things ‘economic’, not the simplicity of their arguments.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

October 13, 2022 at 7:07 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #248446Thank you Scot.

I read Chapter 2 in Tan’s book, ‘The Use and Abuse of Tax Farming’, and found it really interesting. What I didn’t find, though, is any evidence that tax farmers discounted future earnings — in Rome and elsewhere.

In your post, you write that

Tax farmers kept all taxes/tithes they recovered, and it turns out that tax farm contracts were extremely profitable, so one would think there was some form of discounting (capitalization) going on.

Well, from Ch. 2 in Tan’s book it seems that historians of tax farming know relatively little, if anything, about the profitability of tax farmers. One guesstimate puts the rate of profit of Roman publicani in a certain region between 8-215%, while another speculates it was 30% (pp. 57-8). But no one really knows.

Similarly, judging by this chapter, nobody knows what calculations contract bidding was based on. The chapter does not mention discounting/capitalization of future earnings, let alone offers any evidence that such discounting/capitalization took place.

Reading between Tan’s lines, my impression (again, nobody really knows) is that contract bidding was largely a matter of arms wrestling. When the tax farmers overcame their mutual disdain and acted in unison, prices were low and they could make a bundle; when they bickered, prices were high and they earned little or even lost (and sometimes demanded retroactive rebates, no less). There was no need for any risk coefficients and raising the normal rate of return to the power of five. It was simply a matter of strongmen groping for what the ‘Republic will bear’.

This isn’t an area I know enough about, and there may be other studies where discounting of tax farming is discussed and assessed. But without such evidence, the claim that these contracts reflected discounting seems to me unsubstantiated.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

October 12, 2022 at 3:57 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #248441Let’s leave Sumer aside.

Did capitalization — not interest or other future payments, which, on their own do not imply capitalization — start in Ancient Athens and the Roman Republic? Is this where the 13-14th Century European burgers picked the idea from?

That would be an interesting study to read.

October 12, 2022 at 6:04 am in reply to: Is Exchange Value Really Just Capitalized Use Value? #248436It seems to me that, with a sufficiently large sample, writing is a good indication for thinking.

Modern financial textbooks and highly-paid forecasters tell the future by combining expected earnings, assessments of risk and notions of normality. And the fact that capitalists bet on these written forecasts with their money suggests they do believe in what they pay for. Of course, these expensive forecasts, pronounced with stern faces and associated probabilities and aggregated into fancy publications such as consensus forecasts, are almost always wrong. But the reason they are wrong, claim the forecasters, is not that the future is unknowable, but that human beings refuse to obey the rational scriptures and end up walking randomly. But not to worry. There is now a new, innovative profession, formalized by straight-face behavioural financiers, that is busy predicting the external irrationality of us mortals in order to make the future whole again (think Ulf Martin’s autocatalytic sprawl).

Of course, we can never know for sure, but it seems to me that the ontology of the Sumerians, whose gods created humans to be their slaves, whose Anu was supreme authority and Enlil turbulence at will, whose ironclad rate of interest was religiously sanctified, and whose military conflicts were won and lost by competing gods, was very different.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

October 11, 2022 at 7:26 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #248429One of my graduate students in ‘Seven Lectures on Capital’, a course I taught at the Economics Department in Tel Aviv University many years ago, told me that “paleolithic individuals” (his term), just like present-day utility hunters at the shopping mall, made choices by subjecting their indifference maps to budget constraints. I kid you not.

Or, a recent simulation of the evolutionary origin of hierarchy argues that biological networks, from the level of organic molecules and up, become hierarchical only in the presence of what the authors call ‘connection costs’. When there are no connection costs, claim the authors, these networks tend to develop flat structures (Mengistu et al. 2016). In other words, molecules, single-cell organisms and herds of mammals are just like the capitalists who own McDonald’s: they all self-organize to minimize their transaction costs in their quest for maximum gain.

With this in mind, should we trace the origins of capitalization back to Sumer? In my view, the answer is no:

- One of the distinguishing features of the capitalist mode of power is that power appears as a universal quantitative relationship between entities (relative prices). This feature first emerged in the early the European Bourgs and was later formalized by Johannes Kepler to describe the forces of the cosmos. In Sumer, powers (in plural) were stand-alone qualities. The idea that power was a universal quantitative relationship between entities was inconceivable.

- The “larger use of credit”, as Veblen called it, also a key feature of the capitalist mode of power, presupposes the growing universality of the price system. This condition did not exist in Sumer.

- Forward-looking capitalization is a derivative of the larger use of credit, again, inconceivable in Sumer

- Differential capitalization emerges from the wider use of capitalization, unimaginable in Sumer.

Of course, if you can show that these observations are false, or that tracing capitalization back to Sumer is indeed useful and revealing, I’ll withdraw these contestations.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

Is it possible to make an extensive list of all the factors that affect capitalization. My google searches are inadequate, because i don’t know the correct search terms to look for.

You might find the following observations overly general, but it is useful to point them out.

1.

You can make a list, but it will include everything that capitalists believe affects earnings, hype, risk and the normal rate of return. In other words, it will include anything and everything that capitalist modellers (and now days, also their AI algorithms) manage to map — and then some (gut feelings, animal spirits, etc.). However, I don’t think this long list will get you anywhere.

In my view, the first step is to create not a list, but a theory/model that allows us to organize, interrelate and, most importantly, weigh the different forces that bear on differential capitalization. This is what CasP research proposes and tries to do, and it is anything but simple.

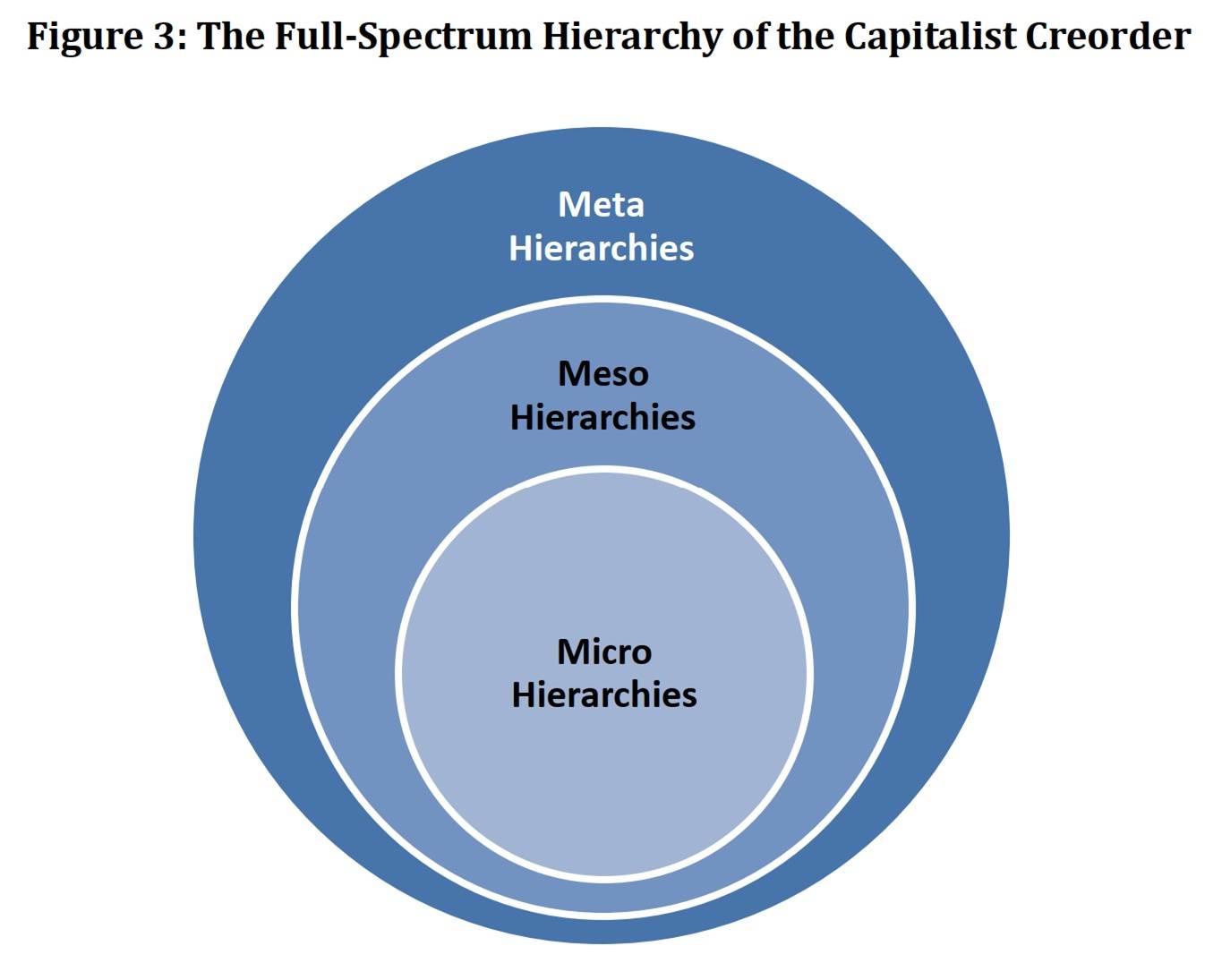

In our paper ‘Growing Through Sabotage’ (2020), we have a section on ‘Full-Spectrum Hierarchy’, where we write that:

[…] the capitalist creorder can be conceived of as a full-spectrum hierarchy, an ever-changing enfoldment of vertical structures nested within other vertical structures. Ranking the different hierarchies of capitalism from the most abstract down to the most concrete, we can say that the more concrete hierarchies are regulated by – and in this sense enfolded in – the more abstract ones. A simplified illustration of this enfoldment is shown in Figure 3: the lowest level of abstraction comprises micro hierarchies; the micro hierarchies are nested in meso hierarchies; and the meso hierarchies are themselves encompassed by the meta hierarchies.

What do the different levels consist of? Begin with the most abstract, meta hierarchies. The hubs of these hierarchies comprise the foundational institutions of capitalism, including, among others, the notion of ‘liberty’ (the differential Latin libertates fused into a universal notion of freedom), the concept of ‘private property’ (the negative Latin privatus inverted into a positive notion of possession), the idea of ‘investment’ (the feudal power of investiture reincarnated as a productive act) and the ritual of ‘capitalization’ (the ancient Mesopotamian caput, or head, made into a fractal-like algorithm of power) (Nitzan and Bichler 2009: 26, 227-228; Part III). The nodes of the meta hierarchies are the broad facets of society – the various dimensions of culture, ethnicity, religion and nationalism, among other things. And the links that tie the hubs to the nodes are the conduits through which the former gradually, and with plenty of setbacks and reversals, mould, leverage, internalize and encompass the latter. [Footnote: Think of how the fractal-like sprawl of concepts such as ‘financial accounting’, ‘investment’ and ‘capitalization’ penetrate and permeate all levels of business – from the small grocery store, family firm and largest conglomerate, to mutual, pension and sovereign wealth funds, to patents and copyrights – as well as other social institutions and organization, such as the military (the capitalized ‘quantity’ of the military arsenal and the ‘return on military assets’), organized religion (‘Islamic finance’ and ‘faith-based funds’), NGOs (‘cultural capital’ and ‘social capital’), workers (‘human capital’) and so on (Nitzan and Bichler 2009: Ch. 9).] At the meso level, the hubs are capitalist polities, corporations and NGOs, the nodes are individual subjects and the links are the capitalist institutions, patterns of thought and modes of behaviour that weave them into shifting hierarchies. And it is only at the lower, micro level of this full-spectrum enfoldment that we find the inner structures of formal organizations examined by Fix.

So if [Blair] Fix is right in arguing that greater energy capture per capita requires more hierarchical coordination, we can go even further: we can hypothesize that, as the capitalist mode of power deepens and globalizes, a significant – and perhaps growing – proportion of this hierarchical coordination will occur outside the boundaries of formal organizations. It will take place not only at the intestinal micro hierarchies of corporations and governments, but also – and increasingly so – at the meso and meta levels of scale-free networks: the hubs and nodes here are the foundational institutions of capitalism, the broad cultural and political facets of societies and their basic organizational units, while the connecting edges are trade, production and ownership ties, the various media of ideology, religion and education, the law and, ultimately, the threat of force and violence.

2.

No matter how successful the theory, it is at best an approximation anchored in its own time and history. Moreover, and crucially, CasP theorizes and researches capitalized power, not the undermining of capitalized power. It is a guide to what is, not to what can be made. This is a crucial distinction. In order to overturn capitalism, you need to understand it; but understanding of what currently exists is not enough. The reason is that every step of overturning capitalism, even the smallest, generates new formations whose structures and constellations are difficult and often impossible to foresee. It took capitalists half a millennium of turbulent, path-dependent trial and error to undo feudalism. There is no reason to think that autonomous formations can overturn capitalism on a preset list or even a theory, no matter how insightful. Theory-informed action is forever work in progress.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

Anything that affects future earnings, hype, risk and the normal rate of return impacts capitalization. But undermining these factors must be intertwined, or at least go hand in hand, with autonomous, non-capitalized form of organization to address the material needs and wellbeing of most people. Without these alternatives, the power logic of capitalization remains intact and its quantities will rebound.

It is important to distinguish between academia and science. They are often opposite to one another.

October 8, 2022 at 9:10 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #248404

October 8, 2022 at 9:10 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #2484041. I don’t understand the idea that capital discounts use value. The processes of power may or may not involve the creation of use value, but, in my view, capitalization is entirely independent of it.

2. In Sumer, wealth wasn’t thought of as Capital in the modern sense, let alone as discounted future earnings. Wealth was obtained by force, confiscation and royal/religious decree. There was no notion of “normal earnings” and “risk”. The future was deemed unknowable, subject to the whims of the gods. I don’t see the point of generalizing the modern ritual of orderly capitalization to pre-capitalist societies, let alone ancient ones.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

October 7, 2022 at 5:41 pm in reply to: Is Exchange Value Really Just Capitalized Use Value? #248398If capitalization is the only pricing mechanism in capitalism, this would imply that what Marx calls exchange value is, in fact, just discounted use value, i.e., exchange value is capitalized use value.

Why do you say that discounting capitalizes use value (rather than power)?

Of course, wages and wage labor predate the emergence of capitalism by thousands of years, which implies that capitalization predates capitalism by thousands of years.

Capitalization was first used, embryonically, sometimes in the 14th century; was first formalized, if only tentatively, in the middle of the 19th century; and came into common use and full dominance in the second half of the 20th century. You can argue that capitalists were always forward-looking, and that the prices of their assets represented, or at least reflected, however unknowingly, future expectations. But I find it hard to think of the daily wage in Sumer as capitalizing something.

Within the nomos of the Market, it does not matter to a capitalist that Musk is more powerful than he/she because the capitalist owes Musk nothing.

1. It seems that we have a rather different notion of power. For us, power is a quantitative relationship between entities, which, in capitalism, takes the form of differential capitalization (and its differential elementary particles). If Musk’s capitalization is 1,000 times that of another capitalist, he is 1,000 more powerful.

2. Does it matter to other capitalists that Musk is stronger than they are? In our view, the answer is a definite yes. This is the crux of capital as power. Musk being stronger means he is able to creorder the world against the interests/opposition of other capitalists and in doing so retain and augment his differential capitalization. For those whose key purpose is more power, having less of it is the ultimate loss.

3. And in the capitalist mode of power, capitalists — regardless of what they think and feel — are compelled to seek differential capitalization, lest they be marginalized or weeded out altogether. And since, in capitalism, differential capitalization depends on and represents power, capitalism cannot be anything other than a mode of power.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

In capitalism, power is priced in and traded for $, and since in principle prices are the same for everyone, Musk and you will buy the same power for the same price.

But this universality does not imply that Musk and you have the same power. If Musk owns $232 billion and you own $232 million, he is 1,000 times more powerful than you — even though both of you face the same prices.

In general, capitalists grow more powerful not because they buy for less than others, but because they change the world in such a way that makes the price of what they own rise faster than other prices.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

1. Creorder means a (dynamic) process of creating a (static) structure (or a given pattern of change). In my view, the specific form of a given creorder is open ended.

2. It is well known that Athenian democracy included only a fraction of the population, but its impulse was creating a society of citizens based on direct democracy (autonomy), philosophy (love of truth) and science (proof). All three components of this triangle assume and imply the absence of power. To me, articulating and fleshing out this triangle was a creorder.

3. The relationships among capitalists are very different. Their key ritual is differential accumulation – which implies not only controlling the rest of society, but also creating a power hierarchy of capitalists and corporations. In other words, their very purpose, even among themselves, is power.

September 30, 2022 at 6:06 pm in reply to: Inflation is always and everywhere a redistributional phenomenon #248364

After decelerating for forty years, inflation is finally back, along with horror stories about capitalists who “use it” in order jack up their prices.

A recent paper in the Intercept bedevils a talkative executive who Has Been “Praying for Inflation” Because It’s an Excuse to Jack Up Prices. (Hat: https://twitter.com/HeavenlyPossum.)

Iron Mountain’s CEO, William Meaney, tells participants in an earnings call that “it’s kind of like a rain dance, I pray for inflation every day I come to work because … our top line is really driven by inflation. … Every point of inflation expands our margins.” And his CFO, one Barry A. Hytinen, can’t agree more: “we do have very strong pricing power” and for the company, inflation is “actually a net positive.”

And its not merely about raising prices. It is about raising them faster than others.

As Meaney explains, “where we’ve had inflation running at fairly rapid rates … we’re able to price ahead of inflation” — that is, increase its prices at a greater rate than the high recent rates of inflation. Raising prices, he says, “obviously covers our increased costs, but … a lot of that flows down to the bottom line.”

Everyone tries to beat the average: “People are seeing what FedEx, UPS, and others are having to do to actually manage their business and pass on that inflation.”

There is also a downside worth mentioning — namely, the differential loses of all those doomed subjects who forever trail the average. But this is just an unfortunate externality: “I wish I didn’t do such a good dance,” boasts Meaney, “but that’s more on a personal basis than on a business model.” According to Hytinen, “we feel for folks [but] we have a high gross margin business, so it naturally expands the margins of the business.”

***

Naturally, neither the executives nor the reporters consider the possibility that differential price increases and the differential profits that come with them are not the consequences of inflation, but its prime causes.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

-

AuthorReplies