Forum Replies Created

-

AuthorReplies

-

My arithmetic was not meant to imply that reading novels was a chore.

Of course not. My answer was a tongue-in-cheek clarification for others….

And thank you for the additional suggestions!

Arithmetic aside, reading is a joy, not a chore.

Yes, the branding of companies based on their ‘home state’ has become increasingly anachronistic.

Thank you Scot.

I am a little confused by the conclusion that “(2) the relative power of U.S. capital continues to wane,” which appears to be based on your discussion regarding Figure 3 and “net profit shares. ”

1. The conclusion is based on Figures 2 and 3.

I thought power (and, therefore, relative power) is determined by market value (i.e., capitalization), not by net profit shares (i.e., earnings multiplied by the number of shares outstanding). By factoring out share price, you’ve eliminated any consideration of differential discount rates and differential “hype,” which conceivably could result in lesser profits representing greater power. What do the relative market capitalization data show?

2. You are correct that, according to our CasP view, differential capitalization is the ultimate power yardstick, and that differential profit gives only a partial picture. However, there is something to be gained by looking at net profit only, since, over the very long haul, it is the main driver of capitalization.

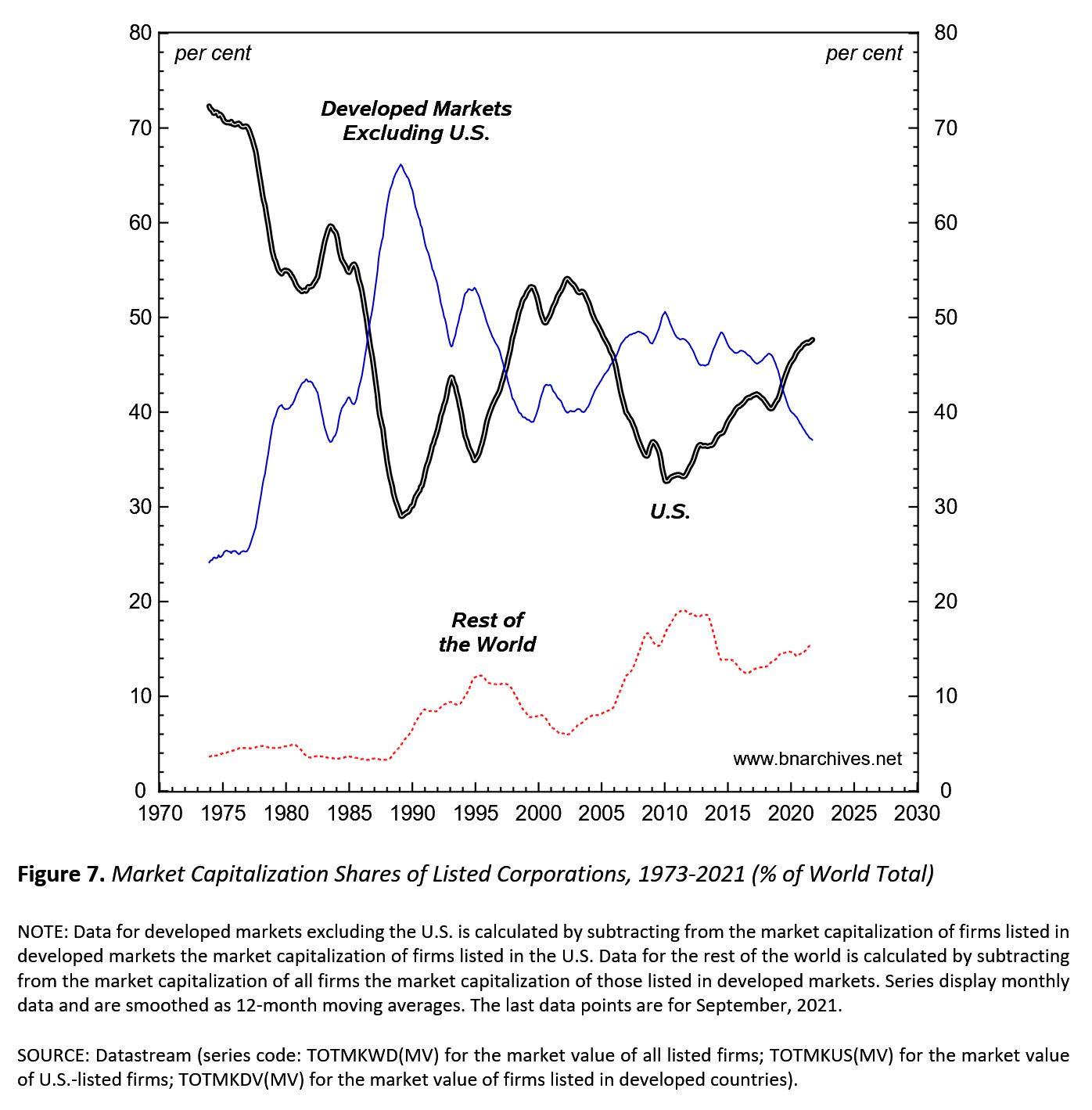

In any event, here is the figure for the global distribution of market capitalization. The downtrend of the U.S. share is not as steep as in the net profit figure, but it is negative nonetheless. And remember that these data start only in the mid 1970s. My hunch is that the U.S. share of global market capitalization in the 1950s was higher.

Thank you James and (mostly) Blair for making it happen.

This is part of a wider project that James McMahon and I are trying to get off the ground.

Excellent.

However, how can we forget China?

We are silence on China because we don’t understand and read any of its languages and are dubious of its data. CasP research of China will have to be done by people who can read the languages and assess the data.

Dominant Capital and the Government

Shimshon Bichler and Jonathan Nitzan[1]

Originally published on The Bichler and Nitzan Archives.

***

This note contextualizes the ongoing U.S. policy shift toward greater ‘regulation’ of large corporations. Cory Doctorow (2021) and Blair Fix (2021) are optimistic about this shift. We doubt it.

1. The Limits of Power

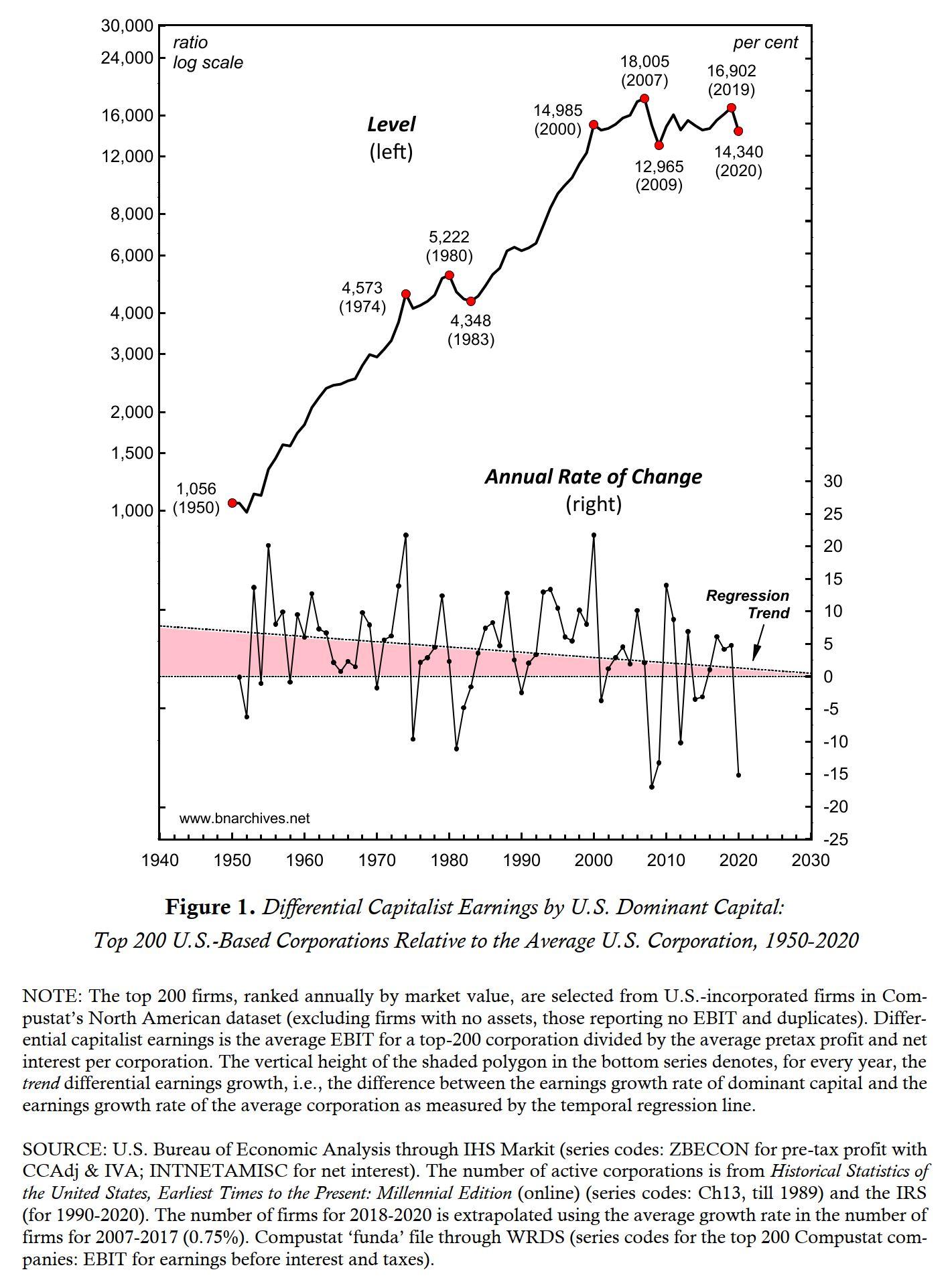

Large U.S.-based corporations are extremely powerful, but the growth of their power has decelerated considerably.

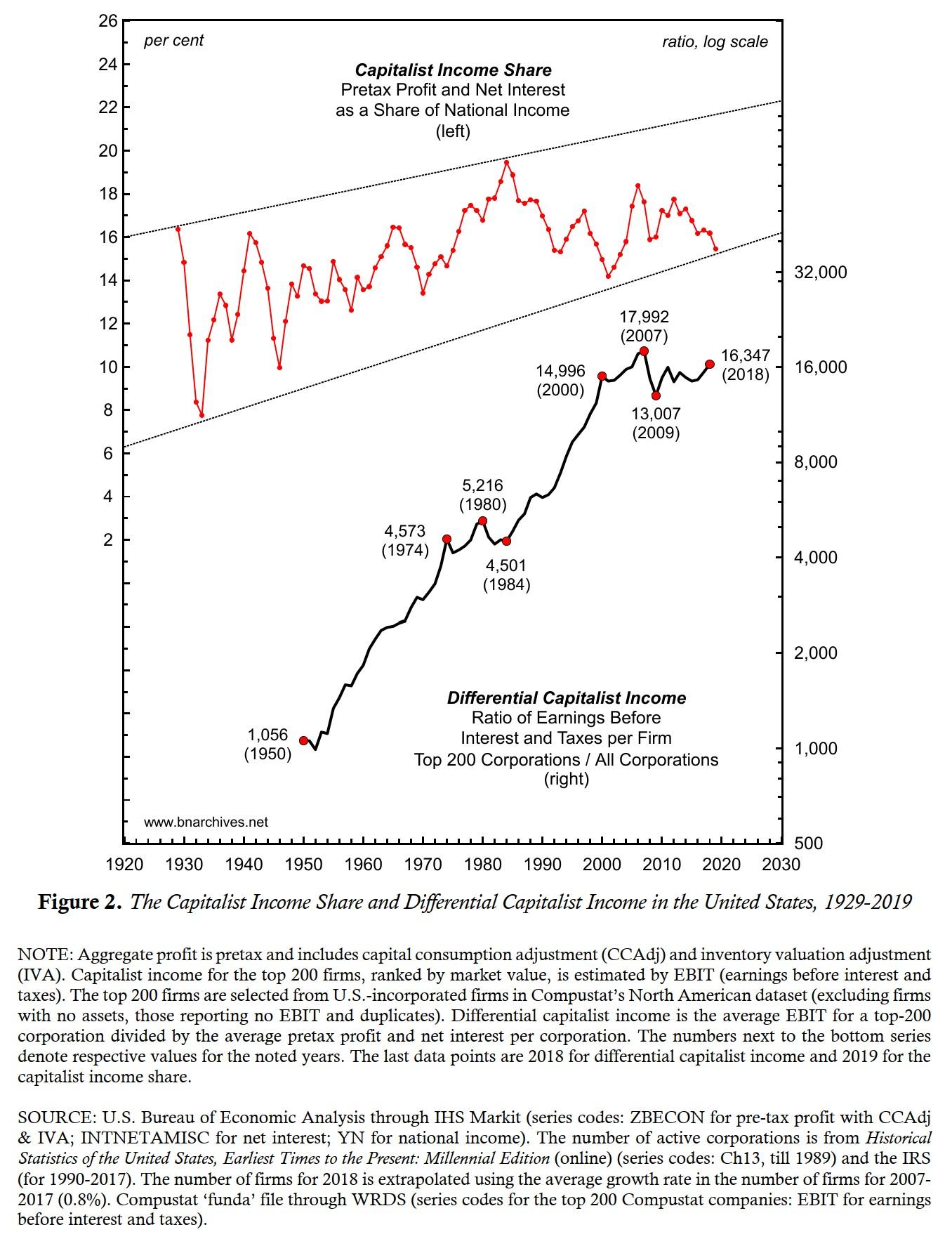

Figure 1, updated from our ‘Corporate Power and the Future of U.S. Capitalism’ (Bichler and Nitzan 2021), shows the earnings before interest and taxes (EBIT) of the top 200 U.S.-based corporations, ranked by market capitalization, relative to those earned by the average U.S. corporation. The top series confirms that this differential – which proxies the relative power of the top 200 firms – has grown exponentially, rising from roughly 1,000 in 1950 to more than 15,000 in the 2000s. The bottom series, though, shows that the rate at which this differential power has grown trends downwards.

This long-term deceleration is not accidental. In fact, it is built into the very nature of social power. In our capital-as-power research – or CasP, for short – we argue that power always elicits resistance from those on whom it is imposed; that this resistance tends to rise along with power; and that the greater the resistance the more difficult it is to augment power even further. In other words, power is self-limiting (Bichler and Nitzan 2012, 2016, 2020).

The twenty-first century revival of anti-corporate sentiments and anti-capitalist movements around the world is part of this resistance – as are some of the policy reforms emerging in their wake. But these reforms shouldn’t be over-hyped.

2. The Capitalist Mode of Power

Our CasP analysis claims that, as capitalism develops, governments and large corporations become increasingly intertwined organs of the same capitalist mode of power. We call this mode of power the ‘state of capital,’ and we label the large government-backed corporate coalitions at its core ‘dominant capital’.

The coalescence of governments into the capitalist mode of power does not mean that ‘policymakers’ can no longer take an independent stance. They can. But the likelihood of them doing so, as well as the scope of their independence, tend to diminish as the capitalist mode of power creorders – or creates the order of – more and more aspects of social and private life. As this corporate-government integration unfolds, government organizations and officials, including ‘reformers’, not only get entangled in the web of capitalized power, but they also find themselves conditioned by its very concepts, symbols, ideologies and rituals. Consequently, most of them cannot even conceive of fundamental change, let alone bring it about.

From this broad perspective, a meaningful shift within capitalism – and certainly a shift away from it – is less and less likely to come from above. If this shift is to materialize – and in our view, the current prospects for it remain dim – it is likely to come not from reformist governments and soulful corporations, but from below or from without. It will be affected either by social movements mobilized by radical rethinking of capitalized power, or by environmental calamity. Finally, and importantly, this change is likely to materialize not peacefully, but conflictually.

3. Why are Neoliberal Governments so Big?

Think of contemporary governments. Since the 1980s, neoliberal ideology has demanded that state ‘intervention’ and ‘regulation’ be scaled back. It has called for capitalist efficiency to substitute for bureaucratic red tape, for market transparency to replace state corruption, and for equal opportunity to displace hierarchical power. It insists that government should stop ‘crowding-out’ private investment and cease interfering with the so-called free market. It argues that for markets to expand, governments must shrink.

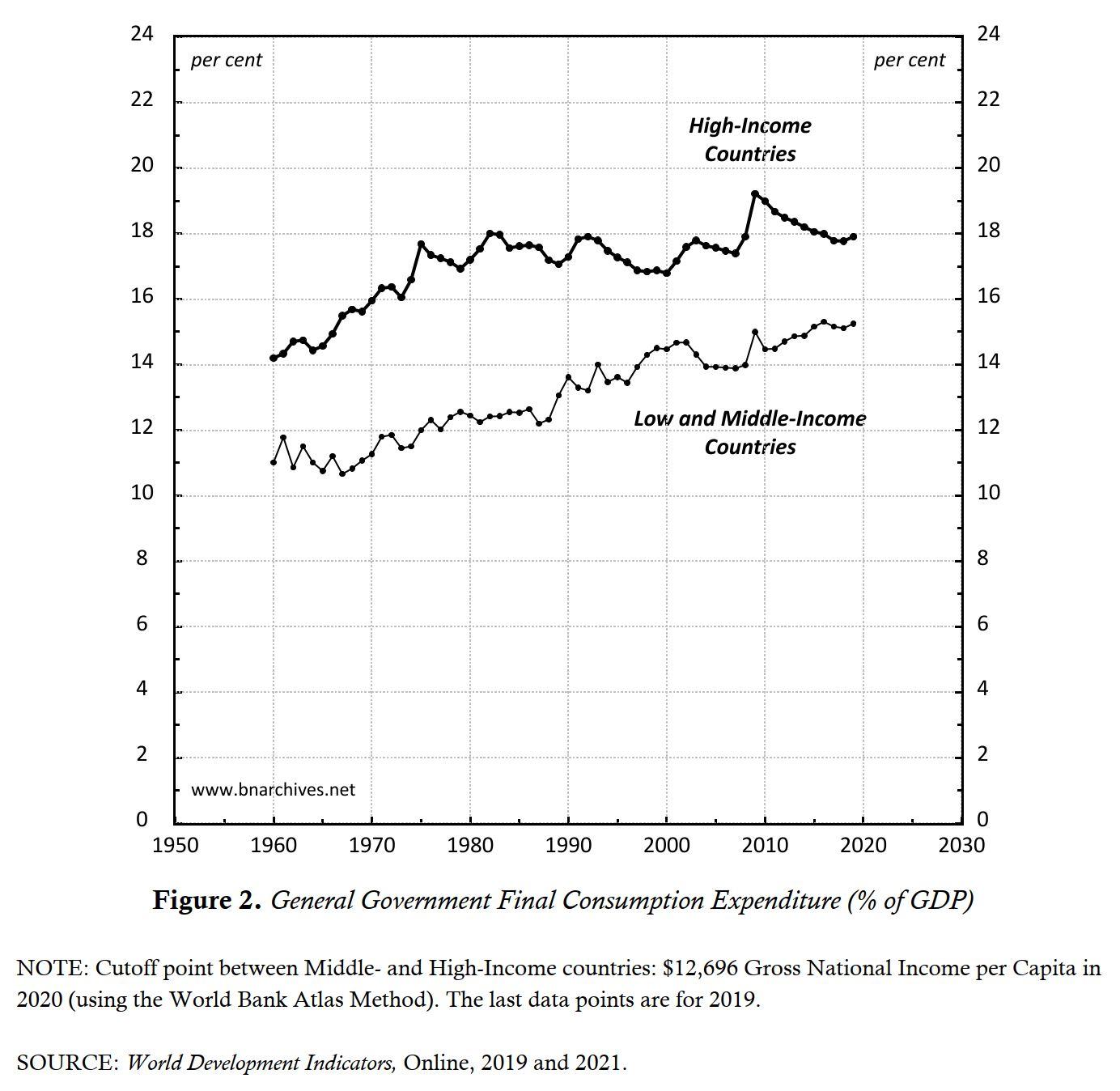

And yet, as Figure 2 shows, the victory of neoliberalism hasn’t made government any smaller. Not by a long shot. In high-income countries, the national income share of government consumption spending remains as large as it was before the onset of neoliberalism, while in low- and middle-income countries, it continues to grow bigger and bigger.

And that shouldn’t surprise us. The capitalist mode of power and the dominant-capital coalitions that rule it do not require small governments. In fact, in many respects, they need larger ones.

As a mode of power, capitalism thrives on multiple forms of ‘strategic sabotage’ – that is, on limiting and redirecting the energy of human beings toward the augmentation of capitalizing power. Dominant capital prevents most people from cooperating, democratically and directly, to improve the well-being of their society and environment. Instead, it forces them to fortify and amplify the very capitalized power that dominates them. And this forcing requires a whole slew of threats, limitations, and the open use of force – in other words, it begets strategic sabotage.

The thing is that, left unregulated, strategic sabotage can easily overbuild, causing the mode of power to implode under its own weight. And that’s where government spending comes in as a mitigating force. From this viewpoint, bigger government – particularly its sprawling social programs and transfer payments – mirrors not the failure of neoliberalism, but its very success.

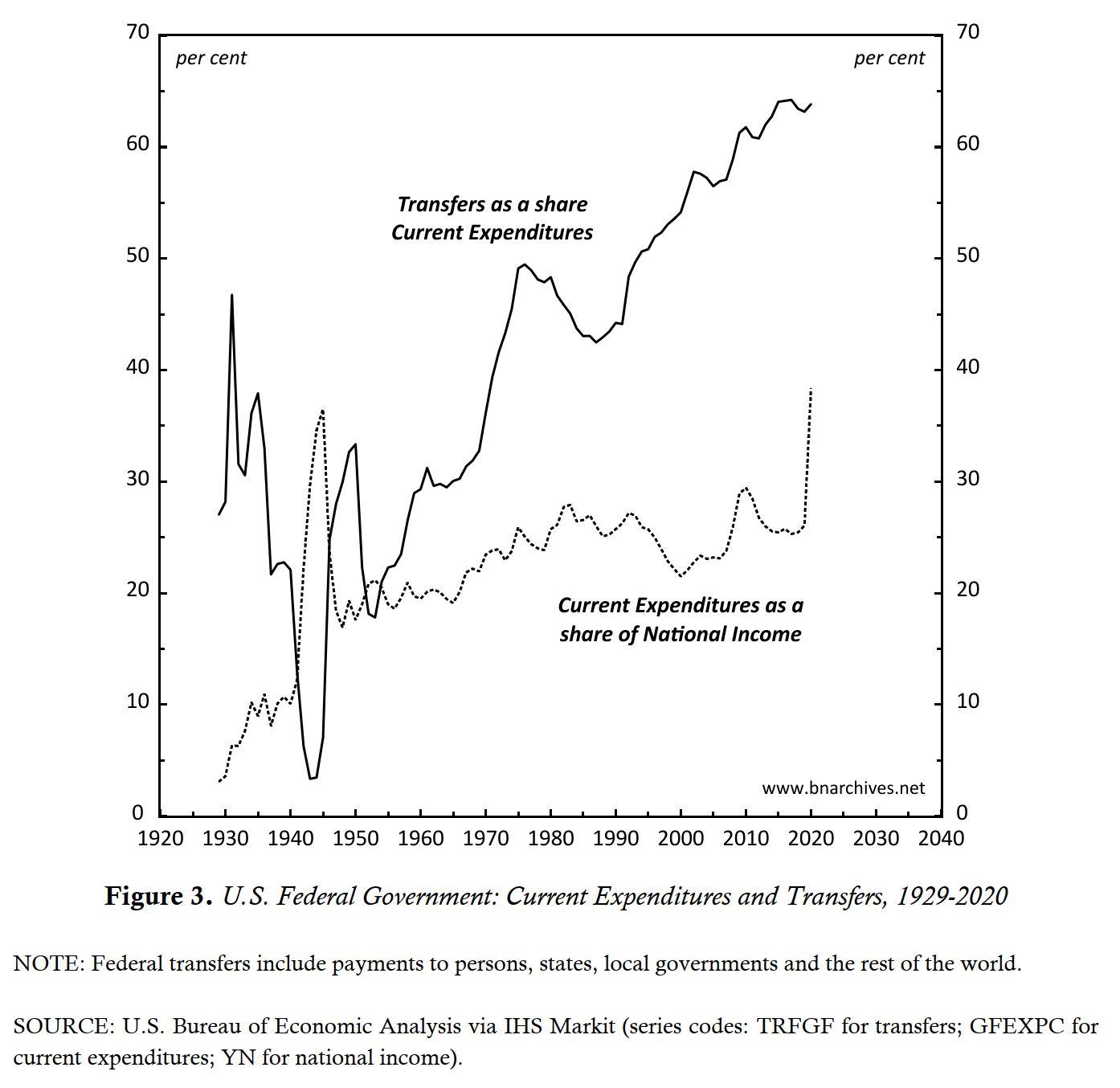

Figure 3 shows the changing importance of federal transfer payments in the United States. The dashed series depicts the level of current expenditures by the federal government, expressed as a share of U.S. national income. Note that these expenditures include purchases of goods and services, as well as transfer payments for which no goods and services are rendered in return. The solid series displays the share of transfer payments in overall current federal expenditures.

The relationship between the two proportions is telling. Initially, the association was negative. During the 1930s and 1940s, when the national income share of current federal expenditures increased, the share of transfers in these expenditures declined – and vice versa when government expenditures fell. This inverse relationship means that transfers were relatively stable, and that most of the ups and downs in federal spending were due to ups and downs in current government consumption.

But soon enough the relationship flipped. From the 1950s onward, the national income share of current federal expenditures trended upward – and, for the most part, this uptrend was driven by a relentless increase in the share of transfers. All in all, during the postwar era, this share rose 13-fold – from less than 5 per cent in the early 1940s, to nearly 65 per cent presently.

With this observation in mind, it is perhaps worth noting that the 2020 Covid19-related surge in current federal spending – a surge that many like/hate to think of as active ‘Keynesianism’ – was accounted for mostly by passive transfers.

The gradual shift from discretionary expenditures on goods and services to reactive transfers is typical of many governments around the world, and it suggests that these governments are far less potent than their size might imply. In fact, one can argue that the bigger ‘transfer states’ of today are far weaker than the smaller ‘consumption states’ of the Keynesian era. Their apparent largess indicates not greater power but subjugation: a built-in deference to dominant capital, whose strategic sabotage must be offset, at least in part, by unemployment insurance benefits, welfare payments and the like.

4. Summary

On paper, the U.S. government is free to legislate its path and determine its policies. In principle, there is little to prevent a resolute U.S. administration from challenging the power of the country’s dominant capital and clip the wings of its largest firms.

But it would be good to remember that the U.S. government – like most other governments – has become part and parcel of an increasingly global state of capital. This integration has undermined the de facto autonomy of governments everywhere. Whether willing or reluctant, many if not most policymakers have become pawns of a global mode of power they cannot control and that forces them to tranquilize the increasingly vulnerable population that dominant capital helps create. Government spending has inflated, but this inflation betrays weakness, not strength.

Larger-yet-weaker neoliberal governments are the alter-ego of bigger-and-meaner dominant capital. It is hard to think of any important sector or aspect of society, in the United States and elsewhere, where dominant capital does not dominate. It is true that, faced with increasing resistance, the rising power of dominant capital in the United States has slowed down significantly over the years and seems to have stalled completely in recent times (Figure 1). But the level of this power is still greater than ever, and it is yet to show any meaningful decline. Finally, and importantly, the stalling advance of U.S. dominant capital makes it extra vigilant against any serious challenge.

Prediction: if the current U.S. government delivers on its promise to curtail the might of the country’s largest corporations, it will face the wrath of the most powerful megamachine the world has ever seen.

Endnotes

[1] Shimshon Bichler and Jonathan Nitzan teach political economy at colleges and universities in Israel and Canada, respectively. All their publications are available for free on The Bichler & Nitzan Archives (http://bnarchives.net). Work on this note was partly supported by SSHRC.

References

Bichler, Shimshon, and Jonathan Nitzan. 2012. The Asymptotes of Power. Real-World Economics Review (60, June): 18-53.

Bichler, Shimshon, and Jonathan Nitzan. 2016. A CasP Model of the Stock Market. Real-World Economics Review (77, December): 119-154.

Bichler, Shimshon, and Jonathan Nitzan. 2020. The Limits of Capitalized Power. A 2020 U.S. Update. Working Papers on Capital as Power (2020/06, December): 1-16.

Bichler, Shimshon, and Jonathan Nitzan. 2021. Corporate Power and the Future of U.S. Capitalism. Real-World Economics Review Blog, January 4.

Doctorow, Cory. 2021. End of the Line for Reaganomics. Capital as Power Blog, September 26.

Fix, Blair. 2021. How Dominant are Big US Corporations? Economics from the Top Down, September 29.

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

Jonathan Nitzan criticises Marx for “dialectical determinism” which “perhaps explains why many of his predictions failed to materialize.”

1.

Very interesting posts, Rowan, but I think their focus is different than mine in the lead post. Notice that I wrote that

Marx’s dialectical determinism was simply too demanding for his narrow ‘economic’ argument

In other words, in my view the problem with Marx’s method is not his quest for dialectical determinism, but his basing of dialectical determinism on narrow economic arguments.

2.

The motivation for this post was the question of alienation, which Marx anchored in the commodification of labour. CasP research suggests that alienation — the estrangement of human beings from their own actions and creations — is an aspect of power writ large, and that the commodification of labour is only one aspect of this power. If this claim is valid, it makes Marx’s economic focus too narrow and therefore potentially misleading in its derivations.

3.

And, yes, many of Marx’s expectations — the falling tendency of the rate of profit, immiseration, deeper and deeper crises, the cascading collapse of capitalism, among others — are yet to come true. Hanging these delays on ‘countervailing forces’ is reminiscent of neoclassical ‘distortions’. A theory that claims to grapple with the fate of humanity should include any meaningful countervailing force in its core. If you think of finance, politics, culture, international relations, etc. as mere derivatives of — or worse still, external auxiliaries/shocks to — the labour process, don’t be surprised that your economically-based predictions end up being off.

I hope these comments help clarify my point.

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

Thank you Rowan for raising this subject, a topic that CasP researchers haven’t examined, certainly not systematically, as far as I know.

I’m curious how one can devise an ex-ante stress test for capitalism in general and Covid-19 capitalism in particular. So far, ex-post differential accumulation seems to continue along with the underlying processes of strategic sabotage.

Looking forward to reading your argument.

From 1960 until 2000, 10-year US treasury yields appear to have correlated with the average inflation rate of the previous ten years. How does this relate to the Power Index and/or systemic fear, if at all? Or is this just what creordering looks like?

- Power Index = (future profit * hype)/(normal rate of return * risk)/wage rate

- Systemic Fear Index =12-month correlation (current price, current EPS).

With respect to the Power Index, current inflation can affect three current variables: hype (up or down), the normal rate of return (mostly up) and the wage rate (almost always up). It should have no impact on future profit and risk, which are forward-looking variables. All in all, the overall direction of its effect on the Power Index is difficult to theorize.

With respect to the Fear Index, current inflation can affect price and EPS, which are both current, though the impacts are unclear. The overall effect on the price-EPS correlation is therefore hard to guess.

Schiller’s correlation between treasury yields and inflation 10 years earlier adds another layer to these already opaque relationships.

Maybe this is one of Mr. Schiller’s irrationalities?

- This reply was modified 4 years, 8 months ago by Jonathan Nitzan.

Capitalists no longer fear the ruled because the ruled think they’re capitalists, too, and they’ve been conditioned to blame their government for their failures, not capitalists

Yes, fraud is a very potent weapon, particularly in capitalism. But we should be careful of appearances. The overt power of the rulers always hides covert fear of losing this power, and collapse, from Belshazzar in Babylon to the communist parties in Euroasia, often occurs when the rulers are caught in their hubris.

This chart, taken from ‘The Limits of Capitalized Power. A 2020 U.S. Update‘, shows that the power of U.S. capitalists in general and dominant capital in particular, having increased dramatically in the last century, is now running against an asymptote.

I’m not sure this asymptote is entirely lost on those in power.

4. I think the WSJ critique here is misguided.

The writer contrasts two examples – one relative, the other absolute: (1) an equal 10% increase/decrease in the stock prices of a very big and a very small company; and (2) an equal $10bn increase/decrease in the earnings of these same companies.

In my view, this is a comparison of apples and oranges. Because the very large company has a greater number and/or a more expensive stock price than the very small company, a 10% increase in the price of this very large company has a much lager absolute effect than a 10% increase in the price of a very small company. Market-cap basing helps reflect these absolute differences.

This market-cap basing isn’t necessary with EPS, since this measure is already computed in absolute terms (dividing the $ sum of all earnings by the number of all outstanding shares). This is why a $10bn gain/loss of the two companies should be treated equally.

Had the WSJ writer complained that S&P weighted equal % changes in prices but didn’t weight equal % change in earnings, then the criticism would have been valid. But as stated, I think it is invalid.

5. I look forward to an empirical analysis of both stocks and bonds that explains the changing correlation of stock price and recent earnings, and why changes in the correlation correlate so tightly with the stock price/wage ratio.

A brief follow-up to some of your specific points, Scot:

1. Compounding interest is backward-looking (it adds the interest that wasn’t paid to the balance), so in that sense, it is ‘opposite’ to forward-looking capitalization. I look forward to insight from considering them jointly.

4. Stock index data are often adjusted and spliced. I doubt that in the case of the S&P series adjustment/splicing alters the overall trajectory. As far as I know, EPS and price indices are based on the same stock weightings.

5. I look forward to bond-stock analysis that explains the changing correlation of stock price and recent earnings.

6-8. I don’t understand your ‘one question’. Our power index is the stock price/wage ratio. Our systemic-fear index is a correlation between stock price and recent earnings. I cannot see any technical reason for these totally different indices to correlate.

- This reply was modified 4 years, 9 months ago by Jonathan Nitzan.

- This reply was modified 4 years, 9 months ago by Jonathan Nitzan.

Thank you Scott. Here are some thoughts.

1. The CasP emphasis on forward-looking capitalization has nothing to do with investors/capitalists being ‘rational’ or ‘irrational’. In our view, forward-looking capitalization is a ritual. (Until the early 20th century, it was heatedly debated by investors and theorists, many of whom thought it was fraudulent and that asset prices should reflect backward-looking ‘real’ means of production.)

2. Forward-looking capitalization does not mean that capitalists ignore the past. It simply means that they use whatever information they have — including the past and including recent earnings — to predict future earnings all the way to infinity.

3. I think we agree that the short-term gyrations of last year’s earnings cannot tell us much about their long-term trajectory. So, if investors indeed discount expected long-term future earnings, stock prices should not be correlated with the ups and down of recent earnings.

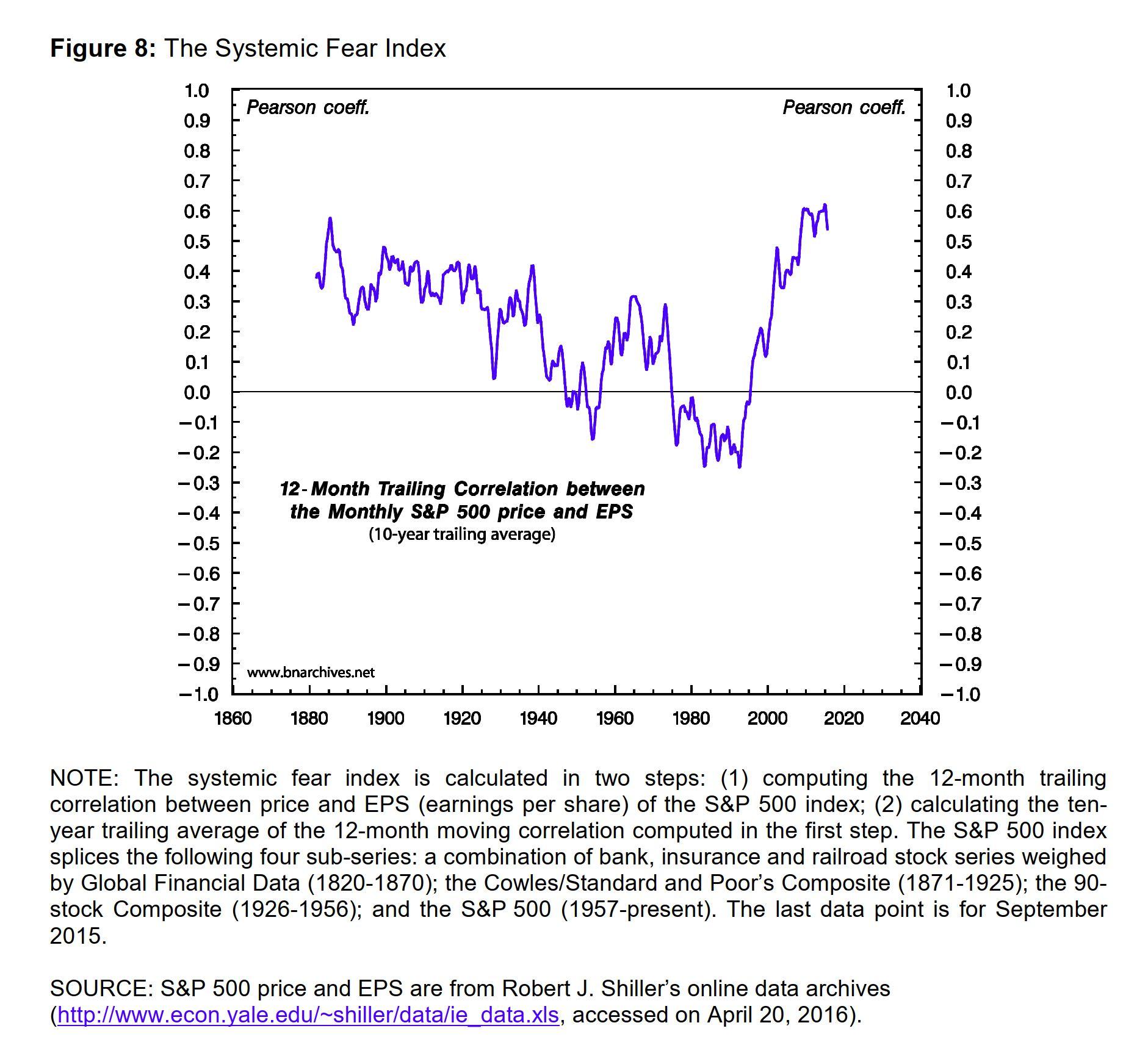

4. The data in the following chart show that, during the 1880-1980 period, as the forward-looking ritual gained traction, the correlation between price and recent earnings trended down, In the 1950s, and then in the early 1980s, it turned negative.

5. This long-term decline inverted in the early 1990s. Since then, the correlation between stock prices and recent earnings rose more or less uninterruptedly, reaching all time highs recently.

6. This inversion, we argue, represents a breakdown of the forward-looking capitalization ritual, and this breakdown is not accidental. In our opinion, it represents systemic fear – investors’ fear that the capitalization system itself might be unsustainable.

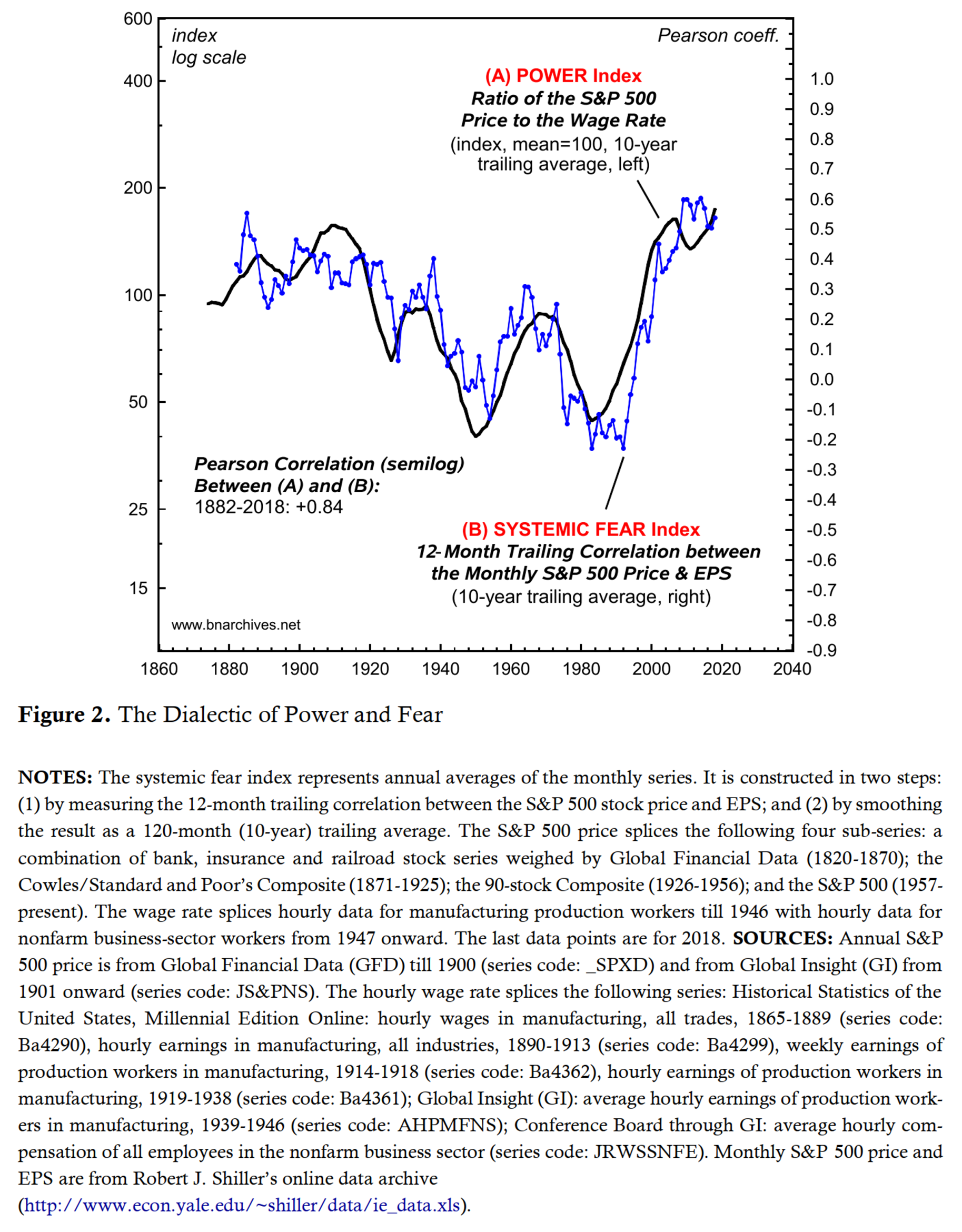

7. As the following chart shows, the entire history of the systemic fear index is associated, dialectically, with the capitalized power of capitalists, measured here by the stock price/average wage ratio: the higher this power, the greater the fear of capitalists that it cannot be sustained, and therefore their greater systemic fear.

8. The correlation in this chart suggests that the future profit expectations of forward-looking capitalists are calibrated by their power: the lesser/greater their power, the smaller/larger the significance of recent profit for their future-earning predictions.

9. This discussion deals with capitalists as a group and in that sense is unrelated to differential accumulation. Hands-on capitalists accumulate differentially by creordering the power underpinnings of their own assets in ways that affect expected differential profit, hype and risk perceptions, while absentee owners do the same by correctly predicting this creordering. The ongoing changes in overall power of capitalists calibrates the way in which their differential efforts translate into future earnings expectations: the greater/lesser this power, the greater/lesser the impact of their current actions-turned-profit on future earnings expectations.

10. And all of these differential processes — although happening here and now, and even though they are affected by the present to various degrees — are focused on the future.

-

AuthorReplies