Forum Replies Created

-

AuthorReplies

-

September 28, 2022 at 12:03 am in reply to: Confidence in Obedience, or Confidence in Liquidity? #248359

I appreciate our dialogue, always.

A few observations:

The Capital Asset Pricing Model (“CAPM”) […] is the basis of CasP’s insight regarding beating the average

I don’t think CasP derives anything from CAPM. In fact, in some sense, the two theories are opposite. CAPM is a neoclassical model that stipulates how passive investors (supposedly) pick the right combination of (presumably known) stock returns and risks. Our theory of differential accumulation tries to study how active capitalists change returns and risks (see Ch. 11 of Capital as Power).

I think the assessment that inflation is driven by the desire to raise prices faster than peers is overly simplistic and incorrect.

CasP does not say that capitalists “desire” to raise prices faster than average. Instead, it argues that capitalists seek to raise capitalized profit faster than average, and that, occasionally, when M&A decelerates, they are tempted to use stagflation to achieve it.

We need to think in terms of things like supply chains (or value chains) instead of just the prices end consumers see.

Correct. But this recommendation bursts into an open door.

September 25, 2022 at 8:09 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248351Thank you for the comments, Scot.

Do you believe your Power Index directly measures confidence in obedience, or do you view it as merely indicative of it? I’ve gone back to the paper in which you first introduce the Power Index, but your assertions and reasoning are more logical than empirical.

Our logic goes as follows.

- We treat power as a quantitative relationship between entities. Our Power Index is the quantitative relationship between capitalists and workers, measured by the ratio of the S&P500 price and the average wage rate.

- The S&P price-to-wage ratio is set by capitalists (this ratio correlates almost perfectly with price and scarcely if at all with the wage rate), so in this sense it represents the confidence of capitalists: higher/lower confidence –> higher/lower price-to-wage ratio.

- We further assume that this confidence-read-price-to-wage-ratio represents the discounted value of future earnings capitalists expect to receive (relative to the wage rate). Since, in our view, these expected earnings depend wholly and only on society obeying the capitalists, it follows that the stock price/wage ratio represents the confidence capitalists have in the obedience of the those whom their rule (i.e., everyone/everything else).

- If our assumptions are incorrect, so is our interpretation.

- One can interpret our Power Index differently (as you do, when you call it “confidence in liquidity”), or devise other Power Indices.

Abstraction destroys the ability to study details that are ignored or eliminated for the sake of simplification. You can’t look at what you aren’t allowed to see.

I don’t think so. Your notion of “confidence in liquidity” is an abstraction. It does not prevent you from looking at the details being abstracted.

I think that theorizing a “State of Capital” does not go far enough, that it would be better simply to focus on understanding and studying the Market as sovereign and relegate the modern state to the Market’s subject, as we all are (including capitalists).

The study of the “state of capital” is in its infancy, and I doubt you can predict its potential reach and likely insights. Having said that, you are more than welcome to make the “Market” the supreme subject and see if it offers different/better insights.

And I’d prefer to jettison words like “ruler,” “ruled,” “citizen,” and “class” to focus entirely developing a new taxonomy based on differential power, which I think is more likely to lead to insights that eliminate such power altogether.

We scarcely refer to “citizens” and “classes”. I’m not sure, though, how one can speak of differential power without differentiating rulers from ruled.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 7 months ago by Jonathan Nitzan.

September 14, 2022 at 11:18 am in reply to: Confidence in Obedience, or Confidence in Liquidity? #248333I think “confidence in obedience” collapses too many disparate issues into a singularity, obliterating any opportunity to distinguish between those issues and understand their differences.

Yes, “confidence in obedience” is a way of describing the totalizing meaning of capitalized power (see Questions 15-16 in ‘The Capitalist as Power Approach’). I’m not sure, though, how the existence of this abstract notion is “obliterating any opportunity to distinguish between those issues and understand their differences.”

This where I think CASP’s outright rejection of the politics v. economics duality is problematic. I have always agreed with you that this dichotomy is a false one, that politics and economics are inseparable, but I also think we have to accept that this dichotomy, as false as it is, is a normative myth that has real power over people’s thinking and drives the formation of capitalist institutions. Whether we treat the state and Finance as separate entities or lump them together as “the state of capital,” the two operate in concert towards the same ends, but they operate differently and independently according to the normative myth and false dichotomy of politics v. economics.

I realize that we don’t share the same views on this matter, but I don’t think that we reject the politics-economics duality outright. Here is what we write on pp. 29-30 of Capital as Power:

To sum up, then, both neoclassicists and Marxists separate politics from economics, although for different reasons. The neoclassicists see the separation as desirable and, if handled properly, potentially beneficial. By contrast, Marxists view the distinction as contradictory and, in the final analysis, destructive for capitalism. Yet, both conclusions, although very different, are deeply problematic — and for much the same reason.

The difficulty lies less in the explanation of the duality and more in the widespread assumption that such a duality exists in the first place. Even E. P. Thompson, a brilliant historian who was otherwise critical of Marxist theoretical abstractions, seems unable to escape it. Writing on the development of British capitalism from the viewpoint of industrial workers, he describes the class socialization of workers as ‘subjected to an intensification of two intolerable forms of relationship: those of economic exploitation and of political oppression’ (1964: 198–99). In this dual world, the industrial labourer works for and is exploited by the factory owner — and when he organizes in opposition, in comes the policeman who breaks his bones, the sheriff who evicts him and the judge who jails him.

Now, this bifurcation is certainly relevant and meaningful — but only up to a point. From the everyday perspective of a worker, an unemployed person, a professional, even a small capitalist, economics and politics indeed seem distinct. As noted, most people tend to think of entities such as ‘factory’, ‘head office’, ‘pay cheque’ and ‘shopping’ differently from the way they think of ‘political party’, ‘taxation’, ‘police’, ‘military spending’ and ‘foreign policy’. Seen from below, the former belong to economics, the latter to politics.

But that is not at all what capitalism looks like from above. It is not how the capitalist ruling class views capitalism, and it is not the most revealing way to understand the basic concepts and broader processes of capitalism. When we consider capitalist society as a whole, the separation of politics and economics becomes a pseudofact. Contrary to both neoclassicists and Marxists who see this duality as inherent in capitalism, in our view it is a theoretical impossibility, one that is precluded by the very nature of capitalism. To paraphrase David Bohm (1980), from this broader perspective, the politics–economics duality is not a useful division, but a misleading fragmentation. It cannot be shown to exist — and if it did exist, profit and accumulation would cease and capitalism would disappear.

The consequences of this entanglement for capital theory are dramatic. As we shall demonstrate, without an ‘economy’ clearly demarcated from ‘politics’ we can no longer speak of quantifiable utility and objective labour value; and with these measures gone, neoclassical and Marxian capital theories lose their basic building blocks. They can observe that Microsoft is worth $300 billion and that Toyota pays $2 billion for a new factory, but they cannot explain why.

You write that:

Next to the capitalists themselves, it is the states whose potential “disobedience” is most concerning to dominant capital.

Yes. Conflicts within dominant capital, which we think of as a complex network of big capitalists, large corporations, government organs and so-called policymakers, are crucial. But in our view, these inner-class conflicts are tied to and delineated by the conflict between the rulers and the ruled. If this latter conflict did not exist or was insignificant, the share of profit in national income would have been far higher, the laws would have been very different and potentially far harsher for the underlying population, violence would have been more extreme, etc.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

September 12, 2022 at 4:12 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248330Thank you, Scot.

You define market liquidity as the existence of “potential buyers with money and a desire [to] spend it on capital assets.”

I agree that this is a precondition for the existence of asset markets – but so are enforceable laws, oxygen, food and human language, for that matter. What I’m unclear about, is what these general preconditions tell us about the direction of the stock market, let alone about capitalist power.

You are correct that, in the short run, investors seem concerned mostly with predicting the actions of other investors, or as Keynes famously put it in the General Theory:

. . . professional investment may be likened to those newspaper competitions in which the competitors have to pick out the six prettiest faces from a hundred photographs, the prize being awarded to the competitor whose choice most nearly corresponds to the average preferences of the competitors as a whole; so that each competitor has to pick, not those faces which he himself finds prettiest, but those which he thinks likeliest to catch the fancy of the other competitions, all of whom are looking at the problem from the same point of view. . . . We have reached the third degree where we devote our intelligence to anticipating what average opinion expects the average opinion to be. And there are some, I believe, who practice the fourth, fifth and higher degrees. (Keynes 1936: 156)

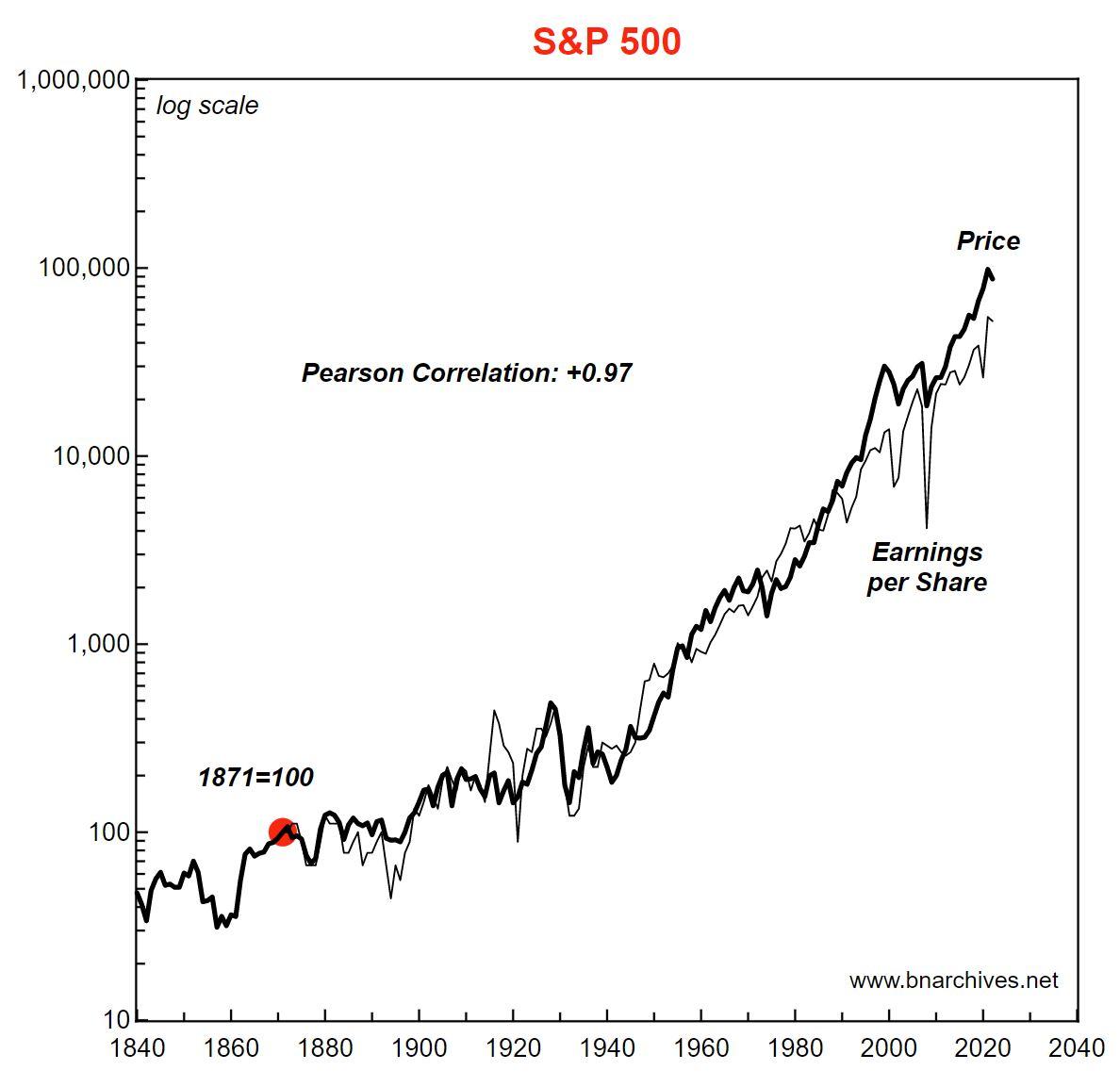

But in the long run, the picture is very different. The chart below shows the price and earnings per share of the S&P 500 group of companies (rebased with 1871=100), and as you can see, the long-term correlation between these two series is nearly perfect (+0.97). To my mind, this tight correlation suggests that, over the long run, the desire of “potential buyers with money to spend on capital assets” – i.e., the market’s “liquidity” – reflects not what investors think about each other, but what they think about future profit.

And this is where CasP’s claims about power and confidence in obedience come in. To earn a profit, corporate owners must exert their power over society. And to provide the liquidity needed to price this power, they must be confident that society will continue to obey them – because if it doesn’t, future profits will falter along with prices.

I can go on to talk how risk and the normal rate of return are also anchored in power, but I think my point is clear.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

September 9, 2022 at 11:31 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248323Thank you Scot.

Your claim, then, is that if, as a group, capitalists think that asset prices should be lower, they will likely go down — and if they think asset prices should be higher, they will likely rise. I believe we agree on this mechanism.

The interesting question is why. Why do capitalists. as a group, think that asset prices should be higher or lower — or, in your language, why should liquidity go up or down?

In my view, the answer has to do with what capitalists, as a group, think about future earnings, risk and the normal rate of return; and what they think about these three elementary particles hinges on power — that is, on the obedience of the system and people that they collectively rule (including policymakers, mind you).

Finally, if we agree that asset prices are set by the capitalists themselves, it follows that their capitalized power gauges their own confidence in this obedience.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

September 9, 2022 at 9:30 pm in reply to: Confidence in Obedience, or Confidence in Liquidity? #248321It seems to me that how capital assets are priced–i.e., looking backward or looking forward– reflects relative confidence in the proper functioning of the Market and, more specifically, the continued existence of liquidity.

Scot, what do you mean by ‘liquidity’, exactly?

September 6, 2022 at 11:47 am in reply to: Jujutsu: can we lever the power of capital against itself? #248307Thank you Pieter for the detailed articulation.

Concepts matter a great deal, particularly when they are key to a whole system of thinking, so it is great to see you engaging with the issue seriously.

Instead of cutting and pasting several pages here, allow me to refer you to our 2020 rejected interview with Revue de la régulation. Question 15 in this interview outlines our notion of power, and Question 16 illustrates how, in our opinion, power is conceived and operationalized in the capitalist mode of power.

As you will see, our view of social power, particularly in capitalism, differs significantly from the received everything-goes plethora of powers ‘over’, ‘to’, ‘with’, etc.

***

Given this discussion, we prefer to think of horizontal, autonomous cooperation not as a different from of power (to, with, etc.), but as the undoing of power. In this sense, to undermine capitalist power is not to convert this power or divert it to other social entities, but to reduce or eliminate it altogether.

This clear distinction saves endless entanglement and never-ending confusion.

- This reply was modified 3 years, 8 months ago by Jonathan Nitzan.

Also, what is the difference between “capitalization” as its used here and price/earnings ratios?

These are two distinct, albeit connect concepts.

1) P/E ratio = price per share / profit per share = capitalization / overall profit

In CasP:

2) capitalization = expected future profit / (risk x normal rate of return)

Note that P/E relies on current earnings that are known, whereas capitalization discounts expected future earnings that are unknown.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

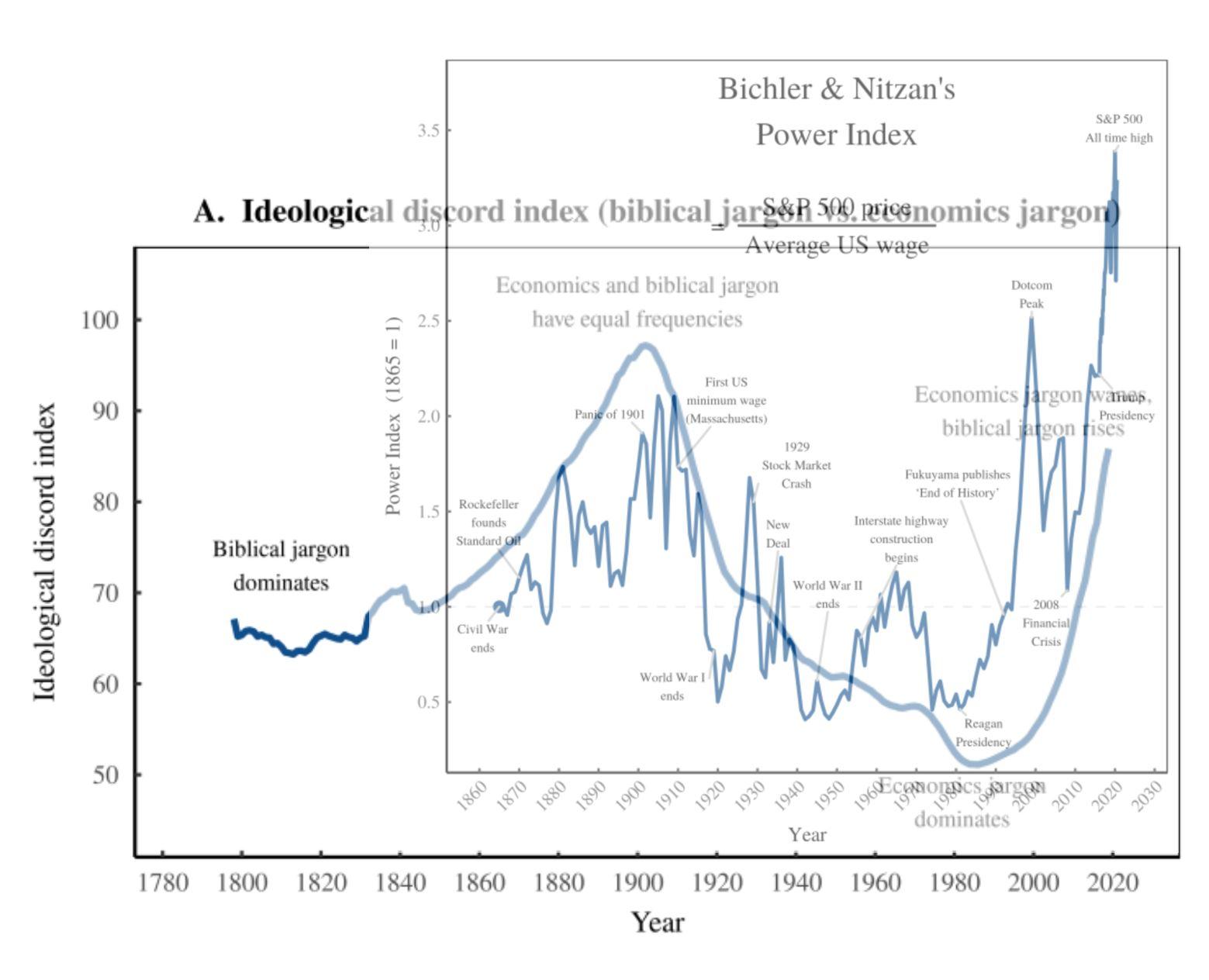

Note how Blair Fix’s ‘discord index’ shares the same periodicity/trajectories as our own ‘power index’: rising till around 1900, down-trending till the 1980s, and re-surging thereafter (notice, though, that in these charts the discord index is smoothed whereas the power index isn’t).

Blair, perhaps you can create a proper chart of this co-movement.

- This reply was modified 3 years, 9 months ago by Jonathan Nitzan.

Path Dependency

Path DependencyThis is Billy Summers’ last job, and, in a sense it is pre-written. It was ‘in the cards’ — or, as a theorist would say, it was ‘path dependent’.

Billy Summers, the protagonist of Stephen King’s 2021 novel, is a gun for hire. And he was bound to be.

As a boy, he shot his abusive stepfather after the man had beaten Billy’s younger sister to death; he spent his youth in a foster home; then, having nothing better to do, he volunteered to the Marine Corps; the Marines sent him to Iraq, where he became a decorated sniper; and upon his return to the U.S, he established himself as a professional assassin. He killed people for a living – but only after ascertaining they were ‘truly’ bad.

His last job – capitalized at two million dollars — is to take down an inmate on the courthouse steps, just as he enters his hearing. The inmate is definitely a bad guy, so Billy’s conscious is clear. But this is a thriller, so things aren’t what they seem to be. Billy senses he himself is next in line, and from there on the plot starts to thicken.

But the plot and its path dependencies are secondary.

Billy Summers is a book you read mostly for King’s gripping storytelling — his portrayal of backwater America, of the gruesome nature of war, of lust – particularly for power and money – and, most importantly, of the frail human psyche.

Highly recommended.

- This reply was modified 3 years, 10 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 10 months ago by Jonathan Nitzan.

- This reply was modified 3 years, 10 months ago by Jonathan Nitzan.

July 18, 2022 at 5:16 pm in reply to: Comment on “The Aggregate Demand Problem in Capitalism Solved” #248130I’d argue that credit, not wages, is central to all crises.

1. Note that my rough-and-ready description rehashes the convention perspective of economics, not my own view. It is meant to explain why Marxists and post-Keynesian see the general movement of wages as central for aggregate demand, even though it is only a segment of that demand.

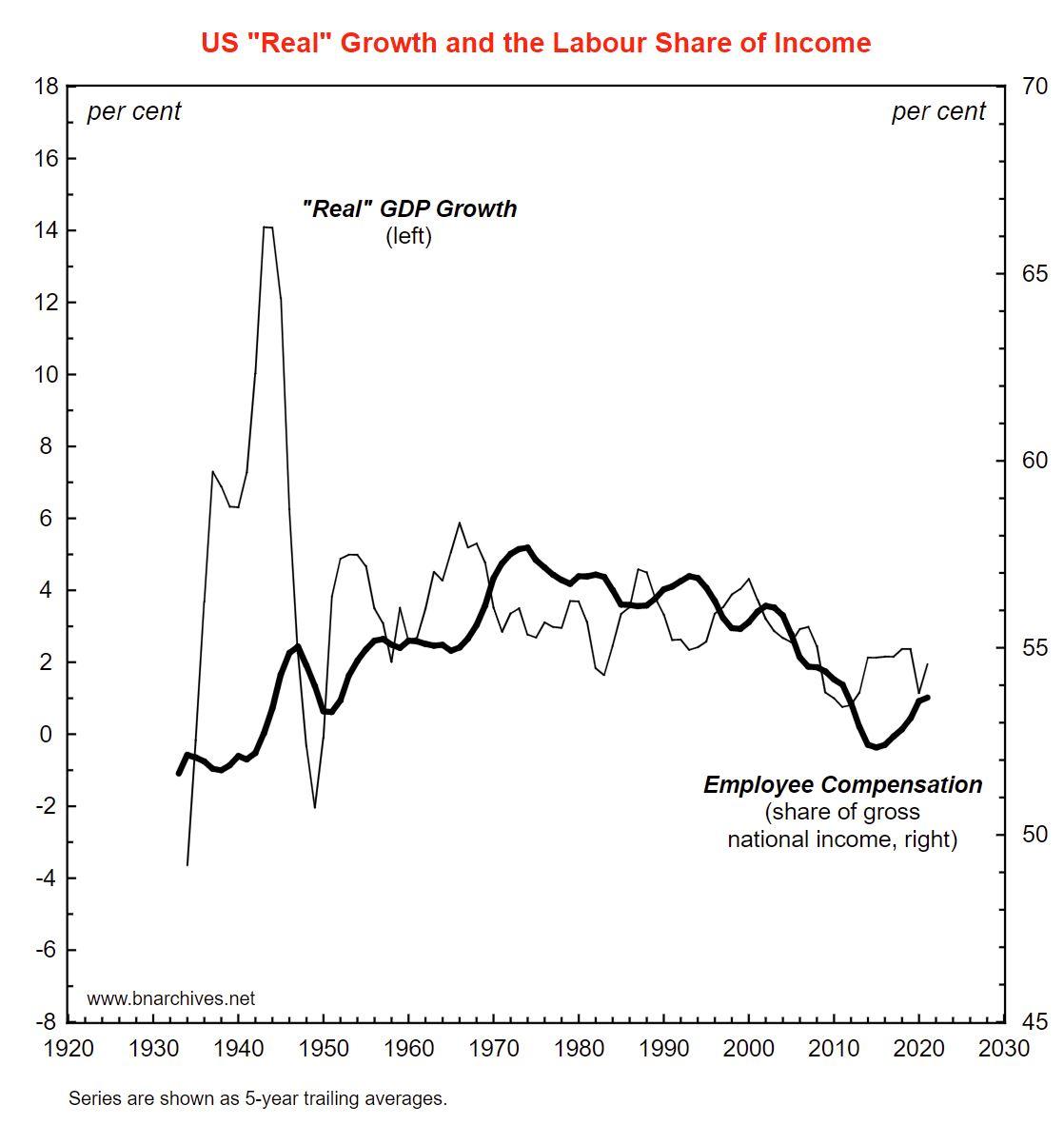

2. And yes, credit and capitalization more generally are the key organizing principle of capitalism. But the expansion of credit depends on distributional dynamics. If the wage share trends downward, credit expansion can surely fill the gap — but only to a point. The likelihood of banks lending more and more to increasingly wage-strapped workers and firms with bloated excess capacity is fairly small.

3. The figure below shows U.S. ‘real’ GDP growth along with the overall wage share in gross national income. The chart demonstrates that the wage share rose till the early 1970s and fell thereafter, and that ‘real’ growth followed a similar periodicity. The short-term differences between the series may have been affected by credit, but the long-term trends were not.

- This reply was modified 3 years, 10 months ago by Jonathan Nitzan.

July 17, 2022 at 1:38 pm in reply to: Comment on “The Aggregate Demand Problem in Capitalism Solved” #248128Why wages are central to economic crises

Crisis is a process of change, which is why economists tend to think of it in terms of growth. When output and employment decelerate, they say we have a recession; when they contract, they call the result a great recession; when they plunge, they speak about depression; and so on. The reason for these oscillations is the subject of ‘crisis theory’.

In line with JB Say’s maxim that supply creates its own demand, most mainstream economists think of crisis as an exogenous, temporary phenomenon. Since every sale is made for the purpose of a purchase, goes the argument, demand is never lacking, and occasional excess or shortage are quickly cleared by flexible, self-equilibrating prices. If the crisis lingers, the reason is always ‘exogenous’: external shock, government intervention, market imperfections – the outside spoiler list is endless.

Keynes critiqued this barter-like conviction. In capitalism, he pointed out, sales and purchases are mediated through money and separated in time, which means that demand can be reduced by saving. And since the incentive to save (withdraw earnings) is often inverse to the urge to invest (inject earnings to create new capacity), lingering recession and depression are possible not only in practice, but in theory too.

Marxists have a developed a full battery of crisis theories, summarized lucidly in Part Three of Sweezy’s 1942 book The Theory of Capitalist Development:

A second generation of crisis theories – post-Keynesian and neo-Marxist – married Keynes’ macroeconomics with Marx’s emphasis on class to examine more closely the impact of income distribution and concentrated market structures (Kalecki, Steindl, Baran & Sweezy, Magdoff, Braverman, Robinson, Kaldor, Eichner, Lee, Lavoie, etc.)

Keynesianism and Marxism, as well as their post- and neo- variants, consider the crisis role of both wage and non-wage income on aggregate demand. But wages are central in the following sense.

Aggregate demand comprises more than the consumption of workers alone. It also includes the consumption of capitalists, their investment in new capacity, the spending of government, and the purchases of foreign buyers.

On the face of it, then, it seems that capitalism can prosper even if labour income falls short of overall income – provided other earners consume, invest and spend enough to compensate for the shortfall.

But the analytical possibility of non-labour demand growing to compensate for the falling consumption of workers, argue Marxists and post-Keynesians, is tenuous in practice. Capitalist consumption is limited by the capitalist need to invest. Rising governments spending is restricted by the overriding logic of free enterprise. And most importantly, current investment is determined by the expectation of future demand, and since this demand depends mostly on workers’ consumption, investment is highly sensitive to the prospect of reduced wages (export demand is subject to all these limitations).

So, in the final analysis, wages, although making only part of aggregate demand, are central to all crises.

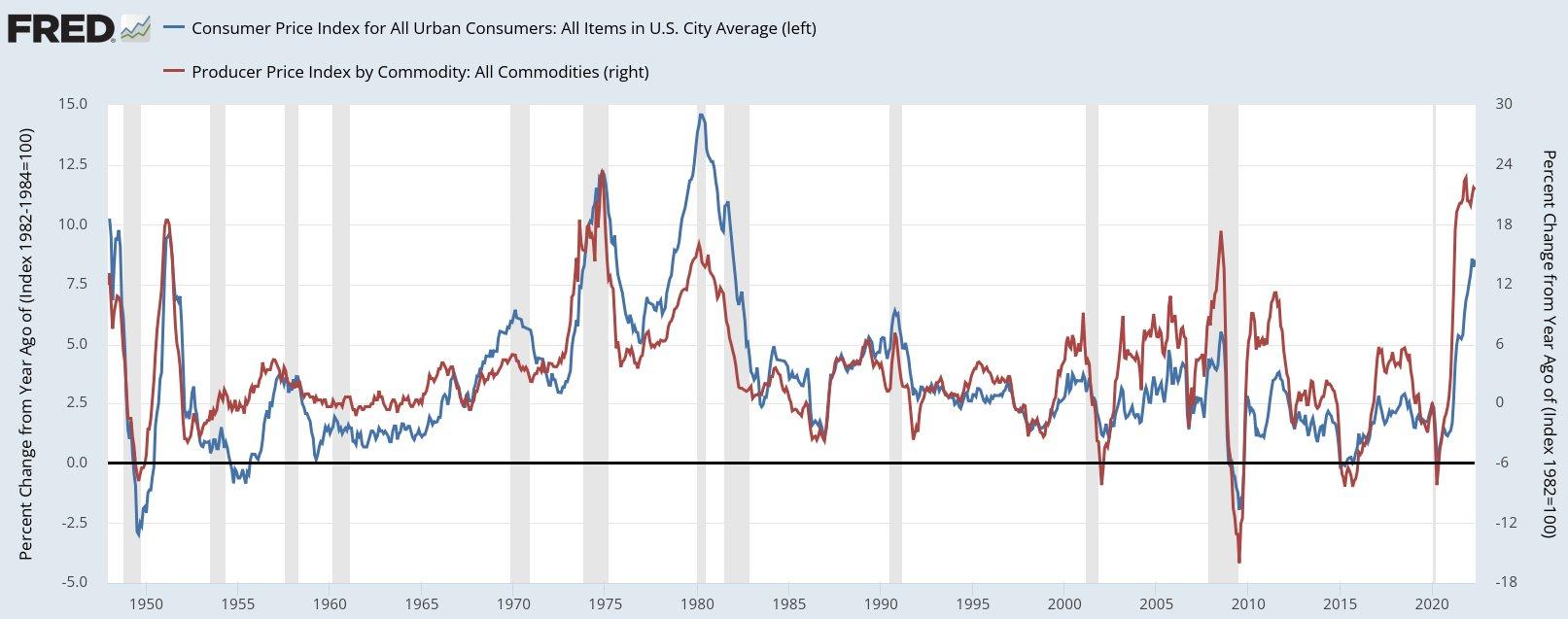

June 25, 2022 at 7:34 am in reply to: Inflation is always and everywhere a redistributional phenomenon #248114The May 2022 data for the United States, shown in the figure below, suggest that the current bout of inflation may be peaking. The chart contrasts the annual rate of change for consumer prices (left) with that of producer prices (right), and both series indicate that the process may be approaching its upper limits.

The reason for these limits has to do with the re-distributional essence of inflation.

Inflation is an average of individual price changes, and this average hides the most important driver of inflation: the fact that individual prices change and different rates, and that these differences redistribute income and assets.

The next chart contrasts the annual CPI inflation in the United States (red) with the annual rate of change of the purchasing power of wages (blue) — or what economists call the “real wage.” Note how the two series are inversely correlated: when CPI inflation accelerates, the rate of change of “real wages” decelerates, and vice versa.

This negative correlation suggests three things.

1. U.S. wage earners tend to lose from inflation — when inflation rises, U.S. wage increases tend to lag (and, inversely, rise faster when inflation slows). And since, on the upswing, wages rise more slowly than prices, the purchasing power of wage earners suffers.

2. Wage increases do not cause inflation — unless you insist on blaming workers for using wage increases to give capitalists the excuse to raise prices even faster.

3. Redistribution tends to limit the inflationary process — as inflation redistributes income from workers to capitalists, it undermines workers’ income-read-consumption, causing the the profitability of price-setters to gradually wane. Eventually, capitalists lose their price-hike resolve, their tacit coordination fractures, and inflation decelerates.

Is anyone aware of work done to “map” the financial system? […] I think an institution-driven mapping of financial networks would be more informative for understanding the state of capital.

Agreed. Such institutional mapping — particularly when quantified — would be highly useful. Creating it, though, would require expert familiarity with the financial process.

-

AuthorReplies